No Current Positions in Europe

Asset Class Performance:

- Equities: Bottom performers: Cyprus -7.9%; Slovakia -3.9%; Ukraine 3.9%; Spain -3.3%; Austria -3.0%. Top performers: Switzerland 60bps; Greece 40bps

- FX: The EUR/USD is down -0.61% week-over-week. Divergences: SEK/EUR -1.3%, NOK/EUR -1.1%; HUF/EUR -0.96%, GBP/EUR -0.34%; CHF/EUR +0.07%.

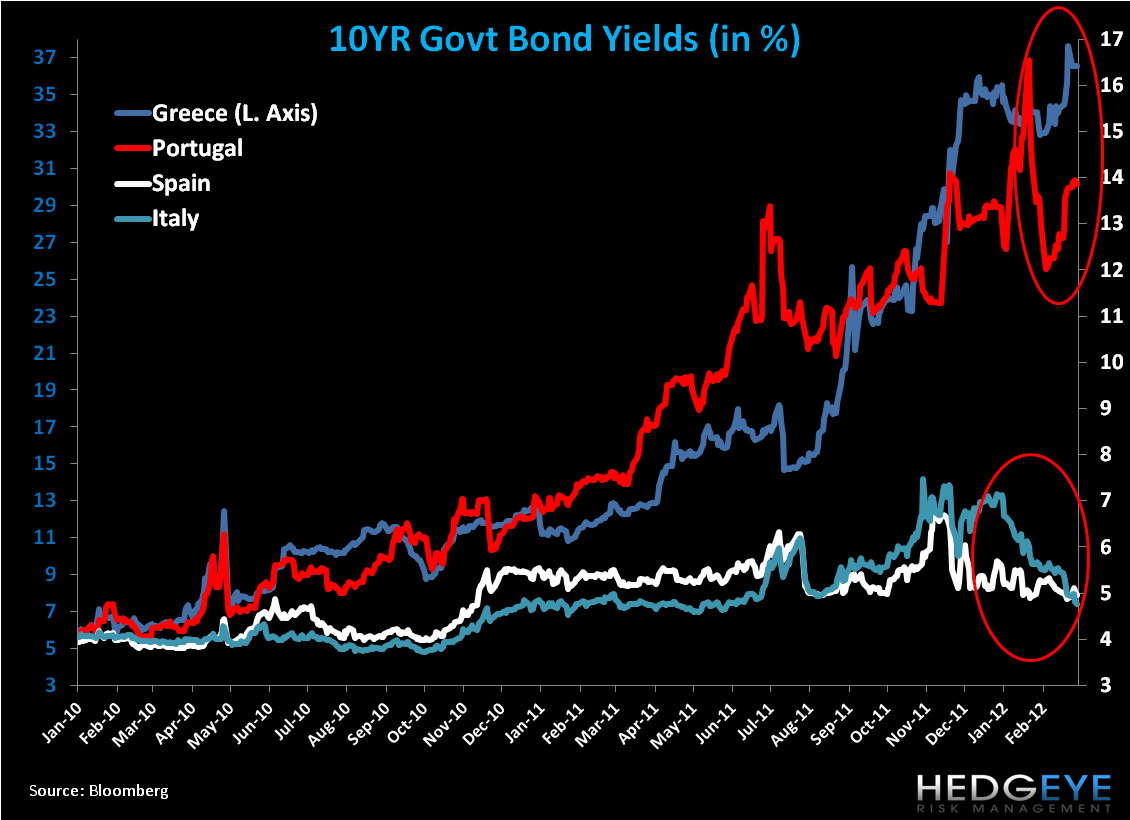

- Fixed Income: Excluding Greece, 10YR sovereign yields we largely flat week-over-week. Greek yields tumbled a 109bps on the PSI announcement, while the Italian 10YR yield saw the second greatest decline at -18bps to 4.77%. Spanish and Italian yields continue to trend lower, while Portugal flashes increased signs of risk.

In Review:

Once again we’ve gotten past a hurdle in the market with confirmation just this morning that the Greek PSI received the critical participation rate, Collective Action Clauses (CACs) were activated, and ISDA ruled that the bonds swapped will trigger a CDS event. However, what’s lost in the near-term hurdles is the underlying flaws of a Union of disparate countries governed by one monetary policy. Namely without the ability to devalue one’s currency and inflate one’s way out debt obligations, or even default (which Eurocrats continue to suspend), Eurozone countries (like a Greece, Portugal, or Spain) can at best deflate wages to gain competitiveness. The problem with this policy, of course, is that it reduces domestic spending power, and therefore further stagnates total output.

The major fallacy that Eurocrats are running with is that through the Fiscal Compact they can manage governments’ budgets, initially by setting targets on debt and deficit levels and when necessary intervening to assure these targets are met. The flaw in this assumption is that countries are not likely to give up sovereignty to Brussels or Frankfurt to manage their spending, and that setting “artificial” targets is inappropriate for disparate countries, and hasn’t worked in the past (think Stability and Growth Pact). For economies that are not all created equal – for example, some may have large current account surpluses and others deficits or varying levels of capital accounts (investment) –a Union with one monetary policy inadequately addresses disparate levels of growth, and can distort the flow of goods and investment across countries.

