TODAY’S S&P 500 SET-UP – March 9, 2012

As we look at today’s set up for the S&P 500, the range is 37 points or -1.53% downside to 1345 and 1.18% upside to 1382.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1777 (53)

- VOLUME: NYSE 716.61 (-10.53%)

- VIX: 17.95 -5.87% YTD PERFORMANCE: -23.29%

- SPX PUT/CALL RATIO: 0.98 from 1.74 (-43.68%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 39.72

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.01 from 2.01

- YIELD CURVE: 1.70 from 1.71

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Trade Balance, Jan., est. -$49.0b (prior -$48.8b)

- 8:30am: Nonfarm Payrolls, Feb., est. 210k (prior 243k)

- 8:30am: Unemployment Rate, Feb., est. 8.3% (prior 8.3%)

- 8:30am: WASDE corn, soybean, cotton, wheat

- 10:00am: Wholesale Inventories, Jan., est. 0.6% (prior 1.0%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Obama to speak on economy at Rolls-Royce aerospace facility in Richmond, Va. 12:30pm, then fly to Houston for campaign events

- CFTC meets to consider issuance of proposed rules, 9:30am

- House meets in pro forma session, 11am

WHAT TO WATCH:

- U.S. payrolls may have increased by 210k in Feb. after rising 243k in Jan., economists est.

- Investors with 95.7% of Greece’s privately held bonds will participate sovereign debt restructuring after govt said it will trigger an option forcing them to take part

- UPS said to be near deal to buy TNT Express after initial offer of EU4.9b rejected

- El Paso holds a shareholder vote on $21.1b Kinder Morgan deal

- Watch video-game makers after NPD reported U.S. video-game sales fell 20% in Feb. to $1.06b

- Texas Instruments cut 1Q sales, profit forecasts; watch chipmakers, suppliers

- Molycorp agreed to buy Canada’s Neo Material Technologies for ~C$1.3b ($1.3b) to increase Chinese sales, gain technology

- Boston Scientific agreed to buy Cameron Health for as much as $1.35b to add a new kind of defibrillator

- Wal-Mart wins South African lawsuit contesting Massmart takeover

- London Stock Exchange agreed to buy a majority stake in LCH.Clearnet Group for GBP463m ($613m)

- NRC deadline for issuing orders on safety improvements developed in year since radiation crisis at Fukushima, Japan

- No U.S. IPOs expected to price: Bloomberg data

- SATURDAY: China trade data for February

- SATURDAY: Kansas Republican presidential caucuses

- SUNDAY: Daylight savings time: Clocks spring forward in most of U.S. (Europe shifts on March 25)

EARNINGS:

- Hibbett Sports (HIBB) 6:30am, $0.56

- Ferrellgas Partners (FGP) 7am, $0.79

- Halozyme Therapeutics (HALO) 7:30am, $(0.15)

- Ann (ANN) 7:35am, $0.09

- Carnival (CCL) 9:15am, $(0.05)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Bulls Strengthen as Wagers Reach $131 Billion: Commodities

- Soybeans Climb to Five-Month High as Brazil Cuts Crop Forecast

- Oil Rises a Third Day on U.S. Economic Outlook, Greek Debt Swap

- India to Review Cotton-Export Ban as China Seeks Withdrawal

- China February Copper Output Rebounds From an 11-Month Low

- Gold May Rise as Low Interest Rates Boost Demand for the Metal

- Tocom to Discuss Alliance With CME Next Week, Ezaki Says

- Copper Traders Probably Added to Wagers That Prices Will Decline

- Palm Oil Surges to Nine-Month High on Speculation Reserves Fell

- Rare-Earth Bust Spurs Molycorp’s Biggest Takeover Bet: Real M&A

- Coffee Falls on Speculation Supplies Will Improve; Cocoa Drops

- Iran Oil Risk Threatens Peak Profit for Naphtha: Energy Markets

- Shipping Lines’ Asia-Europe Rate Rise May Fail: Chart of the Day

- Oil Rises on Greek Debt Swap, U.S. Outlook

- Copper Gains for Third Day on China Inflation, Industrial Output

- Rubber Futures Advance as China’s Inflation Eases: Tokyo Mover

- Chalco to Seek to Raise as Much as 8 Billion Yuan in Share Sale

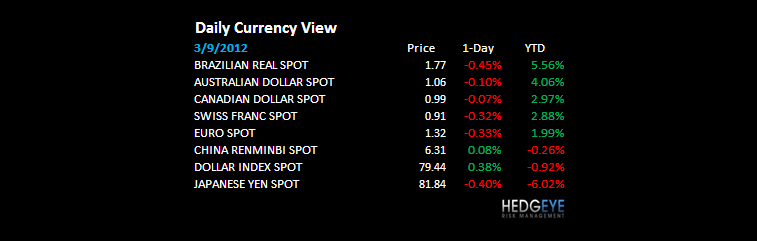

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team