Thursday has announcements from the ECB and BOE on monetary policy. We do not expect moves from either bank in interest rate levels or calls for additional non-standard measures or QE.

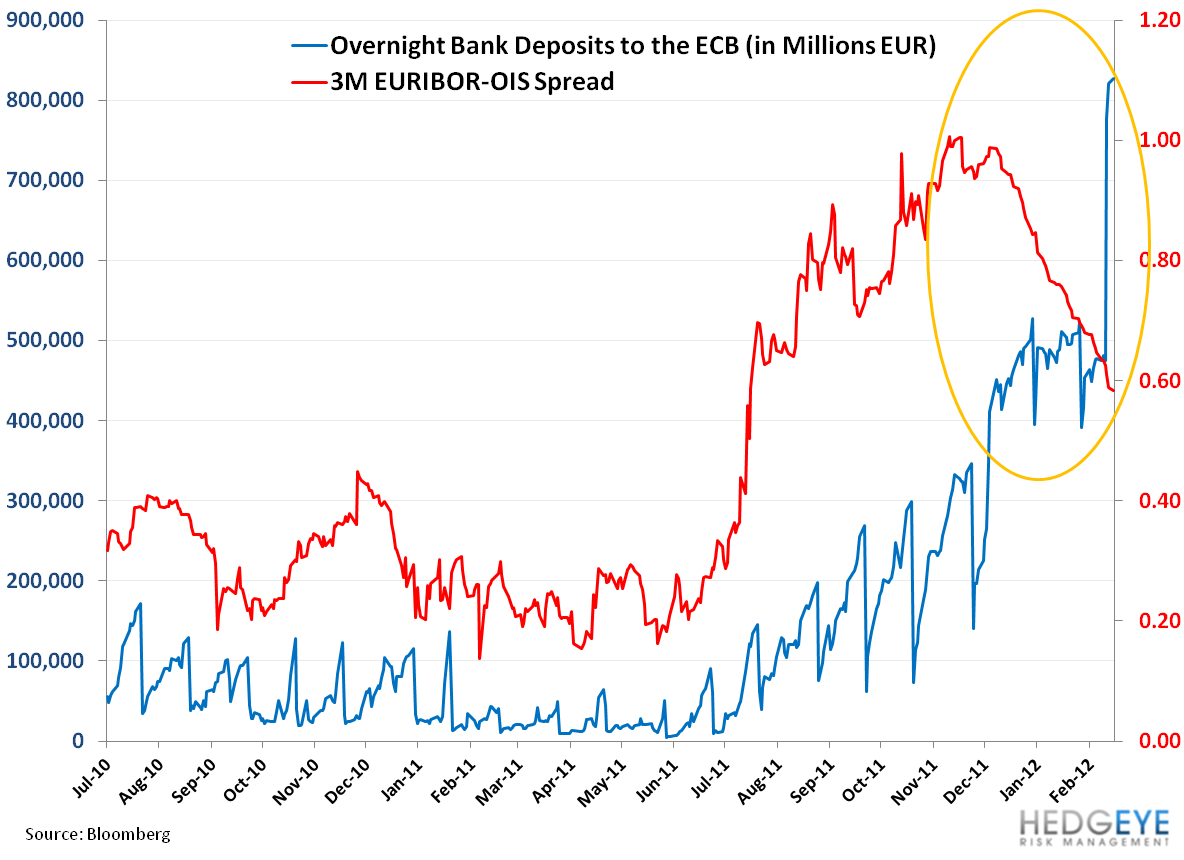

Although the ECB does need to cut its main interest rate as the region is dragged into recession, we’ll likely see Draghi remain on hold due to the timing of the 2nd 36 month LTRO (€529.5 billion) just last week and given that there’s plenty of runway left in 2012 to cut off the 1.00% bound. Another gauge that may weigh on inaction is the improvement in the EURIBOR-OIS spread, down 40% year-to-date to 58bps. However, as the chart below shows, a fair amount of the LTRO’s credit may be flowing to safety in the ECB’s overnight deposit facility (which is hitting new highs), and not to its intended audience of corporates and personal loans.

