With Buffalo Wild Wings’ stock up 32.5% year-to-date, our negative research stance heading into the 4Q11 EPS print has definitely left a scar. We are also not going into hiding because the facts indicate that some important questions need to be answered by Buffalo Wild Wings to sustain its stock price at current levels. Besides the more specific issues facing the company, the macro environment for restaurant stocks is generally positive – for now. Here we run through our updated thoughts on the stock.

Our view of Buffalo Wild Wings’ 4Q11 results was that, while the top line numbers were impressive, it was disconcerting that margins did not expand despite the fact that elevated wing prices were yet to impact the P&L. On its own, this fact would likely have been enough to prompt skepticism among investors but – unfortunately for our research call – the 1Q12 to-date (as of 2/7) same-store sales number, at 12.9% at company locations, superseded any margin-related concerns.

The stock has settled in at around $90 and the EV/EBITDA (NTM) multiple has expanded to 10x. We are less than convinced that this current price level is sustainable over the intermediate term TREND and see significant risk to the downside if the company does not execute to perfection over the next two quarters. The Street, it seems, shares this view; despite the impressive 1Q guidance and the implied same-store sales trends, FY12 EPS estimates did not move significantly. Estimates for 1Q12, appropriately, were revised sharply higher but it seems that analysts are waiting to see how the rest of the year plays out (chart1, 2). Our view is that costs will play a more significant role in 2Q and 3Q than consensus is allowing for.

Here are some points we are currently focused on:

- The sequential move in comparable-restaurant sales from 8.9% in 4Q11 to 12.9% for the first five weeks of 1Q12 benefitted by 3% from the impact of gift cards and also, we estimate 2-3% of favorable weather impact. Our estimate for the real current run-rate of comps is 7%. Gift cards may not have as much of a favorable impact on the full quarter comp versus January’s but we still expect a significant boost from gift cards and weather for 1Q12 comps.

- The Street obviously gave the company a pass on flat margins in 4Q, despite a stronger-than-expected top line, due to the 12.9% 1Q12 to-date same-store sales number released coincidentally. 4Q11 was a poor quality quarter for BWLD given the lack of flow through on strong comps and the fact that the tax rate was lower than expected. Unless the company can keep disclosing quarter-to-date comps far in excess of expectations, the lack of leverage in the business model will be a concern for investors. Without gift card and weather benefits, especially in the event that the broader employment outlook softens the stock price could move lower. Tougher top line compares are coming in 2Q and 3Q for BWLD and we believe investors will be seeking reassurance from management that the momentum in sales is continuing into April when 1Q EPS is reported (chart 3).

- We are hearing from some franchisees that sales softened in the second half of February. Gas prices (up 6% in the two weeks from 2/15) are thought to have been a factor.

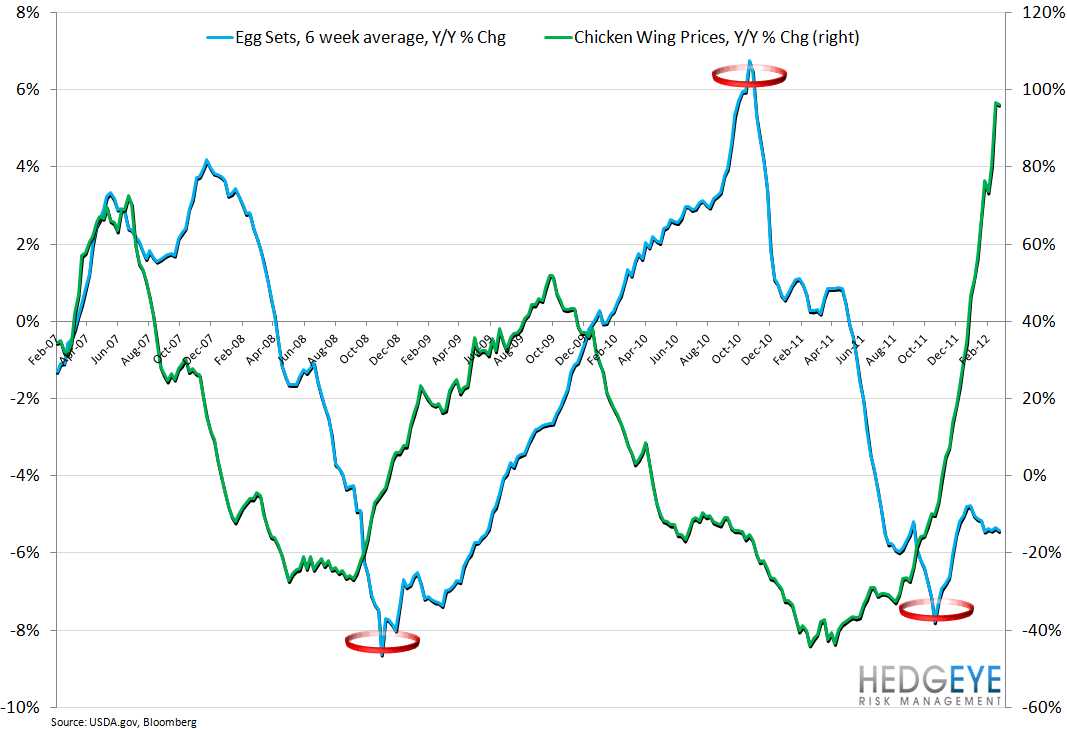

- Chicken prices continue to head higher. While chicken wings led the way, other cuts are now following; breast, leg, and full bird prices are all gaining as elevated beef prices push food service toward chicken products. This demand for chicken is a bullish indicator for wing prices. Additionally, as the processors continue to struggle, supply remains constrained (chart 4).

