TODAY’S S&P 500 SET-UP – March 14, 2012

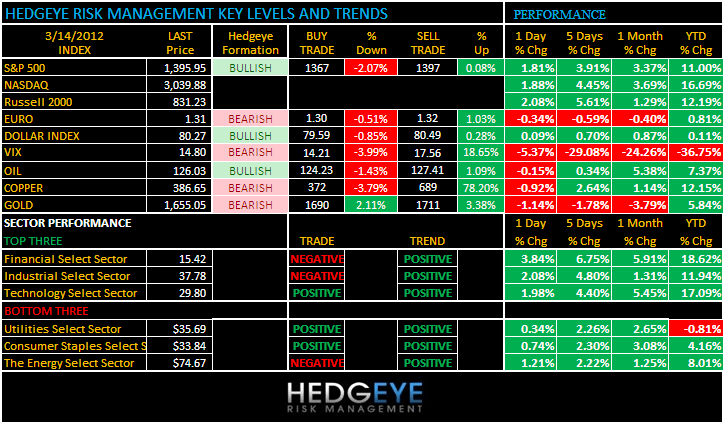

As we look at today’s set up for the S&P 500, the range is 30 points or -2.07% downside to 1366 and 0.08% upside to 1397.

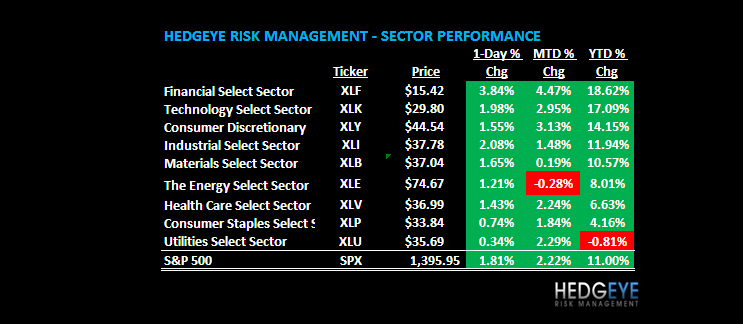

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1813 (2178)

- VOLUME: NYSE 907.12 (40.92%)

- VIX: 14.80 -5.37% YTD PERFORMANCE: -36.75%

- SPX PUT/CALL RATIO: 1.42 from 1.36 (4.41%)

CREDIT/ECONOMIC MARKET LOOK:

STOCKS – fascinating, but maybe not surprising, that the lowest “quality” countries in the world are leading the upside this morning (Japan +1.5%, Greece +2.6%, Romania +1.5%). China and Hong Kong closed down -2.6% and -0.2% post the “stress test” squeeze into the US market close. We should hang out up here in the nosebleed seats, until we don’t – new SPX range = 1.

BONDS – kaboom! 2-yr US Treasury yields are only up about +33% in 10 days, so there’s really no Global Macro interconnected risk with this Bernanke pancake plan, is there? Only if you are long anything Bonds, Gold, or FX – 10yr absolutely ripped after it crossed my 2.03% line. This is one of the biggest off-sides 1-day moves I’ve ever seen in Global Asset Class attribution.

- TED SPREAD: 39.24

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.20 from 2.13

- YIELD CURVE: 1.84 from 1.78

MACRO DATA POINTS (Bloomberg Estimates):

- 7:00am, MBA Mortgage Applications, week of Mar. 9 (prior - 1.2%

- 8:30am, Import Price Index (M/m), Feb., est. 0.6% (prior 0.3%)

- 8:30am, Current Acct Balance 4Q, est. -$115.0b (prior -$110.3b)

- 10am, Bernanke speaks in Nashville, Tenn. at Independent Community Bankers convention

- 1:00pm, U.S. to sell $13b 30-yr bonds (reopening)

GOVERNMENT:

- British PM David Cameron visits White House, holds joint press conference with President Obama

- House not in session, Senate meets

- Senate Agriculture Committee holds hearing to develop a 2012 farm bill. 10am

- Senate Foreign Relations Committee hears from actor George Clooney on Sudan and South Sudan. 10am

- Senate Finance Committee holds hearing on proposal to establish permanent normal trade relations with Russia. 10am

- Supreme Court not in session

WHAT TO WATCH:

- Rick Santorum won Alabama, Mississippi presidential primaries, strengthening his status as Mitt Romney’s main challenger; Romney won Hawaii’s caucuses: AP

