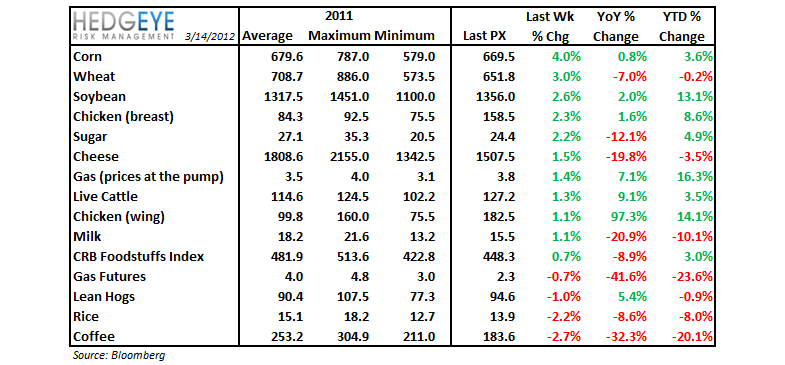

Despite the stronger dollar over the past week, the commodities that we monitor generally gained with the exception of pork, rice, and coffee.

CONSUMER CALLOUT

McDonald’s COO, Don Thompson, speaking at the UBS Global Consumer Conference, had the following to say about grocery inflation and its impact on McDonald’s business: “I think the projection for 2012 is for the grocery store prices, the food at home to moderate a little bit in the maybe 4% to 5%, 3% to 4% range and food away from home to be more like 2% to 3%. So that gap is closing but the projections are still for the grocery stores to be a little higher. If that means for us, our back store cost won't increase as much, that's a good thing.”

As our chart below illustrates, the spread between food at home CPI and food away from home CPI has been narrowing over the past four months. If the trend over the last four months were to continue, assuming the average rate of narrowing since the spread stopped widening, by the end of the second quarter the spread would be closed. While this is not a foregone conclusion, it is important to note that – on the margin – the gap has been closing and offering less of a competitive advantage to restaurants versus grocery stores.

