POSITIONS: Long Utilities (XLU), Short SPY, Short XLI, Short XLY

Much like my call last Tuesday “Short Covering Opportunity”, this one is explicit. There should be no mincing of words associated with my positioning. Ahead of tomorrow’s option expiration and inflationary CPI report, I’d love the opportunity to short 1401.

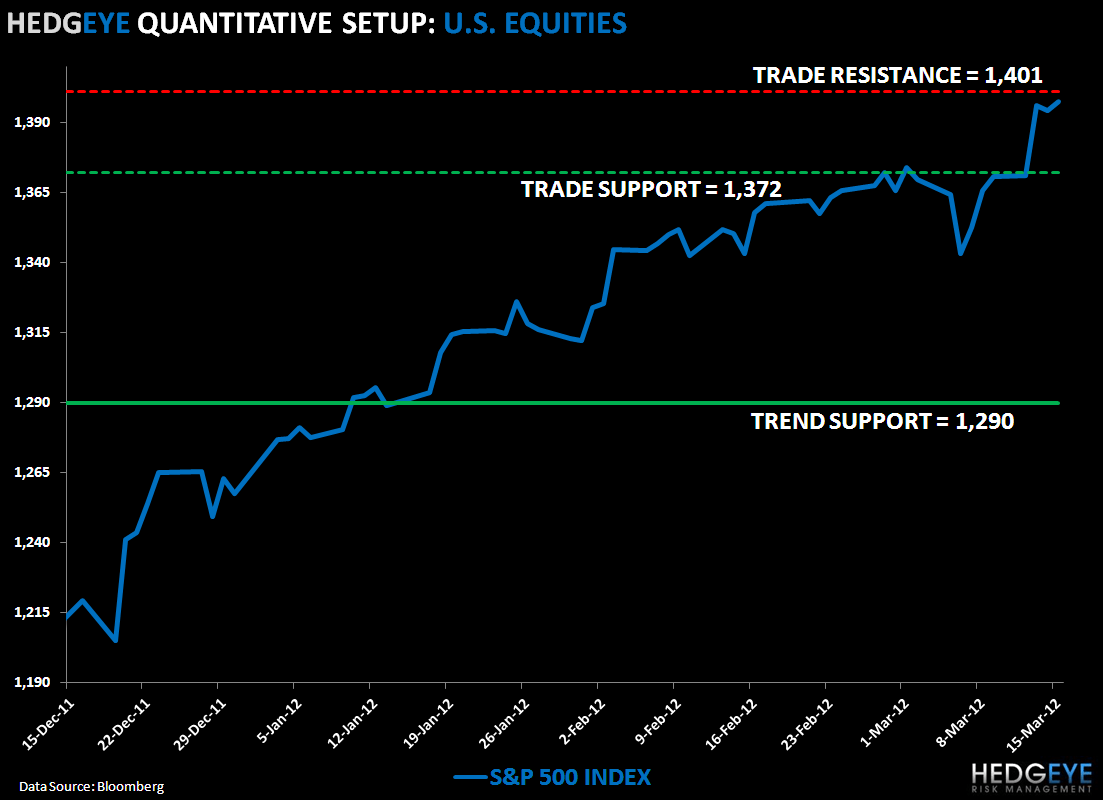

Across my core risk management durations, here are the lines that matter most:

- Immediate-term TRADE overbought = 1401

- Immediate-term TRADE support = 1372

- Intermediate-term TREND support = 1290

In other words, I’m looking at 3 points of upside versus almost 30 on the downside (wicked asymmetry). And since few agreed that there were 30 points of upside from last Tuesday’s 1345 line (there was 55), I say game on.

As (hopefully) many learned during the tops of Q1 2008, 2010, and 2011 – tops are processes, not points.

Manage this immediate-term range of risk accordingly,

KM

Keith R. McCullough

Chief Executive Officer