US Dollar strength over the past week pressured commodity prices across the board with only chicken breast prices, of the commodities we monitor, posting a significant gain. Coffee prices continue to lead the way to the downside.

CONSUMER CALLOUT

Gas prices continue to move higher, gaining 50 bps over the last week despite Brent Crude prices declining -0.3% over the same period. Below are some recent comments from management teams regarding the impact of gas prices on their businesses. Clearly, given a sufficiently substantial rate of increase in gasoline prices, we will see an impact on restaurant companies’ top line trends.

WEN: Obviously, we're all watching gas prices carefully and – but consumers seem to quite honestly have digested that quite nicely.

BAGL: If employment continues to be positive, again from my perspective, I think that sort of offsets any impact that you might get – we might get on gas prices … That said, if employment tightens up or we don't see continuously positive momentum than longer-term, obviously, if we get a $5 gas price, that's one of those price points that hits overall.

CBRL: We think that given our susceptibility particularly to – in the summer travel season to potential increases in gasoline prices that it is appropriate to be suitably cautious about our third and fourth quarter traffic outlook.

DRI: Yes, I would say as we look back, we don't think the current levels, the $4 current gas prices, no longer represents sticker shock.

SUPPLY & DEMAND

Corn

SUPPLY

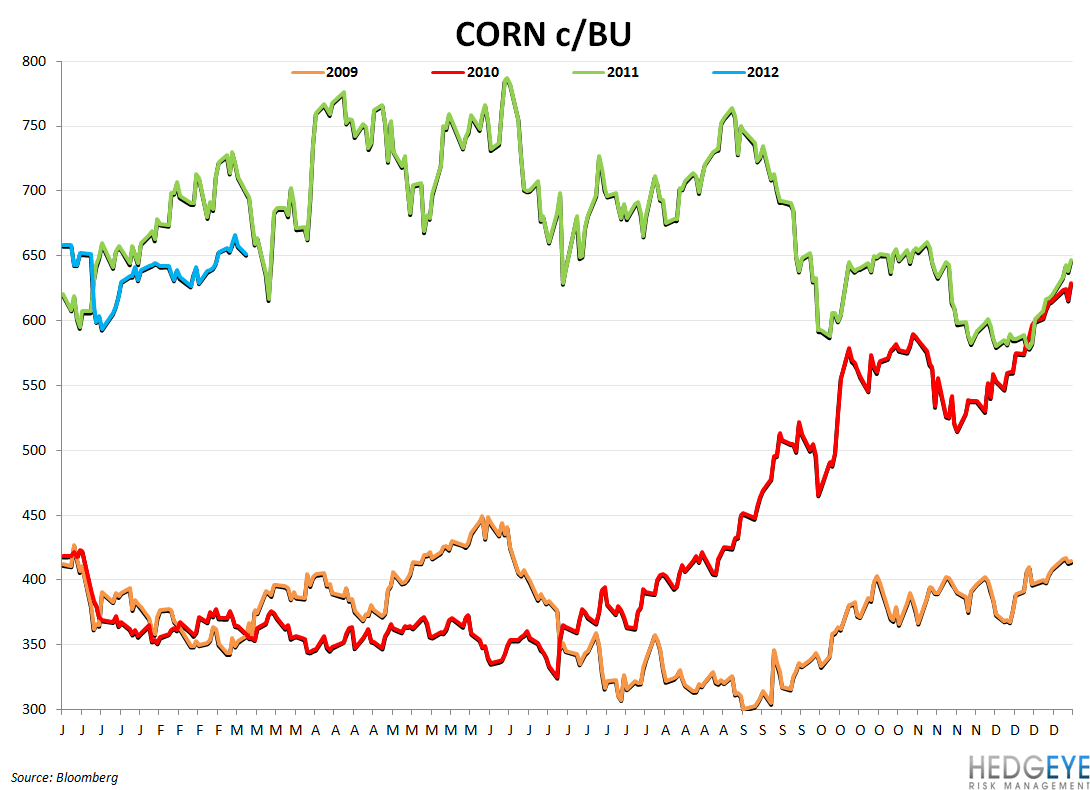

The USDA expects China’s corn production to drop 190 million metric tons in the year starting October 1st, down from 191.75 million metric tons the year prior. China’s corn imports are expected to remain steady at 4MMT.

DEMAND

Corn prices fell 2% today as commodity funds liquidated long positions ahead of the USDA crop production release at 8:30AM on Friday.

Speaking at the Bayer CropScience Ag Issues Forum in Nashville, Tennessee recently, William Lapp, grain economist with Advanced Economic Solutions stated that three factors have driven commodity prices to record levels: strong global economic growth in agriculture led by developing economies such as China, a weakening of the US dollar since 2002, and biofuels policy for grain use in the US. He believes that the “corn ethanol story is nearing the end” as the science lower cost cellulosic ethanol production progresses.

