The casual dining space, as we wrote 3/2, anchors heavily on the employment market. A rollover in headline initial jobless claims trends could lead the space lower. Here we highlight two names we see as being most at risk.

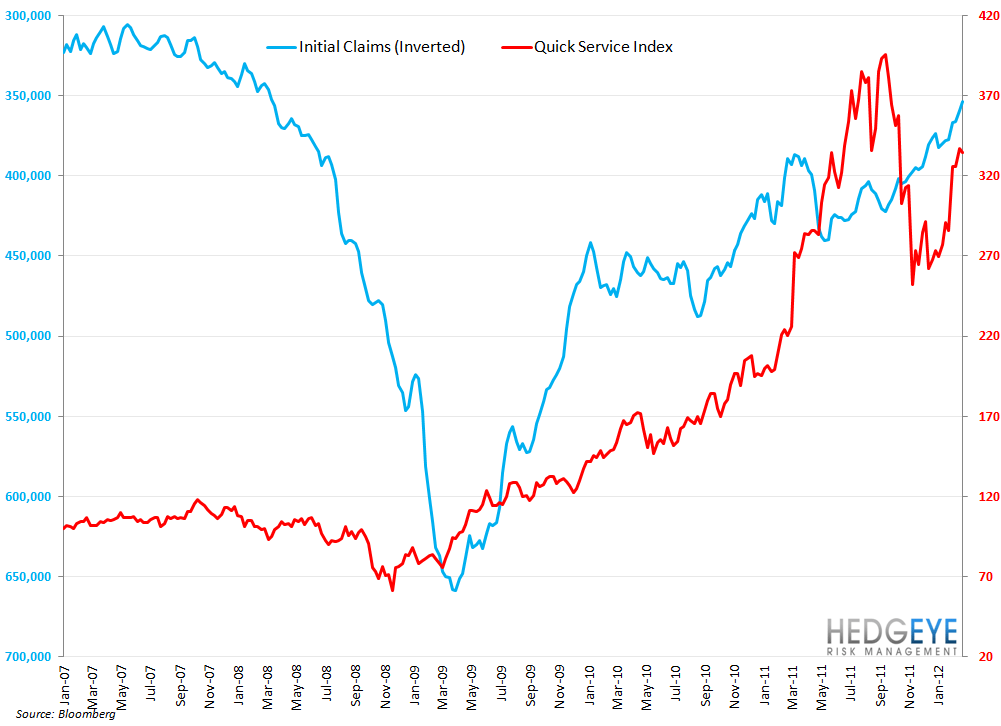

When positive or negative macroeconomic news that pertains to the restaurant industry hits the tape, casual dining stocks tend to move somewhat in unison. Similarly, a preannouncement of sales results significantly above or below consensus can lead to the whole group trading on the news. The risk of jobless claims rolling over as a tailwind related to a distortion in the labor statistics (see our 3/2 note for details) could be the next macro catalyst for casual dining. As the two charts, below, indicate, claims tend to be far more consequential for casual dining than quick service.

As our post on 3/2 outlines, the distortion in the seasonal adjustment factor stemming from the Lehman-related shock in initial jobless claims in 2008/09 began in week 36 of 2008. Looking at the correlation between jobless claims (inverted in the chart) and the stock prices of some of the casual dining names, we can get a sense for which companies may have benefited most from the distortion that our Financials team dubbed “the Ghost of Lehman”. As the Ghost of Lehman turns from tailwind into headwind, we can infer that those same companies that outperformed during 4Q and into 2012 could be at risk of underperforming over the next few months.

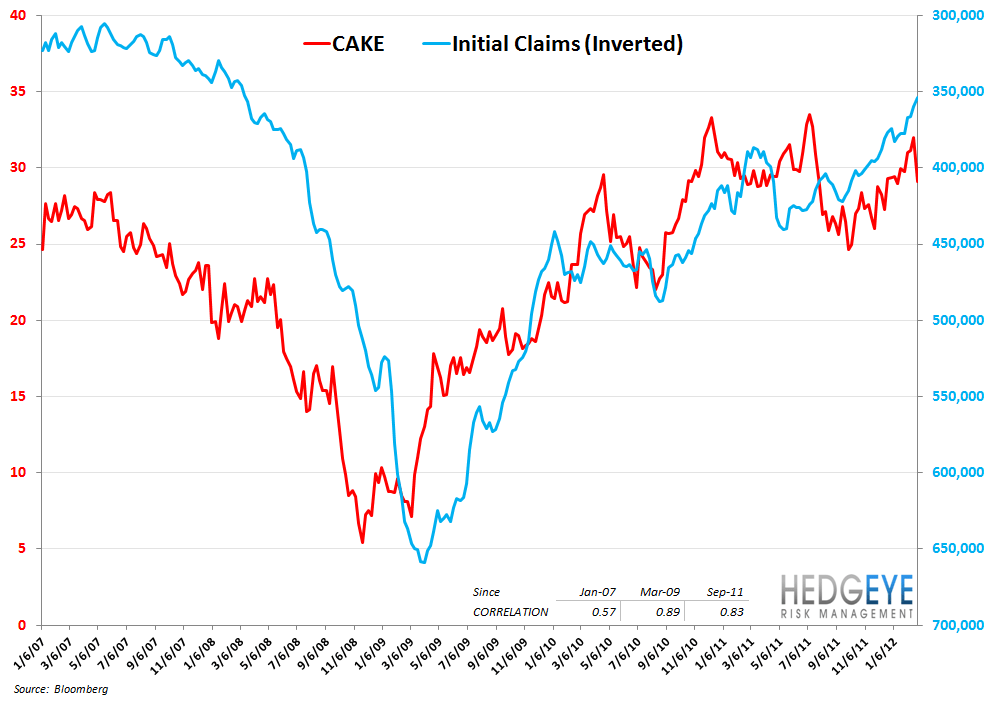

The first stock we would like to call out in this regard is Cheesecake Factory. The stock has moved largely in step with jobless claims’ improvement since March 2009 and, as the employment picture improved in 4Q11 and into 2012, the stock continued to gain. The correlation between initial jobless claims and CAKE’s stock price from 9/1/11 to present is -0.83. We highlighted yesterday that the ICSC Chain Store Sales Index data is hinting at a slowdown in CAKE’s top line in 1Q12. That is a metric worth monitoring as we progress through the quarter.

Cracker Barrel is a second stock that we would highlight as being particularly exposed to a meaningful reversion in jobless claims. The stock has appreciated greatly due to an improving top line but, given that the correlation between jobless claims and CBRL’s stock price is -0.95, we think that this stock could underperform in a scenario where employment trends soften. While many observers like Clarence Otis, CEO of Darden Restaurants, believe that the US consumer has become more resilient to elevated gas prices, if the trend in retail gasoline prices continues and the miles driven data in the U.S. trends lower, we believe that there could be an adverse impact on CBRL’s restaurant traffic. If gasoline prices can rise to, and remain at, prices close to $4 in the second quarter, we expect Cracker Barrel’s business to be affected.

It is also worth bearing in mind that Cracker Barrel’s advertising spending is being targeted on the second and fourth quarters of its fiscal 2012. This advertising spend helped the company outperform Knapp Track traffic trends during the same period. The company is guiding to its advertising spend in 3QFY12 being down year-over-year by $1-2mm and 4Q advertising year-over-year being flat. We are not expecting a significant boost, if any, from 4Q advertising on a year-over-year basis, certainly not as meaningful as the impact was in 2Q. If the employment outlook and gasoline prices become a negative factor for the stock, we believe there could be a substantial drop in same-restaurant sales at Cracker Barrel. Lastly, while weather lifted the entire industry over the winter months, we believe that Cracker Barrel may have been a larger beneficiary than some competitors but this is obviously difficult to prove.

Howard Penney

Managing Director

Rory Green

Analyst