We don’t like VRA headed into the Q4 print, or coming out of it. It’s next to impossible for us to make a valuation call in this tape. But our model is 20% below Street expectations next year, which pretty much speaks for itself.

TRADE (3-weeks or Less)

We’re at $0.44 vs. the Street at $0.47E for Q4. We expect the shortfall to come from lower margins despite the likelihood of sales coming in above the upper end of guidance.

- Current expectations for a rebound in gross margins implies the impact of a timing shift in sourcing costs and opportunistic sale of retired inventory were one-time events and does not appear to reflect the current promotional climate or VRA’s exposure to cotton.

TREND (3-months or More)

Comps have been driven by pattern proliferation and additional category expansion over the last two years and are starting to slow putting greater emphasis on store growth to drive the top-line driving higher costs.

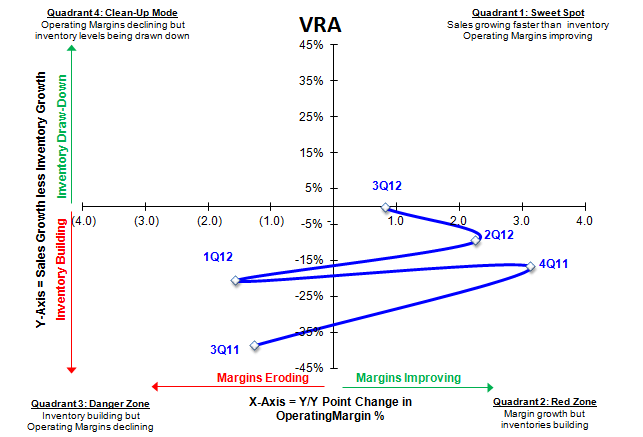

- Managing the inventory/sales growth spread will remain challenging in the 1H with sales slowing at the same time retailers get increasingly cautious on inventory.

- Top-line trends are already starting to roll. The top end of Q4 guidance implies a significant deceleration in both the 1yr and 2yr trends. We expect this trend to continue with mid 20%s revenue growth over the last two years slowing to a low-teens rate over the next two as retail and e-commerce growth offsets a decline in wholesale sales.

- In addition, our sense is that VRA is getting more aggressive with the terms it’s offering wholesale accounts to encourage earlier receipts. This tactic might work to drive sales over the near-term, but it’s not sustainable. Particularly given the profile and size of 25%-50% of VRA’s wholesale accounts, which simply don’t have the capacity to store excess inventory.

- Perhaps this is already happening. Management addressed concerns about product showing up at Costco on a recent conference call essentially revealing that while they don’t sell directly to Costco, a large wholesale account had flushed excess inventory through the discount channel. There is nothing to keep this from this happening again. It may be through smaller channels (think flash sale sites), but the evidence of over inventoried product inevitably comes to roost.

TAIL (3-years or Less)

VRA risks overextending the brand in pursuit of additional category expansion. At the same time, the company is looking to expand internationally into Japan and double the size of its DC which requires incremental investment.

- Square footage growth can come, but at a price we think is grossly underappreciated when it comes to VRA’s business model. Unlike the other brands, VRA is sold not through department stores (with the exception of a few Dillard’s locations), but rather through small independent retailers where VRA often drives and accounts for a meaningful percentage of sales at each wholesale account. Its network of 3,400+ small independent retailers is far more sensitive to the competitive threat of company-owned retail stores opening nearby than typical brands that are distributed in department stores that are far less reliant on any one vendor.

- Despite efforts to expand its product offering (e.g. rolling luggage), VRA is more constrained than the other brands in its ability to drive meaningful category growth limiting store productivity potential. This has been reflected in a material deceleration in comps to HSD with little to suggest a material reacceleration is likely.

- Over the last three years, SG&A leverage has accounted for 9 pts of margin expansion, which is now likely to shift in the other direction and suggests VRA was over earning in its first year as a public company. We expect this shift to result in a 2pt margin swing as a 1.5pt tailwind turns into a 0.5pt headwind this year (F13). (see table below)

- Over each of the last two years, VRA has kept Advertising, Marketing and Product Development flat to down. This is the line that accounts for new product initiatives for a brand that’s starved for expansion ideas – not good. We think VRA is going to be forced to take this line higher over the next few years. We are modeling this line up +10% and along with continued growth in selling expense expect SG&A deleverage for the first time in four years.

The stock appears to be baking in the kind of growth that we’d associate with the possibility of another department store partnership. We prefer to value what we see in front of us and that’s a brand challenged to grow with operating margins already over 20%. We are shaking out at $1.55 and $1.61 in EPS for F12 and F13 respectively 20% below Street expectations next year (F13). With the stock trading at 22x and 12.5x consensus F12 EPS and EBITDA estimates, this is not reflected in the stock here at $37. Nor is the structural risk in VRA’s wholesale accounts once it starts rolling out owned retail stores more aggressively.

Casey Flavin

Director