THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

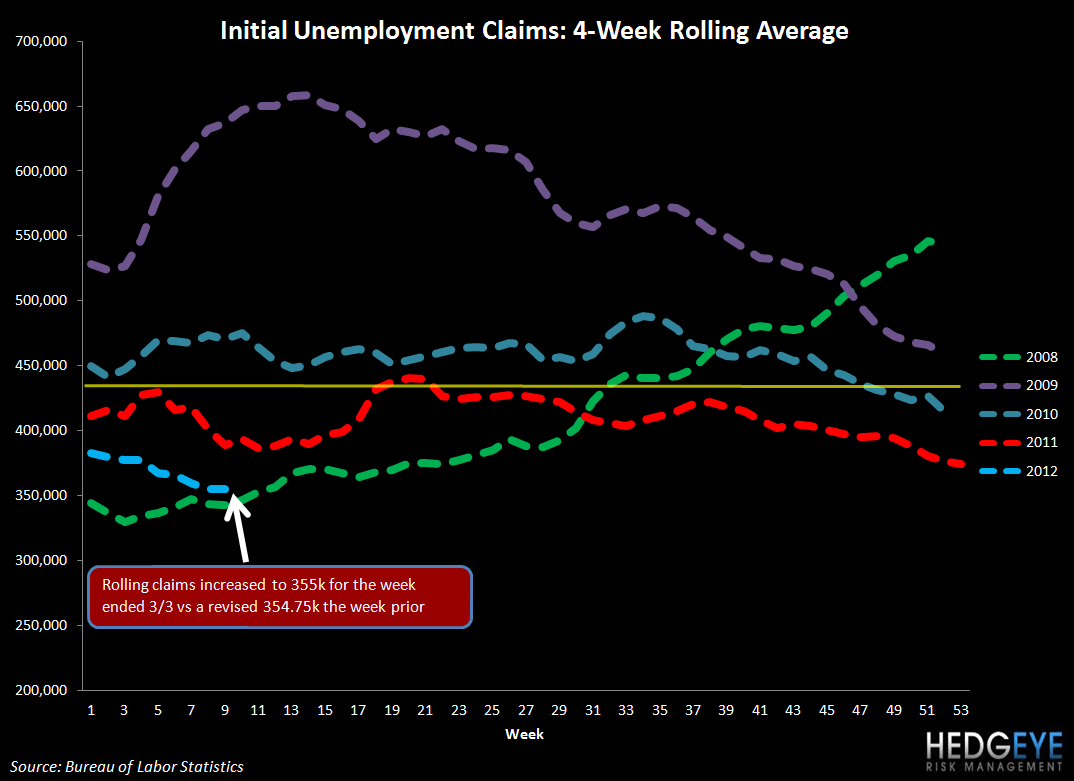

Consumer

Initial jobless claims came in at 362k versus 352k consensus for the week ended 3/3 and 354k during the week prior (revised up from 351k)

SUBSECTOR PERFORMANCE

QUICK SERVICE

MCD: McDonald’s reported sales of 11.1%, 4.0%, and 2.4% for the U.S., Europe, and APMEA, respectively. Consensus was looking for 8.7%, 6.8%, and 8.6%, respectively. Due to calendar shifts, the numbers include an adjustment ranging from approximately 3.1% to 3.4%. We will have a note up detailing our thoughts on MCD shortly.

PNRA: Panera is featured in the Wall Street Journal today stating that it will increase its media investment by 26% this year. "A lot of people think, if you do nothing, you will stay at zero. But the reality is, if you do nothing, you'll be at a negative," said Founder and Chairman Ron Shaich.

AFCE: AFC reported 4Q EPS of $0.24 versus $0.24 consensus.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

AFCE: AFC Enterprises gained 3% on accelerating volume.

CASUAL DINING

CBRL: Cracker Barrel continues to highlight gas prices as a potential risk going forward. Most of the other restaurant companies that have addressed the topic have been downplaying the impact of gas prices and highlighting the consumer handling current levels quite well.

BWLD: Sanderson Farms CEO Joe Sanderson said yesterday that there is no chance of the supply of chicken growing this year.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

DIN: Dine Equity bounced back after three consecutive down days.

Howard Penney

Managing Director

Rory Green

Analyst