THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Commentary from CEO Keith McCullough

Greece, slowly, but surely falling off Most Read (Bloomberg) news wk-over-wk; China and Global Growth Slowing back in vogue:

- CHINA – worst Trade Deficit in 22yrs (let’s call that ever – and ever is a long time) at -$31.5B after last week saw that big sequential drop in Chinese IP growth (to 11% vs 14% in JAN despite Lunar shift). Growth Slowing. Chinese stocks looking for a rate cut.

- ISRAEL – someone knows something or someone thinks they do – what I can’t see here makes me call it out as the Tel Aviv25 Index not only moved to red for 2012 YTD last week, but is down another full 1% this morning (down -4% in since Feb 21). Iran?

- USD – the most important (and bullish on the margin for US Consumption Growth) recovery in the last few weeks has been the US Dollar Index recovering its intermediate-term TREND support of $79.36. With short-term Treasuries (2yr) breaking out above 0.26% TREND support and Gold struggling relative to oil, I’m out of Gold for now. Considering the short side GLD and looking to buy USD back.

VIX 15-17 range has proven to be the right zone to take down both gross and net for the last 4yrs.

KM

SUBSECTOR PERFORMANCE

QUICK SERVICE

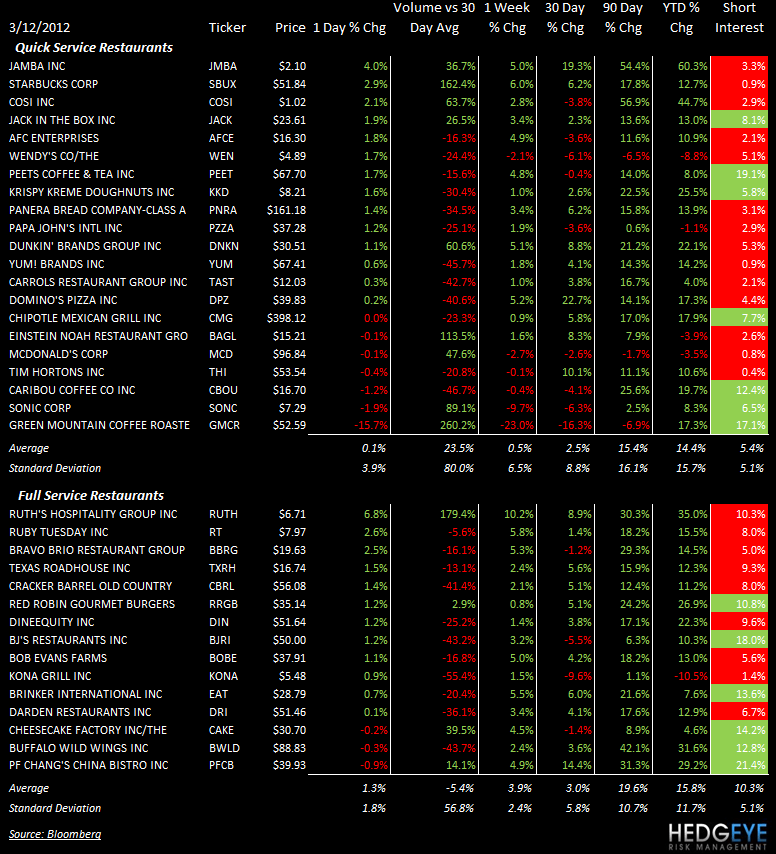

GMCR: Green Mountain Coffee was downgraded to Neutral from Buy by BofA on Friday. The price target was lowered to $63 from $70.

MCD: McDonald’s featured in a Barron’s article this weekend where “the Trader” column detailed why the stock may be overpriced.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

GMCR: Green Mountain declined almost 16% on accelerating volume as SBUX announced the arrival of its new brewer and David Einhorn said that Green Mountain’s install base has no “true protection”.

SBUX: Starbucks gained 2.9% on accelerating volume.

CASUAL DINING

RUTH: Ruth’s Chris announced 10% buyback of its 10% convertible preferred stock. Retiring the 10% convertible preferred stock cost the company $60.2mm in cash which was funded by its $100mm senior revolving credit facility. This move prompted Jeffries to raise its PT by $1 to $8.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

RUTH: Ruth’s Chris gained 6.8% on accelerating volume.

Howard Penney

Managing Director

Rory Green

Analyst