TODAY’S S&P 500 SET-UP – March 7, 2012

As we look at today’s set up for the S&P 500, the range is 23 points or -0.55% downside to 1336 and 1.16% upside to 1359.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2509 (-1923)

- VOLUME: NYSE 877.82 (24.29%)

- VIX: 20.87 15.62% YTD PERFORMANCE: -10.81%

- SPX PUT/CALL RATIO: 1.63 from 2.04 (-20.10%)

CREDIT/ECONOMIC MARKET LOOK:

USD – this is not a political comment, it’s a correlation one – Romney’s momentum rising/falling is starting to track the US Dollar Index and our new Hedgeye Election Index (Obama at 58.4% before Super Tuesday results). The back-test is meaningful – send us a note if you want the data series. US Dollar Index = +2% since Romney won Michigan/Arizona and you see what happened to inflation in the face of that (deflated, fast).

- TED SPREAD: 40.85

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 1.96 from 1.94

- YIELD CURVE: 1.68 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 7:00am: MBA Mortgage Apps, week of Mar. 2 (prior -0.3%)

- 8:15am: ADP Employment Change, Feb., est. 215k (prior 170k)

- 8:30am: Nonfarm Productivity 4Q F, est. 0.8% (prior 0.7%)

- 10:30am: DOE inventories

- 3:00pm: Consumer Credit, Jan., est. $10.45b (prior $19.308b)

GOVERNMENT:

- President Barack Obama visits Daimler truck manufacturing plant in Mt. Holly, N.C., delivers remarks on economy, 12:45pm

- House, Senate in session:

- House Financial Services subcommittee holds hearing on modernizing Securities Investor Protection Corp., 9:30am

- Senate Agriculture holds hearing on healthy food, nutrition as part of farm bill drafting, 9:30am

- House Energy and Commerce hearing on gasoline prices, 10:30am

- Congressional Progressive Caucus holds news conference on home foreclosures, 12:15pm

WHAT TO WATCH:

- Apple to host iPad event; watch for details on processing speed, display, pricing, effect on potential suppliers, 1pm

- Mitt Romney won 6 states including Ohio; Rick Santorum captured 3, signaling fight for Republican delegates may last months

- SocGen, Generali, UniCredit joined firms saying they would participate in Greece’s debt swap

- Sprint said to plan end to network-sharing deal with Falcone’s LightSquared

- Netflix explores putting film streaming service on cable systems

- JHL Capital Group says subsidiary of Clear Channel Communications Inc. improperly moved $656m to its parent

- Freddie Mac faulted with FHFA for oversight of loan servicers

- Calpers may cut assumed rate of return for 1st time since 2004

- Delphi investors can’t block Tokio Marine offer, judge ruled yesterday

EARNINGS:

- Fresh Market (TFM) 6 a.m., $0.38

- Children’s Place (PLCE) 6:30 a.m., $0.90

- Ciena (CIEN) 7 a.m., $(0.04)

- Brown-Forman (BF/B) 7:30 a.m., $1.01

- American Eagle Outfitters (AEO) 8 a.m., $0.35

- Laurentian Bank of Canada (LB CN) 8:54 a.m., C$1.26

- Hot Topic (HOTT) 4 p.m., $0.20

- Men’s Wearhouse (MW) 4:01 p.m., $(0.13)

- Express (EXPR) 4:01 p.m., $0.68

- H&R Block (HRB) 4:03 p.m., $0.07

- Semtech (SMTC) 4:30 p.m., $0.31

- Pall (PLL) 5:01 p.m., $0.74

- Canadian Western Bank (CWB CN) 7 p.m., C$0.55

- HudBay Minerals (HBM CN) Post-Mkt, C$0.15

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL - both Brent and WTIC continue to hold all 3 durations of support (TRADE, TREND, TAIL) in our model with Brent Oil’s refreshed risk management range = $120.83-123.98. It would have to break $118 (and WTIC break $102) for us to consider this a tailwind of Deflating The Inflation for the benefit of US Consumption.