Wheat

SUPPLY

Concerns about a “glut” of wheat supplies overwhelming demand. Crops in key growing regions have seen favorable growing conditions

DEMAND

Wheat prices fell 3% today as commodity funds liquidated long positions ahead of the USDA crop production release at 8:30AM on Friday.

Soybeans

DEMAND

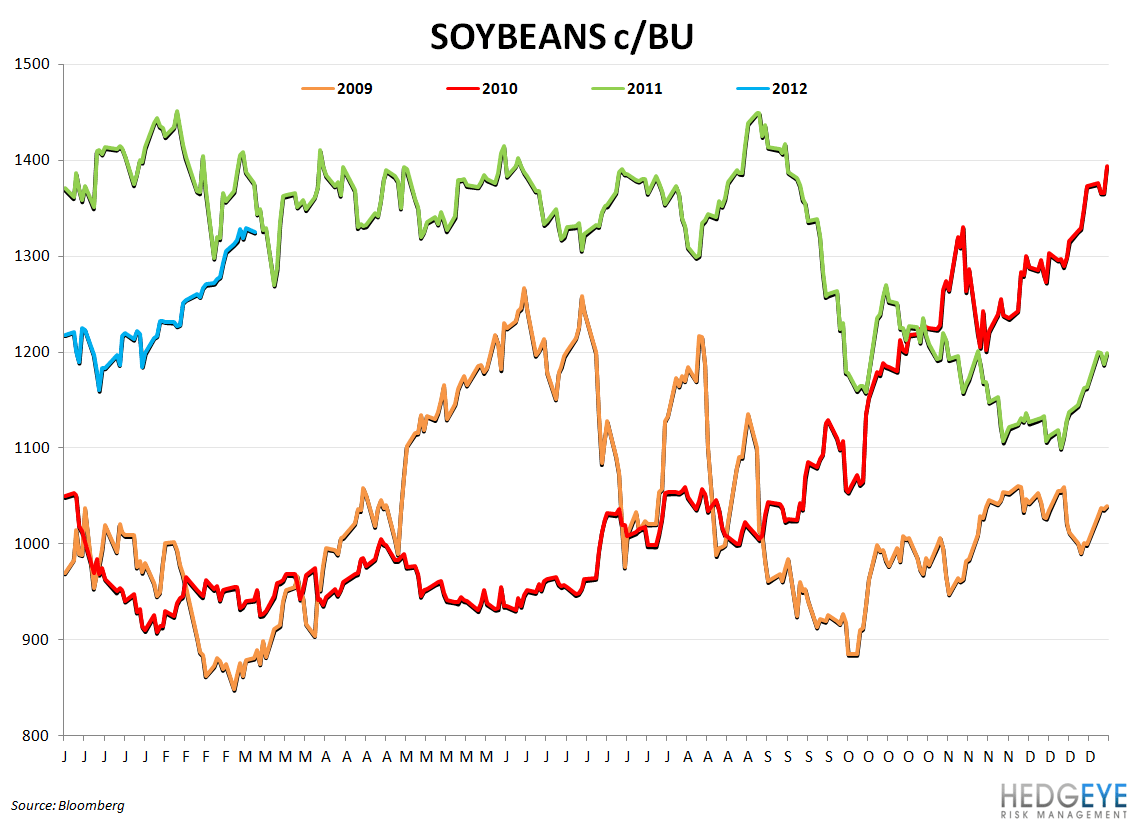

China’s rate cut in its forecasted economic growth rate on Monday has heightened concerns around the outlook for the world’s biggest buyer of soybean.

Beef

SUPPLY

The US herd remains depleted and the first steps for producers to develop a plan of action are to see how conditions are in the spring, forage growth following last year’s damaging drought, and financial and economic factors.

DEMAND

A fascinating article on CattleNetwork.com discusses the bright future of China’s beef market. According to consulting company Frost & Sullivan, China’s beef market is still in the primary development stage but it is likely to get more opportunities to grow with support from governmental policies.

Chicken

SUPPLY

Joe Sanderson, CEO of Sanderson Farms, said today that there is no chance of the supply of chicken growing this year.

Egg sets placements continue to contract at around the same rate, -5.4%, according to the Broiler Hatchery report released by the USDA today. This implies that supply will remain tight as the industry looks for more favorable business conditions before expanding production.

RECENT COMPANY COMMENTARY

Beef: Most companies are expecting beef cost inflation to be up mid-to-high single digits versus last year

TXRH: We expect approximately 8% food inflation in 2012, primarily due to higher beef costs…on the beef side we do have fixed price – pricing arrangements in effect for over 90% of our beef costs in 2012.

CBRL: To the continued pressure on ground beef prices and other commodities partly offset by lower average dairy and produce prices, along with benefits from our supply chain initiatives, we expect cost of sales to increase 60 basis points to 80 basis points over 2011 to near 26% in 2012.