- Sanderson's Farm (SAFM) is up 14% over the past month on the improved outlook for chicken prices.

- In order to manage inflation and meet EPS expectations, management will likely need to cut costs and/or raise prices. Both of these strategies could ultimately have a negative impact on the top line. Cutting G&A costs is not without its risks for a "growth" restaurant company given the likelihood that it might impact revenue growth down the road. Additionally, as we learned on the 2Q11 EPS earnings call, expanding the concept's geographical reach - a key component of the growth story - requires significant G&A investment.

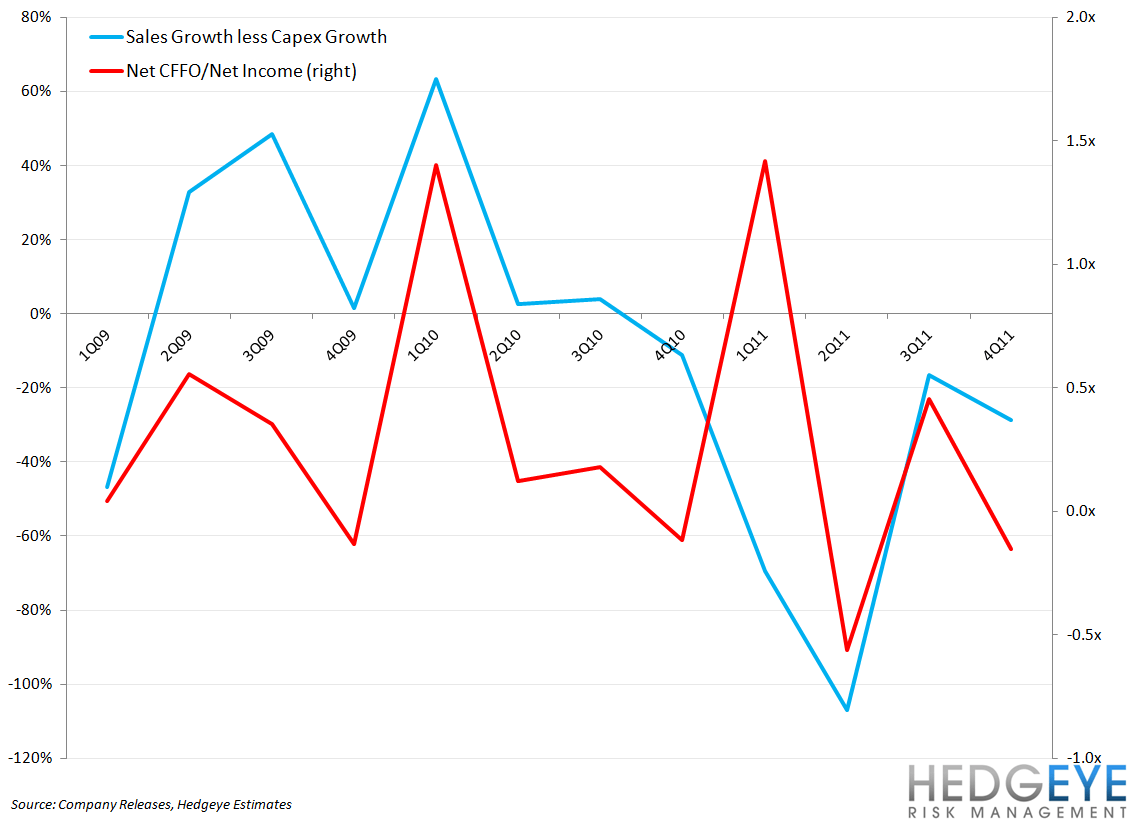

- Management mentioned the possibility of acquiring or developing a second concept. This is generally a huge drain on company resources and can require significant investment. We would be initially skeptical of this notion but obviously will reserve judgment until such a time that management might disclose more detail. Our initial concern is founded upon the fact that BWLD is not generating much cash flow (after growth-related expenses). The company’s net CFFO-to-net income ratio has been barely positive over the last year (chart 5). If margins contract in 2Q and 3Q, that only heightens our negative view of BWLD acquiring an additional concept; the company would have to lever up to acquire a second concept of significant scale.

- AT 10x EV/EBITDA, BWLD looks very expensive for a company with a checkered past of inconsistent operating performance.

Howard Penney

Managing Director

Rory Green

Analyst