- Boar Hunter Sets Sights on China After MF Global: Commodities

- Oil Rises on Forecast of U.S. Fuel Supply Drop, Jobs Increase

- Copper Swings Between Gains, Losses on Stocks, Slowdown Signals

- Soybeans Climb for Second Day as Chinese Demand May Strengthen

- Gold Gains in London as Drop to Six-Week Low Attracts Buyers

- Robusta Coffee Falls as Supplies May Increase; Cocoa Advances

- Palm Oil Seen Rallying 24% as World Cooking-Oil Supply Drops

- Australian Beef to Compete With Brazil, India as Demand Surges

- Jinchuan Plans to Raise Nickel Output, Look for Mines Abroad

- Goldman Takes Lead in M&A List Spurred by Natural-Resource Deals

- New Iraq Oil Terminal Starts Pumping Today, Minister Says

- California Nuclear Backlash Mounts After Japan Meltdown: Energy

- Netanyahu Sees Red Sea-Negev Rail Spurring China Trade: Freight

- China to Buy Corn If Prices Are Right, Reserve Chief Says

- India’s Singh Demands Urgent Review of Cotton-Export Ban

- Australian Wool May Tumble 8% as Slowing Economy Hurts Demand

- Copper Demand to Grow At Least 6% This Year, Tongling’s Wei Says

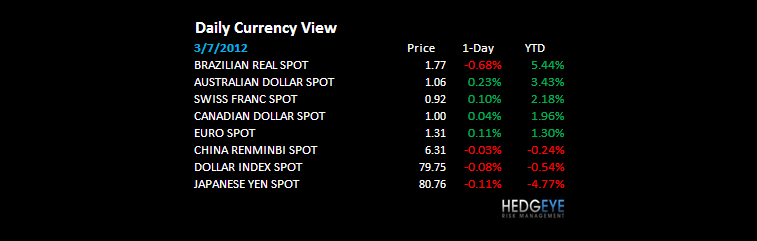

CURRENCIES

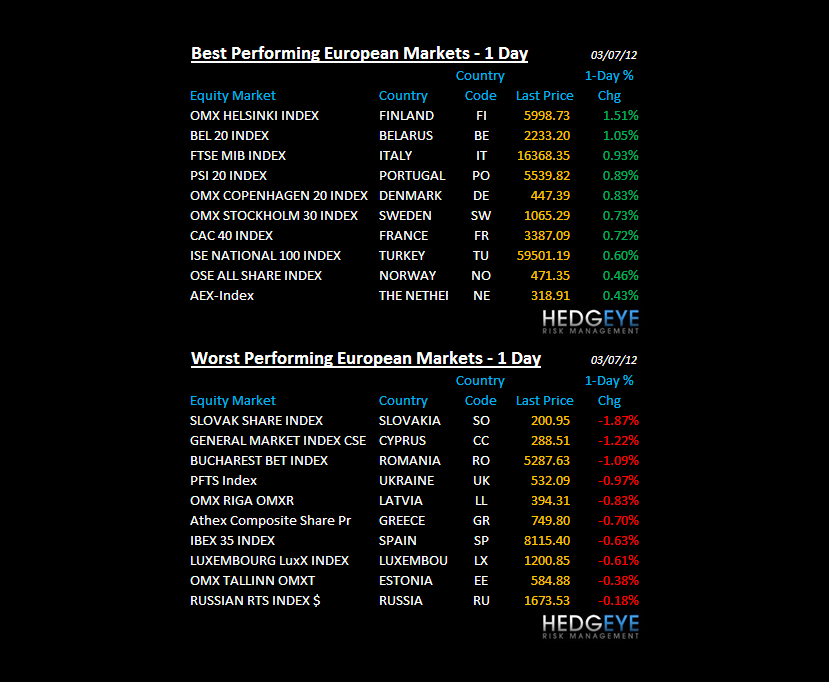

EUROPEAN MARKETS

SPAIN – never mind Greece, pull up a chart of the IBEX = straight down and, more importantly, this is the 1st major European stock market to snap its intermediate term TREND line (8499). Spanish Equities are down -4% all of a sudden YTD. Debt structurally impairs growth – these economies and markets are stagflating, big time – and even a Keynesian can’t stop gravity in perpetuity.

ASIAN MARKETS

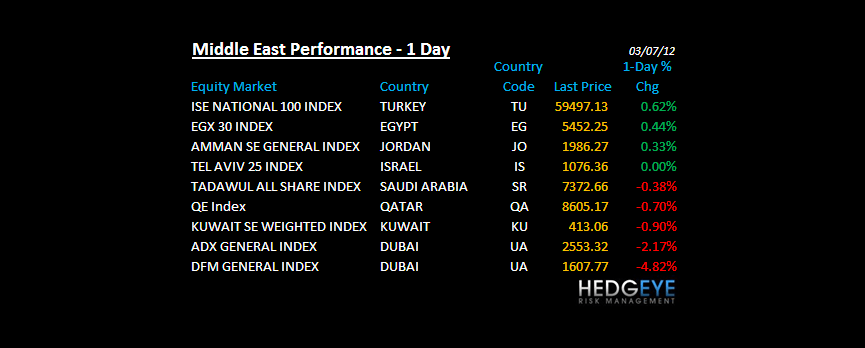

MIDDLE EAST

The Hedgeye Macro Team