- Apple said to be subpoenaed by FTC as part of antitrust probe of Google, seeking information on how company incorporates the search engine on iPhone, iPad

- Fed yesterday said 15 of 19 banks passed stress tests; JPMorgan, Wells Fargo raised dividends, share purchases after getting approval while Citigroup will resubmit capital plan

- Boeing to pay Air India $500m in compensation because of delays in delivering 27 on-order 787 Dreamliners

- Carlyle, Onex Group seeking to take Allison Transmission Holdings public at valuation almost triple what they paid

- BofA, JPMorgan, three other banks agreed to pay $25m to NY to resolve some monetary claims over use of mortgage database after reaching $25b national settlement on foreclosure practices

- Senate will vote today on two-year, $109b bill to fund highway construction, mass transit

- Roche gets second FTC information request on Illumina deal

- Yahoo! put CFO Tim Morse on board of Alibaba to fill position vacated by Jerry Yang when he stepped down in Jan.

- U.S. budget deficit shortfall for 2012 will be $1.2t, ~$93b more than forecast two months ago, CBO said in report yesterday

- Five biggest European telecoms may face investigation by EC, FT says

EARNINGS:

- Lin TV (TVL) 7:30am, $0.20

- Marcus (MCS) 7:45am, NA

- Vera Bradley (VRA) 4pm, $0.47

- Youku (YOKU) 4pm, $0.05

- Guess? (GES) 4:05pm, $1.04

- Power Corp of Canada (POW CN) 4:17pm, $0.55

- Semafo (SMF CN) 4:50pm, $0.13

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Anglo’s Diamonds Seen as M&A Turnoff for Glencore: Commodities

- Copper Drops as China Signals Housing-Market Curbs Will Remain

- Oil Declines on Forecast U.S. Supply Rose to Six-Month High

- Gold Seen Heading for 12th Annual Advance on Investor Hoarding

- Gold Drops as Economic Recovery Curb’s Metal’s Investment Demand

- Palm Oil to Climb to Year High as Cooking-Oil Supply Drops

- YPF Given Five Days to Retract Argentine Province Price Increase

- Soybeans Reach Six-Month High on Supply Concern, China Demand

- IEA Predicts Bumpy Ride for Oil Prices Amid Non-OPEC Supply Cuts

- Vekselberg Crisis Warning Spurs Rusal Yield Surge: Russia Credit

- Wheat Stockpiles in Australia Seen at Record 10.5 Million Tons

- Dubai Oil Draws Near to Brent on Iran, Asian Use: Energy Markets

- Copper Stocks at ‘Critical Level’ Signal Rise: Chart of the Day

- Gold Seen Heading for 12th Annual Advance

- Coffee Reaches One-Week Low as Supply May Improve; Sugar Drops

- Indian Funds Best Gold Deal as Producers Trail: Riskless Return

- Gazprom Trips in India as Shale Upends Asia Gas Markets: Energy

CURRENCIES

CURRENCIES – so the Japanese Yen is crashing (down -9.1% in 2 months) and now the Euro is back into a Bearish Formation. The best news we have here, but only for Americans, is that Strong Dollar is potentially back (until Qe4 whispers come on a 50bps SPY down move). But the globally interconnected risk to a sustained strong dollar (Gold hammered) is tangibly evident.

EUROPEAN MARKETS

ASIAN MARKETS

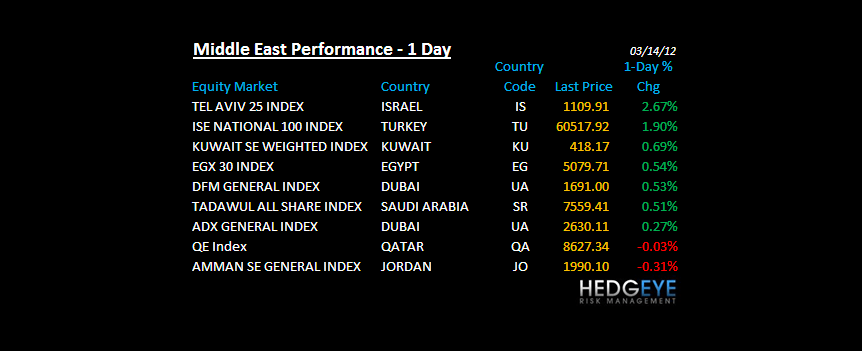

MIDDLE EAST

The Hedgeye Macro Team