Remember, Draghi revised the language on the main outlook on the Eurozone economy in the last meeting (on 2/9) to “tentative signs of stabilization in economic activity at a low level” versus “substantial downside risks” in the previous report. We could see a return to his previous language.

Recent data since the last meeting that will weigh on the decision, and collectively hasn’t shown “tentative signs of stabilization”, includes:

Eurozone Q4 GDP -0.3% Q/Q vs 0.1% in Q4 2011

Eurozone M3 2.5% JAN Y/Y (exp. 1.8%) vs 1.6% DEC

Eurozone Unemployment Rate 10.7% JAN vs 10.6% DEC (highest since ‘97)

Eurozone CPI Y/Y 2.7% FEB (exp. 2.6%) vs 2.7% JAN

Eurozone PPI 3.7% JAN Y/Y (exp. 3.5%) vs 4.3% DEC [0.7% JAN M/M (exp. 0.5%) vs -0.2% DEC]

Eurozone Retail Sales 0.0% JAN Y/Y vs -1.3% DEC [0.3% JAN M/M vs -0.5%]

Eurozone PMI Manufacturing 49 FEB vs 48.8 JAN

Eurozone PMI Services 48.8 FEB vs 50.4 JAN

Eurozone Business Climate Indicator -0.18 FEB vs -0.21 JAN

Eurozone Consumer Confidence -20.3 FEB Final vs -20.7 JAN

Eurozone Economic Confidence 94.4 FEB (exp. 94) vs 93.4 JAN

Eurozone Industrial Confidence -5.8 FEB (exp. -6.9) vs -7 JAN

Eurozone Services Confidence -0.9 FEB (exp. -0.6) vs -0.7 JAN

------

The BOE should also maintain its 0.50% benchmark rate and £325 Billion bond purchasing program, following a £50 Billion increase last month. Fundamental data hasn’t shown signs of material improvement, though improvement on the margin, but again, there’s a lot of runway left in 2012 for monetary policy and still much uncertainty surrounding the direction of the Eurozone, the UK’s main trading partner.

In the last meeting, David Miles and Adam Posen pushed for £75 Billion in stimulus, and looser monetary policy, so we’ll have to wait for the minutes to see if the two had any more influence on the committee.

Recent data weighing on the decision includes:

UK Q4 GDP -0.2% Q/Q vs 0.6% in Q4 2011

UK CPI 3.6% JAN Y/Y (exp. 3.6%) vs 4.2% DEC

UK PPI Output 4.1% JAN Y/Y (exp. 3.7%) vs 4.8% DEC

UK PPI Input 7.0% JAN Y/Y (exp. 6.8%) vs 8.9% DEC

UK RPI 3.9% JAN Y/Y (exp. 4.1) vs 4.8% DEC

UK ILO Unemployment Rate 8.4% DEC vs 8.4% NOV

UK Jobless Claims Chg 6.9K JAN (exp. 3K) vs 1.9K

UK Avg Wkly Earnings 2.0% DEC Y/Y vs 1.9% NOV

UK Net Consumer Credit 0.1 B GBP JAN vs 0.0B GBP DEC

UK Mortgage Approvals 58.7K JAN vs 55K DEC

UK M4 Money Supply -1.8% JAN Y/Y vs -2.5% DEC

UK Nationwide House Prices 0.9% FEB Y/Y (exp. 0.3%) vs 0.6% JAN

UK PMI Manufacturing 51.2 FEB vs 52.0 JAN

UK PMI Services 53.8 FEB vs 56.0 JAN

UK PMI Construction 54.3 FEB (exp. 51.3) vs 51.4 JAN

Matthew Hedrick

Senior Analyst