SUPPLY & DEMAND

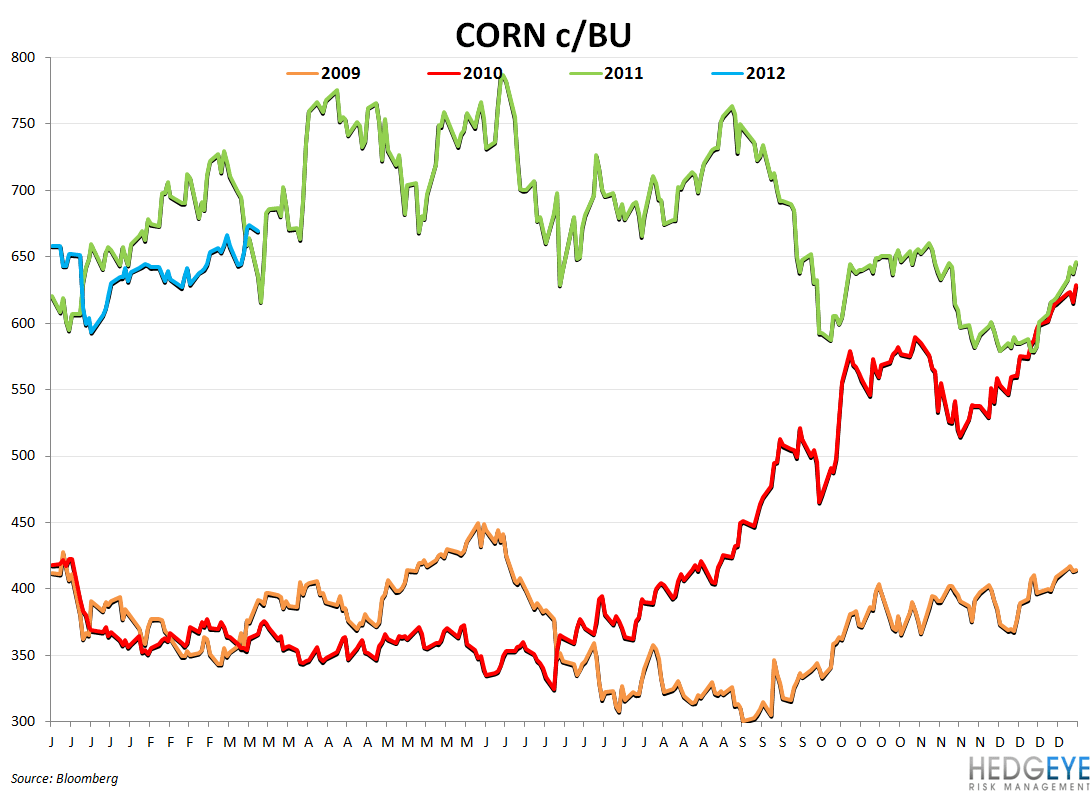

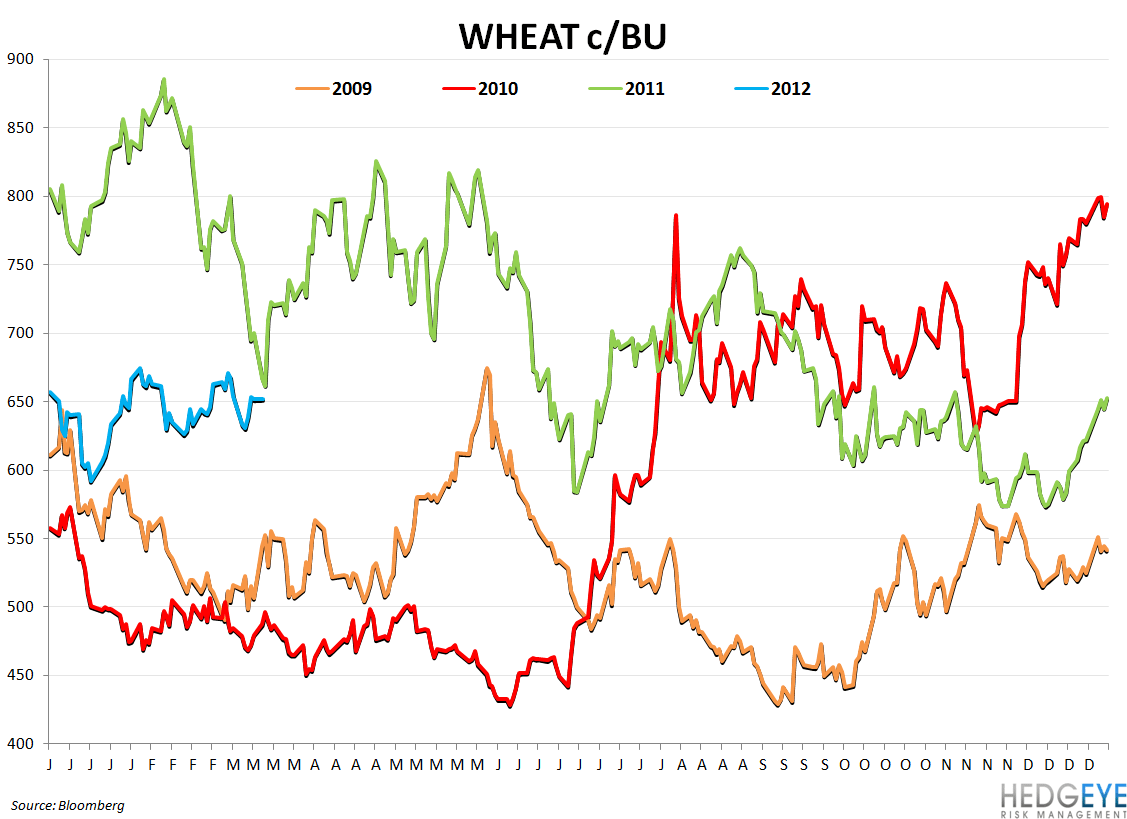

Wheat

SUPPLY

The USDA’s Wheat Outlook report is projecting world wheat production in ‘11/12 2011/2012 world wheat production is up 1.1 million tons this month to 694.0 million, further raising the historical record. In Australia, 2011/12 production is up 1.2 million tons to 29.5 million this month, and up 1.6 million tons on the previous year’s record.

