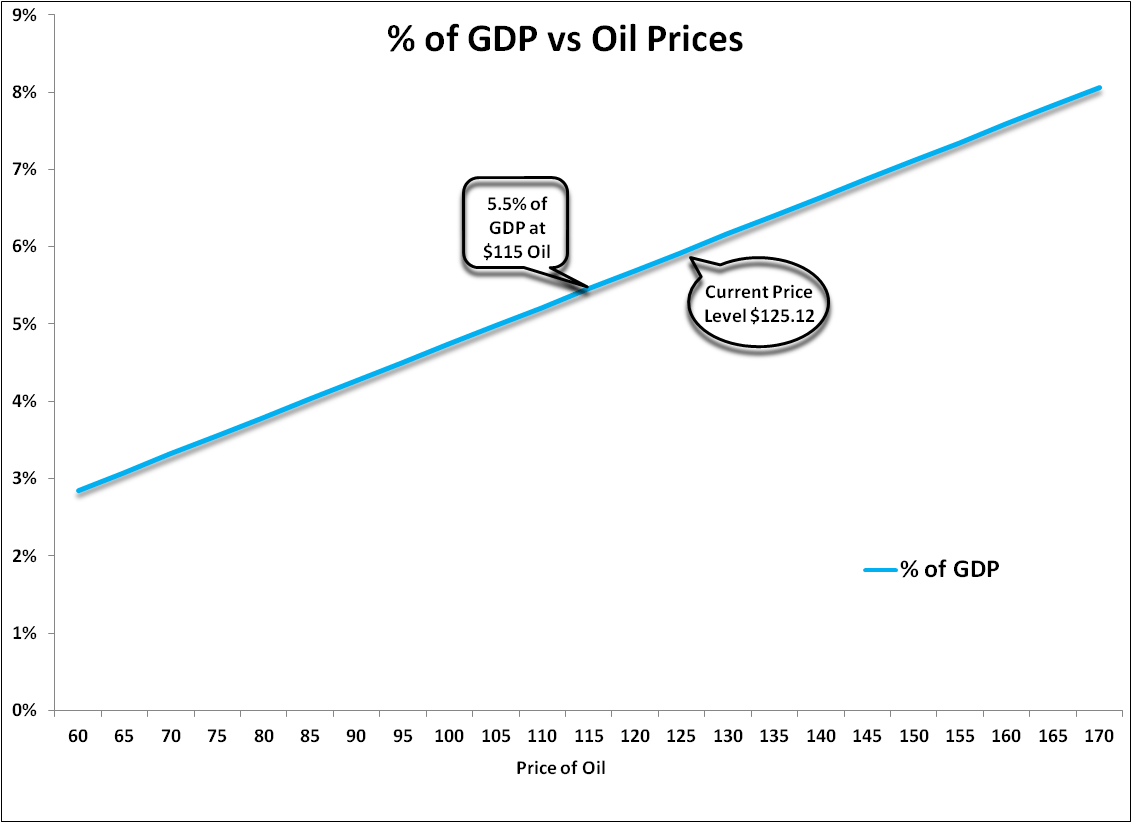

Conclusion: As consumption of oil eclipses 5.5% of GDP, it has historically had clear negative impacts on economic growth. This relationship is only further enhanced when the there is a “price shock”, so when oil moves up at an accelerated pace.

We recently stumbled upon a tweet that a major brokerage firm did an analysis of the correlation between GDP and the price of oil dating back to 1970 and found that there was literally no correlation. We’ve heard other pundits suggest that increasing oil prices are, perversely, good for growth. Or that increasing oil prices are, at the very least, indicators of improving demand and thus an improving economic outlook. Well, to put it mildly, we beg to differ.

In this note, we wanted to start with some recent history and a series of charts that highlight the impact of rapidly increasing oil prices on certain economic indicators:

- Brent Oil versus World Food Prices - In the chart below we show one of the derivative impacts of high oil prices, which is that these energy input costs also influence other commodity oriented products, in particular food. As this chart shows, oil and food prices have basically moved in lockstep over the past nine years. In fact, the correlation over the period is 0.81, so high, which isn’t totally surprising given that energy is a major input into the production of food. According the Bureau of Labor Statistics, the average U.S. consumer spends more than 10% of their pre-tax income on food. Energy is an input cost for food and naturally impacts the cost of food.

- Brent Oil versus Jobless Claims – The relationship between jobless claims and Brent oil is an obvious one if you look at the chart below. Specifically, a rapidly increasing price of oil is historically an accurate leading indicator for jobless claims. This occurred three times to note over the last two plus decades, in the late 1980s, in the late 1990s, and in late 2007.

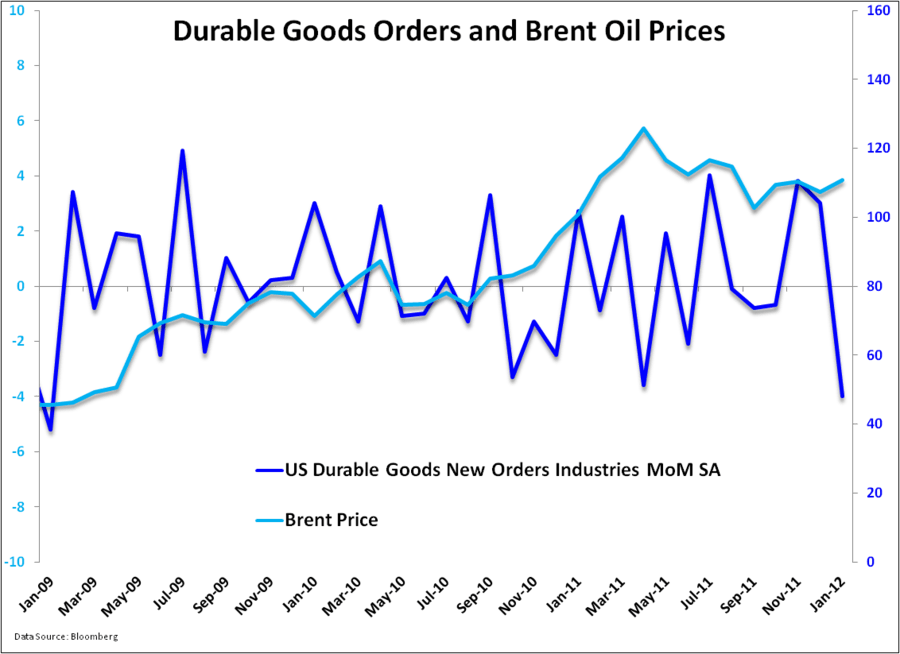

- Brent Oil versus Durable Goods Orders – The image below emphasizes that as the price of Brent has stepped up durable goods growth has decelerated. Durables goods are those goods purchased that are expected to last more than three years. In the most recent report, durable goods were down -4% year-over-year, with the biggest decline, not surprisingly, in civilian aircraft orders, whose key input cost is jet fuel. This negative correlation between durable goods orders declining and higher energy prices further supports the idea that consumers, and companies, are unwilling to make longer term, larger ticket investments in an uncertain input cost environment.

Charles Hall, Steven Balogh, and David Murphy did an analysis of the connection between the price of oil and when recession can be expected, examining the Minimum Energy Return on Investment (EROI). In their assessment, recession is likely to occur when oil amounts to more than 5.5% of GDP. Logically, this makes sense. Even based on the very tainted calculation of CPI, the average U.S. consumer spends 9% of his or her income directly on energy, with the majority allocated to gasoline. This obviously also excludes the derivative impact of increasing energy costs, such, as we noted above, the increasing costs of food.

Hall, Balogh, and Murphy also modeled out various scenarios of price increases, which we’ve highlighted in the chart below. They found that price shocks versus gradual increases in prices are much more detrimental to near term GDP growth. There models considered two types of price shocks. The first being a 10% price increase that either happens gradually over 5-6 quarters or that happens quickly within two quarters, and the same scenario only with a 50% magnitude price increase.

Based on all scenarios, the price of oil was a headwind to growth but if a price hike transpired in a shorter period of time it would lead to a more dramatic and an almost exponentially negative impact on GDP growth. As energy prices accelerate, it creates uncertainty related to the future, which slows decision making. We actually see this clearly in the durable goods orders chart above. Consumers slow their durable goods orders in conjunction with increasing energy prices because of both the price, but also increasing concerns related to future economic demand.

The chart directly below shows this long term impact of oil accelerating quickly and reaching 5.5% of GDP going back to 1970. While certain large investment banks may not have been able to measure the correlation, the relationship is quite obvious in the chart.

We actually did an analysis of the U.S. economy’s current situation relating to oil consumption. Based on the assumption that U.S. GDP is roughly $15.0 trillion, that the U.S. uses 19.5 million barrels of oil per day, and based on the current average price of Brent oil for the year at $116 per barrel. Employing that math, U.S. consumption of oil is at 5.51% of GDP, which is clearly in the danger zone. Now, obviously, our assumptions can be manipulated a little each way and WTI oil is trading at a lower price, but the key point is that we are at, or very close, to a ratio of oil to GDP of 5.5%.

In terms of whether a shock has occurred, the price of Brent has increased 26% from the start of Q4 2011 to today. Obviously, this isn’t a 50% ramp in the price of Brent, but it is in the realm of a price shock that negatively impacts growth as cited in the study above.

The simple fact is this: nine out ten recessions since World War 2 have been preceded by an increase in oil prices. Coincidence? Perhaps . . .

Daryl G. Jones

Director of Research