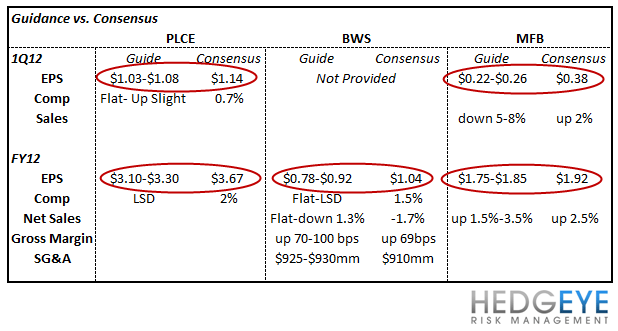

Among a flurry of retail earnings, three companies missed expectations and are guiding full-year 2012 earnings lower by average 12% below Street expectations. These aren’t rounding error shifts in expectations and highlight the increased volatility we think we’ll see through the 1H. The common callout here is that much like the rest of retail, inventory growth is outpacing sales growth. However, despite each company improving their respective sales/inventory spreads sequentially through more aggressive markdowns in Q4, there remains a high level of near-term uncertainty near-term in retail.

BWS: (Revs +4%; Inv +7%)

While sentiment on the name has improved over the last few quarters according to our sentiment monitor, today’s results suggest there is still plenty of wood to chop here as it relates to turning this business around. In addition, better results out of the PSS domestic business last week could suggest fewer stores will ultimately need to be closed dampering what we see as a potential tailwind for BWS over the intermediate-term.

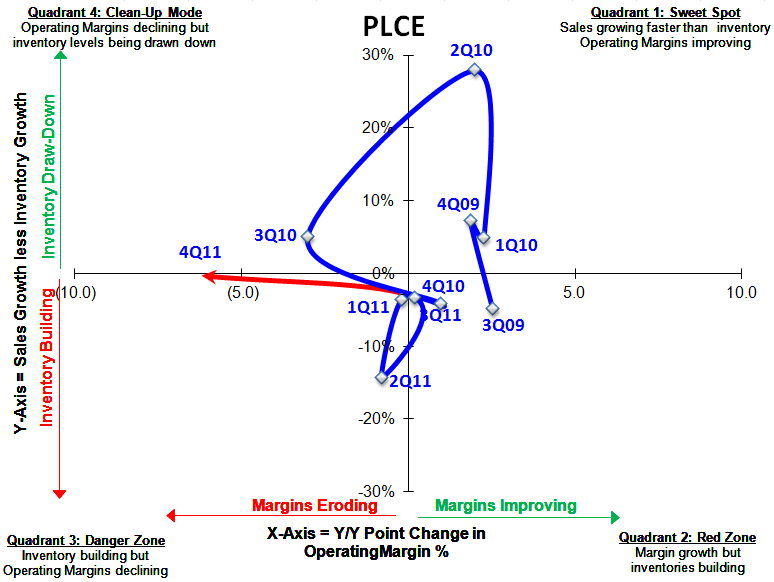

PLCE: (Revs -1%; Inv +1%)

Aside from blaming the quarter on poor weather, PLCE took aggressive markdown actions in an effort to clear inventory at year-end, but that clearly wasn’t the only factor given the company’s outlook for F12. Despite the positive SIGMA move this quarter that is gross margin bullish on the margin, continued promotional activity across the industry will continue to weigh on margins near-term.

MFB: (Revs +5%; Inv +27%)

Sales performance at the mid-tier was the weakest of MFB’s channels up +2.4% reflecting that discretionary spending for the most price sensitive consumer demographic remains under significant pressure.

Casey Flavin

Director