DEMAND

Record production and stocks have stimulated trade. Iran is negotiating grain purchases with Russia, Pakistan, and India using letters of credit denominated in rubles and rupees to bypass Western banking sanctions. Globally, export forecasts have been increased for countries including Australia, Brazil, Kazakhstan, and the U.S.

Beef

SUPPLY

The USDA said that 922k farms raised cattle last year, 13k fewer than in 2010. The USDA has lowered its forecast for 2012 beef production by 80 million pounds and raised its forecast for fed cattle prices by $2.50/cwt.

The Texas AgriLife Extension Service is beginning a statewide educational initiative focusing on rebuilding cattle herds within the state. Dr. Ron Gill, AgriLife Extension livestock specialist said, “…The historic drought of 2011 dramatically accentuated that trend [declining herd sizes]. The state’s cattle industry and affiliated trade and service companies are the second largest economic driver in the state, bringing in billions of dollars to the state economy. With the cowherd at such a critically low level, Texas will start to lose infrastructure if cow numbers do not increase soon.”

The World Agricultural Supply and Demand Estimates from the USDA indicated that beef supplies will shrink further this year and imports will pick up, but not enough to account for lower production and continues strong exports, according to USDA projections.

DEMAND

Beef exports in January were even in volume versus a year ago but increased in value by 14%. Philip Seng, president of U.S. Meat Export Federation (USMEF), said that “there are opportunities to expand the presence of U.S. red meat by exploring new market niches as well as increasing access with several key trading partners.”

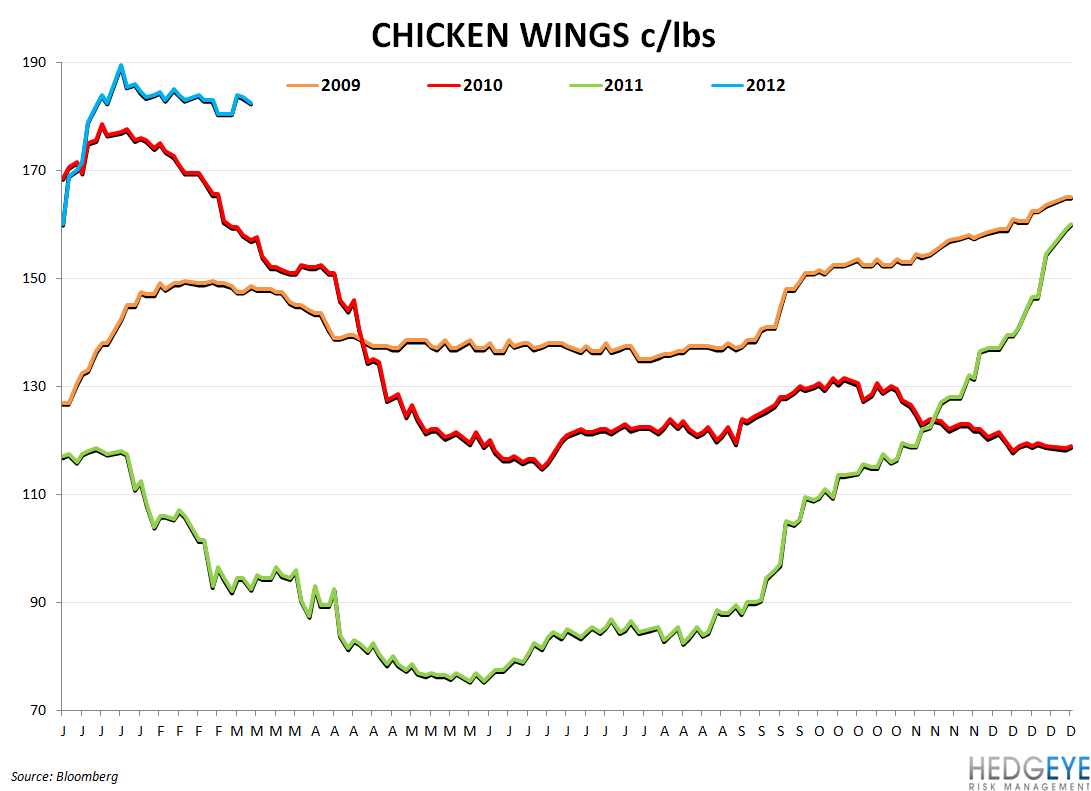

Chicken

SUPPLY

Egg sets placements continue to contract at around the same rate, at -5.4% for the six-week moving average, according to the Broiler Hatchery report released by the USDA today. This implies that supply will remain tight as the industry looks for more favorable business conditions before expanding production.

RECENT COMPANY COMMENTARY

Beef: Most companies are expecting beef cost inflation to be up mid-to-high single digits versus last year

TXRH: We expect approximately 8% food inflation in 2012, primarily due to higher beef costs…on the beef side we do have fixed price – pricing arrangements in effect for over 90% of our beef costs in 2012.

CBRL: To the continued pressure on ground beef prices and other commodities partly offset by lower average dairy and produce prices, along with benefits from our supply chain initiatives, we expect cost of sales to increase 60 basis points to 80 basis points over 2011 to near 26% in 2012.

RUTH: We project 2012 beef inflation to be between 5% and 8%. We currently have purchase agreements for beef representing approximately 30% of our needs through August of 2012, which represents an approximate 7% premium compared to the prior years.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans. Beef costs will be especially challenging due to protracted supply shortages, despite recent reductions in grain prices.

MCD: As we look at our guidance for 2012, we've built another mid-teens increase for beef, expecting that the dynamics in the marketplaces that we see, and are expecting, will continue.

DRI: U.S. beef production will continue decline though over the next 24 months, placing continued upward pressure on beef prices because of the slow economic recovery hamburger and value oriented beef, cattle beef are in high demand and can be priced accordingly by the packers. At Darden we purchased mainly tenderloins and other premium steakcuts, while we expect pricing for our beef products to increase by 12% our pricing has been tempered by consumers' resistance to record higher retail prices for premium stakes and the resulting shift to value oriented cuts and as you can see beef is approximately 14% of our cost basket … We have 75% of our beef requirements contracted for fiscal 2012 and 40% of the June to December usage under contract for fiscal 2013.

SONC: One item to note is that we recently locked in our beef contract for calendar year 2012… given the potential for beef costs going even higher, which there are a lot of reports out there that speculate that could happen, that we chose to go with making this more of a known quantity here, and the idea of having a set price for the next 12 months, we feel like would be good for our business, adds some predictability to the business.

Coffee: Prices are now down -32% versus last year

PEET: We expect 2012 coffee costs to rise 12% instead of last year's 42%.

SBUX: We've taken advantage of the recent declines in the C-price to lock in more of our coffee needs for fiscal 2013. We now have six months of our fiscal 2013 requirements secured at costs moderately favorable to 2012.

Dairy: CAKE, DPZ, PZZA, TXRH and others could benefit from favorable cheese costs this year

TXRH: The volatility around that 8% estimate for food cost inflation would really be driven by produce and dairy. Those are of the biggest components that we float around the market, and that's about 15% to 20% of our total cost of sales.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans.

CORRELATION TABLE

CHARTS

<chart12>

Howard Penney

Managing Director

Rory Green

Analyst