RUTH: We project 2012 beef inflation to be between 5% and 8%. We currently have purchase agreements for beef representing approximately 30% of our needs through August of 2012, which represents an approximate 7% premium compared to the prior years.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans. Beef costs will be especially challenging due to protracted supply shortages, despite recent reductions in grain prices.

MCD: As we look at our guidance for 2012, we've built another mid-teens increase for beef, expecting that the dynamics in the marketplaces that we see, and are expecting, will continue.

DRI: U.S. beef production will continue decline though over the next 24 months, placing continued upward pressure on beef prices because of the slow economic recovery hamburger and value oriented beef, cattle beef are in high demand and can be priced accordingly by the packers. At Darden we purchased mainly tenderloins and other premium steakcuts, while we expect pricing for our beef products to increase by 12% our pricing has been tempered by consumers' resistance to record higher retail prices for premium stakes and the resulting shift to value oriented cuts and as you can see beef is approximately 14% of our cost basket … We have 75% of our beef requirements contracted for fiscal 2012 and 40% of the June to December usage under contract for fiscal 2013.

SONC: One item to note is that we recently locked in our beef contract for calendar year 2012… given the potential for beef costs going even higher, which there are a lot of reports out there that speculate that could happen, that we chose to go with making this more of a known quantity here, and the idea of having a set price for the next 12 months, we feel like would be good for our business, adds some predictability to the business.

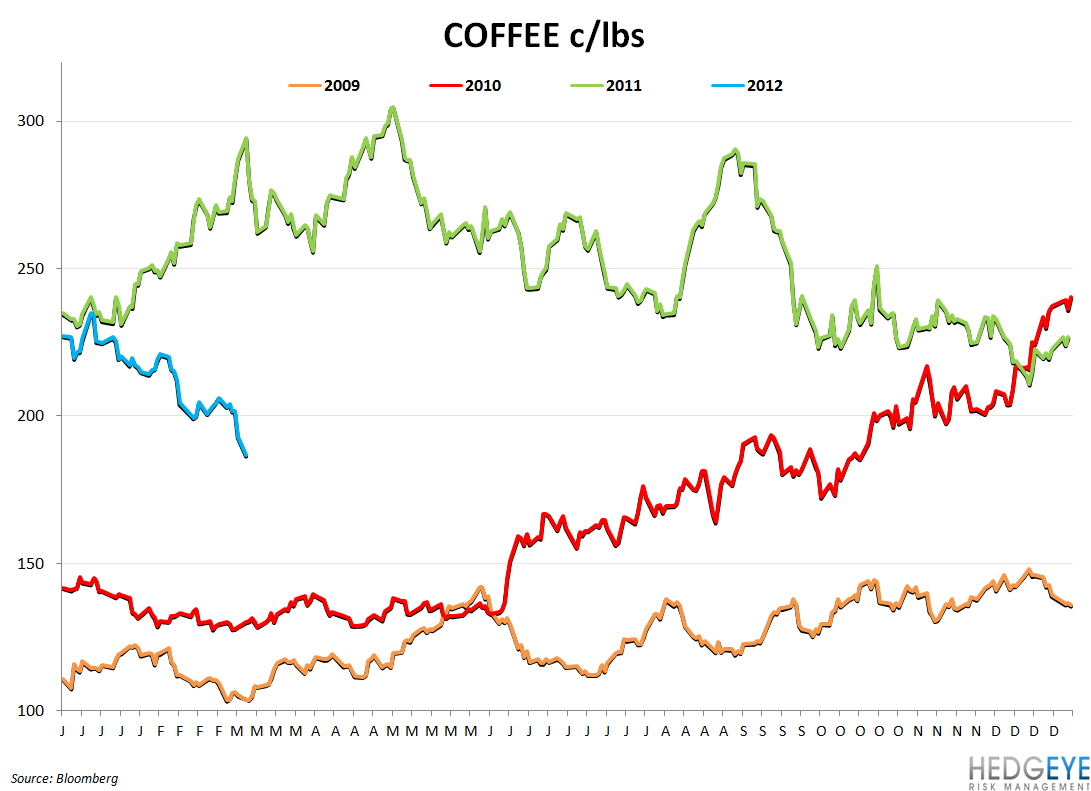

Coffee: Prices are now down -32% versus last year

PEET: We expect 2012 coffee costs to rise 12% instead of last year's 42%.

SBUX: We've taken advantage of the recent declines in the C-price to lock in more of our coffee needs for fiscal 2013. We now have six months of our fiscal 2013 requirements secured at costs moderately favorable to 2012.

Dairy: CAKE, DPZ, PZZA, TXRH and others could benefit from favorable cheese costs this year

TXRH: The volatility around that 8% estimate for food cost inflation would really be driven by produce and dairy. Those are of the biggest components that we float around the market, and that's about 15% to 20% of our total cost of sales.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Soybeans

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst