(Correction: Last sentance of opening paragraph was cut off in prior version)

We’re used to seeing VFC involved in M&A deals. It’s simply part of it corporate fabric and for good reason they have had a solid track record of success. But this morning VF is in a less familiar role as the seller of its John Varvatos brand. This is hardly a blockbuster deal (less than $100mm), but we like it for the following reasons:

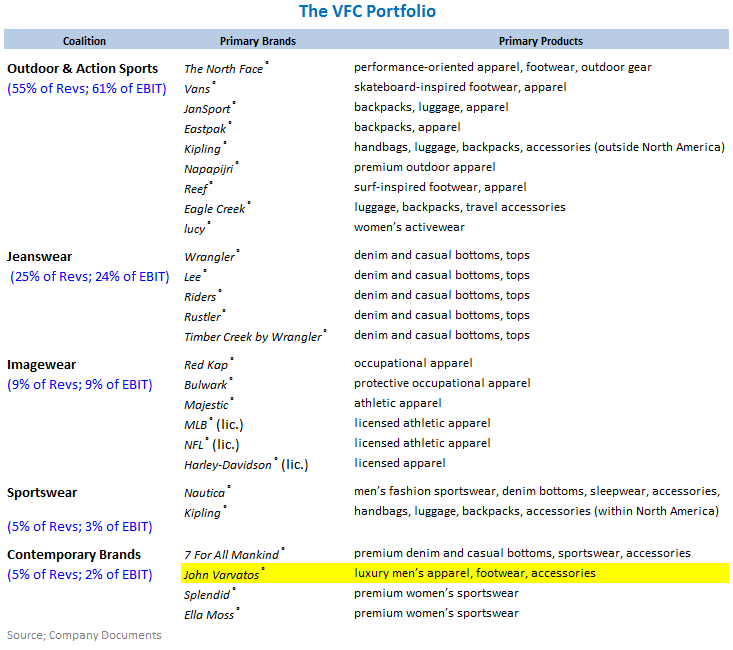

- There’s a lot of variety in the 26 primary brands that make up VFC’s consumer branded portfolio (see below), but Varvatos simply didn’t fit in. It’s a luxury men’s apparel brand that sells through luxury department stores like Barneys, Neimans, Bloomie’s, etc. in addition to its 10 free standing stores. VF has plenty of premium brands, but this was its only luxury brand. It was requiring incremental effort in order to maintain relationships with the department stores that VF wouldn’t have been dealing with otherwise – that’s now alleviated.

- We like the timing. While not a blockbuster deal (financial terms weren’t disclosed), VF is selling an asset in the luxury end of its portfolio just when luxury retail is shinning. As such, whatever the value the deal comes out to (we suspect around $100mm; over $100mm in sales at HSD margin), it’s not likely to have been at depressed multiples.

- It improves the balance sheet. The proceeds of this deal can be put towards reducing VFC’s debt-to-capital ratio. VF ended the year with a debt-to-capital ratio of 32% well below 40% where the company ended Q3 following the TBL acquisition. While slightly above plan (30% by year end), the company paid off nearly $900mm in debt during Q4 and can generate over $1Bn in FCF this year reflecting a 9% FCF margin despite ramping CapEx spending nearly 2x its historical rate in order to support continued growth, HQ relocation, new DCs, etc. With this level of FCF generation plus an additional ~$100mm from Varvatos, we expect VF to reduce its debt-to-capital ratio to the low-20s in-line with pre acquisition levels by year-end.

All in, this deal isn’t going to have a material financial impact, but the company is selling off a fringe asset in the least profitable segment of the business – it makes perfect sense. We like the stock here and the fact of the matter is that VFC continues to give the market reasons as to why it will likely never look cheap. Moreover, we think VF’s initial F12 outlook appears overly conservative, which shouldn’t come as a surprise to those that have followed this team.

Our model has VF growing EPS at a mid-teens rate over the next two years – without any stretch assumptions. Timberland growth alone gets us there, and we’re not making any heroic assumptions as to the use of VFC’s $1bn in free cash. With the stock trading at 13.9x our F13 estimate of $10.75, and about 10x EBITDA we can’t exactly call it cheap. But estimate revisions are likely to be headed up from here, and you generally don’t want to be on the wrong side of VFC when estimates are heading higher.

Casey Flavin

Director