No change to our full month GGR forecast of HK$24-26 billion, up 23-33% YoY.

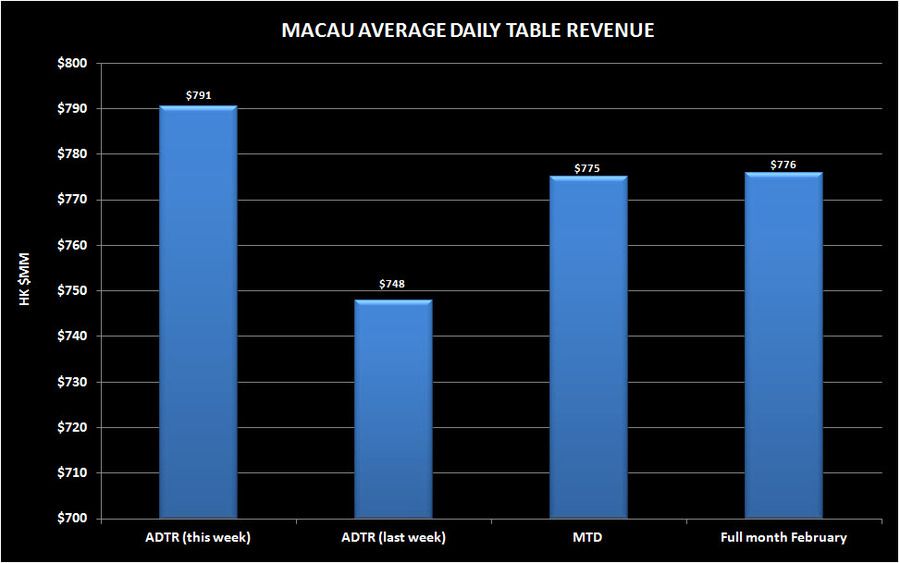

Average daily table revenues (ADTR) jumped to HK$790 million this past week, up from HK$776 million in February. Month to date, ADTR is in-line with February.

Remember that the comp is fairly easy as VIP hold % was the lowest in 2011. Nonetheless, overall business levels should be considered very strong and above consensus expectations.

MPEL appears to have lost a lot of share in the past week, no doubt due to hold, while Galaxy gained the most. Relative to trend, MGM seems to be performing the best in March while MPEL and LVS are below.