While the above only begins to touch on the imbalance created in binding uneven economies to one monetary policy, here we’ll reiterate that we do think Eurocrats will do everything in their power to maintain this existing and flawed Union. We expect this to bring volatility to markets, like we’ve seen over the last 18+ months, and monetary policy to continue to drive a larger divergence in the “Have’s” versus “Have Nots” within the Union, which will ultimately lead to protracted economic weakness and fiscal imbalances.

Data Dump:

Eurozone Q4 GDP -0.3% Q/Q and 0.7% Y/Y

Eurozone Retail Sales 0.0% JAN Y/Y vs -1.3% DEC [0.3% JAN M/M vs -0.5%]

Eurozone Sentix Investor Confidence -8.2 MAR vs -11.1 FEB

Germany Factory Orders -4.9% JAN Y/Y (exp. -1.7%) vs 0.0% DEC

Germany Exports 2.3% JAN M/M vs -4,4% DEC

Germany Imports 2.4% JAN M/M vs -3.9% DEC

Germany Industrial Production 1.8% JAN Y/Y (exp. 1.1%) vs 1.3% DEC [1.6% JAN M/M (exp. 1.1%) vs -2.6% DEC]

Germany CPI 2.5% FEB Final, in line w initial

France Manufacturing Production -1.2% JAN Y/Y vs 0.8% DEC

France Industrial Production -1.5% JAN Y/Y vs -1.2% DEC

France Bank of France Business Sentiment 95 FEB vs 96 JAN

France Non-Farm Payrolls -0.1% in Q4 Q/Q vs -0.2% in Q3 Q/Q

Greece Q4 GDP -7.5% Y/Y vs original est. of -7%

Greece CPI 1.7% FEB Y/Y vs 2.1% JAN

Greece Unemployment Rate 21.0% DEC vs 20.9% JAN

Portugal Q4 GDP -2.8% Y/Y vs -2.7% in Q3 [-1.3% Q/Q vs -1.3% in Q3]

Spain Retail Sales -4.8% JAN Y/Y vs -6.4% DEC

UK BOE/GfK Inflation next 12 months 3.5% FEB Y/y vs 4.1% JAN

UK Industrial Production -3.8% JAN Y/Y vs -3.1% DEC [-0.4% JAN M/M vs 0.4% DEC]

UK Manufacturing Production 0.3% JAN Y/Y vs 0.9% DEC [0.1% JAN M/M vs 1.1% DEC]

UK PPI Input 7.3% FEB Y/Y vs 6.6% JAN [2.1% FEB M/M vs 0.1% JAN]

UK PPI Output 4.1% FEB Y/Y vs 4.0% JAN [0.6% FEB M/M vs 0.4% JAN]

Sweden Industrial Production 2.1% JAN Y/Y vs -0.4% DEC

Norway CPI 1.2% FEB Y/Y vs 0.5% JAN

Switzerland CPI -1.2% FEB Y/Y (exp. -0.7%) vs -0.9% JAN

Switzerland Retail Sales 4.4% JAN Y/Y vs 1.7% DEC

Interest Rate Decisions:

BOE Interest Rate UNCH at 0.50% and bond purchasing program remains at 325 Billion GBP

ECB Interest Rate UNCH at 1.00%

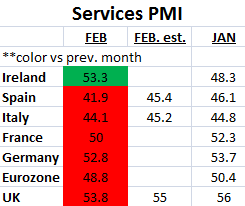

Services PMI:

CDS Risk Monitor:

Compared to previous weeks, we did not see huge moves in 5YR CDS on a week-over-week basis. Portugal rose the most at 42bps to 1229bps, followed by Spain (+37bps) to 396bps, Ireland (+32bps) to 620bps, and Italy (+10bps) to 369bps. One inflection to note is that Italian CDS traded below Spain, throughout the week. As the chart below shows, since August 2011, Italian CDS was priced comfortably above Spanish CDS.

The European Week Ahead:

Monday: Eurogroup Meeting; Q2 Germany Manpower Employment Outlook; Feb. Germany Wholesale Price Index; Feb. UK RICS House Price Balance; Q4 Italy GDP – Final; Jan. Greece Industrial Production

Tuesday: Mar. Eurozone ZEW Survey (Econ. Sentiment); Mar. Germany ZEW Survey (Current Situation and Econ. Sentiment); Jan. UK House Prices, Trade Balance; Feb. France CPI; Jan. France Current Account; Feb. Russia Budget Level (Mar 13-15); Jan. Russia Trade Balance; Feb. Italy and Spain CPI - Final

Wednesday: Feb. Eurozone CPI; Feb. UK Claimant Count, Jobless Count Change, Jan. UK Weekly Earnings, ILO Unemployment Rate

Thursday: Mar. Eurozone Monthly Report Published; Feb. Eurozone 25 New Car Registrations; Q4 Eurozone Labour Costs, Employment; Jan. Italy General Government Debt; Q4 Spain House Prices; Q4 Greece Unemployment Rate

Friday: Jan. Eurozone Trade Balance; Feb. Russia Industrial Production, Producer Prices; Jan. Italy Trade Balance, Current Account; Q4 Spain Labour Costs

Extended Calendar Call-Outs:

20 March: Greece’s €14.5 billion Bond Redemption due.

22 April: French Elections (Round 1) begins, to conclude in May.

29 April: Potential Greek Presidential Elections

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst