Positions in Europe: Covered Italy (EWI)

Asset Class Performance:

- Equities: There were plenty of European equity performance swings this week, yet the top performer was Italy’s FTSE MIB, gaining 2.5% week-over-week, and Eastern Europe showed outperformance. Top performers: Romania 2.2%; Ireland 2.0%; Portugal 1.9%; Czech Republic 1.7%. Bottom performers: Ukraine -2.1%; Finland -1.2%; Switzerland -60bps; FTSE -40bps.

- FX: The EUR/USD is down -1.88% week-over-week. Divergences: PLN/EUR +1.45%, GBP/EUR +1.63%; RUB/EUR +1.38%, NOK/EUR +1.28%, CZK/EUR +1.07%; CHF/EUR -0.15%.

- Fixed Income: 10YR sovereign yields continued to move down in Italy and Spain week-over-week, while Greece and Portugal continued higher. Italy fell -53bps to 4.95% -- can the sub 5% level be held? Spain fell -16bps to 4.89%. Conversely, Greece rose 341bps w/w or 197bps Friday/Thursday to 37.65% and Portugal rose 101bps to 13.78%.

In Review:

Markets continue to make gains on short term hurdles—think Germany’s parliamentary approval of Greece’s second bailout on Monday and the 2nd 36M LTRO of €529 billion on Wednesday. To the latter example, while we think the LTRO is pumping in critical liquidity to the banking system (up from LTRO1 of €489), it cannot cure the solvency issues facing certain banks, nor is there any evidence that this cash is being lent through to corporates and consumers. Much of it still looks to be parked “safely” at the ECB’s overnight lending facility. Markets finished the week giving up some of their early week gains as reality set back in: there are many unanswered questions like if the fiscal union can really work when a similar program, the Stability and Growth Pact, failed so miserably in the past, and if the size and composition of the ESM and/or EFSF are sufficient.

For now, Eurocrats seem resolved to keep the existing Eurozone fabric in place, which is to say to prevent a “default” or exit of Greece and/or Portugal. ISDA, too has been playing ball, ruling that Greece has not had a "credit event" and credit default swap payments will not be triggered. Yet, as austerity takes hold and the region slips into recession, it will be increasingly difficult for governments to shave down bloated debt and deficit levels, and maintain sinking sovereign yields without the magic hand of the ECB. Noting these structural headwinds is nothing new, however this week emerged a great optimism in the press (at least pushed by the Eurocrats at their Summit this week) that the worst is behind us. We’ll take the other side. Witness a revision this week to Spain’s budget deficit, which last year reached 8.5% of GDP versus the original target of 6.0%.

All the while, the goalposts continue to change. This week’s highlight includes further details that the when the ECB swapped about €50 billion of Greek bonds for new longer maturity securities, the switch made the ECB senior to other investors, exempting it from a haircut of 53.5% that all other private holders must take. Obviously this last point will have a huge impact on gaining the critical 95% participation rate on the PSI. Should this rate not be reached, all calculations on a Greek plan to reduce its debt load will have to be revised higher. Back to square one--Yippie!

Another diverging theme this week is the stance of the UK (but also Czech Republic) that it does not want to be part of the fiscal compact. We’ll be touching on this subject in more detail, but it’s clear that to some extent there is an advantage to having one’s own currency, however the problem remains that that Eurozone is the largest trading partner for most European countries, so a slowdown is going to impact topline no matter the currency benefits.

And a continuing theme over the last week remains sovereign bond auctions issuing paper at lower yields than previous auctions. Notable call-outs this week include: Spain sold €1.06 billion due April 2014 with a yield of 2.06% vs above 6% in November 2011; France sold €3.92 billion of 10YR debt at an average yield of 2.91% vs 3.13% on February 2nd; and Italy sold €3.75 billion in 10YR bonds with an average yield of 5.50% versus 6.08% at a January 30th auction.

Finally, as we go into the weekend, it looks like a foregone conclusion that Putin will win Russia’s Presidential election on Sunday. This has severe implications for the modernization of Russia, a theme we’ll reserve for another post.

Call Outs:

France-

- Sarkozy gains in polls. With less than two months before the ballot, Sarkozy lags behind Hollande by 4.5 points in voting intentions, down from a seven-point gap a week earlier, according to an Ipsos SA poll for Le Monde and France Televisions.

- Hollande reiterates calls to renegotiate EU Fiscal Treaty and pledges to cap oil prices for 3 months if elected.

- Hollande floats idea of creating 75% tax bracket on super rich if he wins election.

Data Dump:

Eurozone M3 2.5% JAN Y/Y (exp. 1.8%) vs 1.6% DEC

Eurozone Unemployment Rate 10.7% JAN vs 10.6% DEC (highest since ‘97)

Eurozone CPI Y/Y 2.7% FEB (exp. 2.6%) vs 2.7% JAN

Eurozone PPI 3.7% JAN Y/Y (exp. 3.5%) vs 4.3% DEC [0.7% JAN M/M (exp. 0.5%) vs -0.2% DEC]

Germany GfK Consumer Confidence 6 MAR vs 5.9 FEB

Germany Retail Sales 1.6% JAN Y/Y (exp. 0.2%) vs 0.3% DEC [-1.6% JAN M/M (exp. 0.5%) vs 0.1%]

Italy Business Confidence 91.5 FEB (exp. 92.3) vs 92.1 JAN (falls to 2-year low on recession)

Italy Annual GDP 2011 0.4% (exp. +0.3%) vs 1.8% 2010

Italy Deficit to GDP in 2011 3.9% (exp. +4%) vs 4.6% in 2010

Ireland Property Prices -17.4% JAN Y/Y vs -16.7% DEC [-1.9% JAN M/M vs -1.7% DEC]

Greece Retail Sales -11% DEC vs -6.4% NOV

Portugal Retail Sales -8.5% JAN Y/Y vs -10.3% DEC

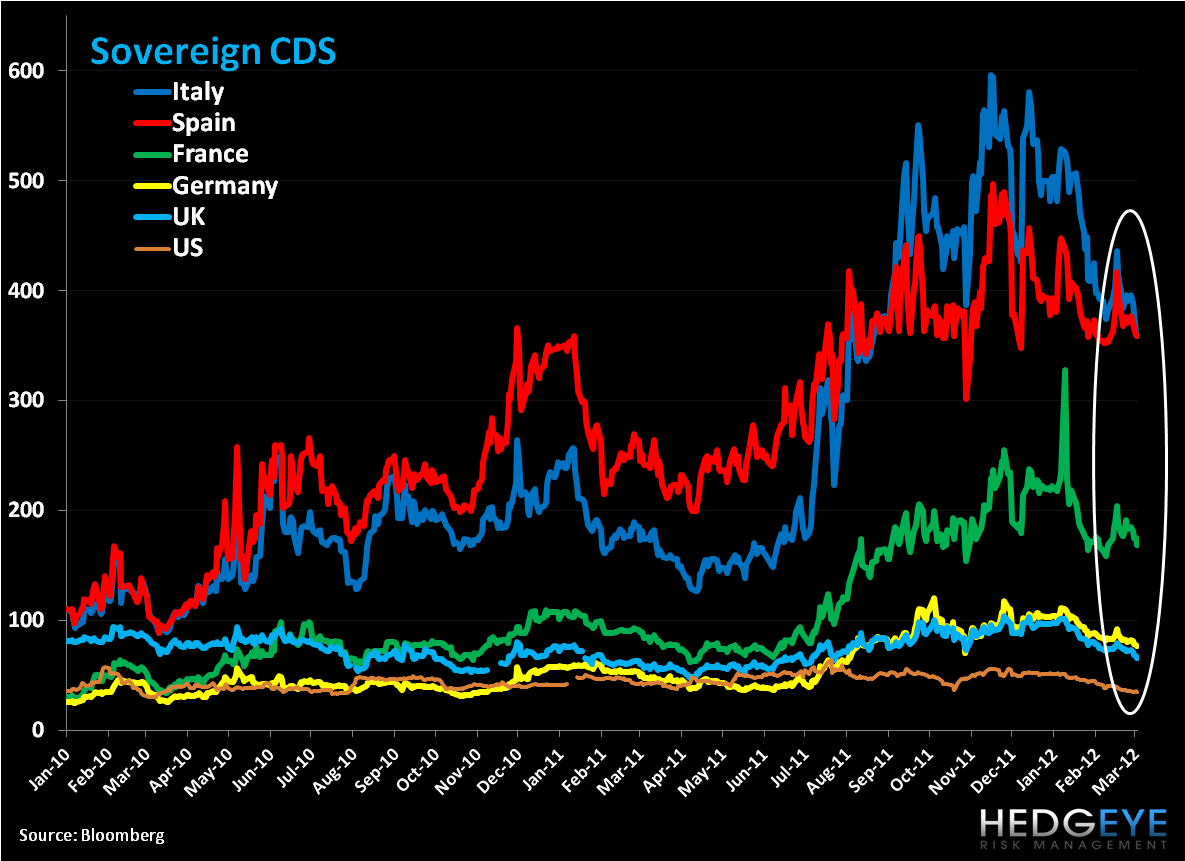

CDS Risk Monitor:

Similar to sovereign yields, Italy and Spain saw CDS declines on a week-over-week basis. Italy contracted -32bps to 359bps and Spain dropped -11bps to 359bps. Interesting, you’d have to go back to AUG 2011 to find Italian CDS at or below Spanish CDS. Portugal’s CDS rose the most at 57bps w/w to 1187bps, but is down -165bps m/m. Ireland rose 14bps w/w to 588bps.

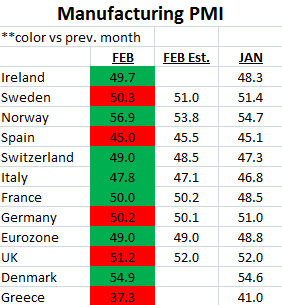

Manufacturing PMI:

The European Week Ahead:

Monday: Mar. Eurozone Sentix Investor Confidence; Feb. Eurozone PMI Composite and Services - Final; Jan. Eurozone Retail Sales; Feb. Germany and France Services PMI – Final; Feb. UK House Prices (Mar 5-9), PMI Services, Official Reserves, and BRC Sales Like-For-Like; Feb. Italy Services PMI; Jan. Italy PPI; Feb. Russia Consumer Prices (Mar 5-6), and Services PMI

Tuesday: Q4 Eurozone GDP, Household Consumption, Government Expenditures, and Gross Fix Cap – Preliminary; Feb. UK BRC Shop Index, and New Car Registrations

Wednesday: Jan. Germany Factory Orders

Thursday: Eurozone ECB Policy Meeting and Interest Rate Announcement; Jan. Germany Industrial Production; UK BoE Announces Rates; Feb. France Business Sentiment; Jan. France Trade Balance; Q1 France Non-farm Payrolls – Final; Dec. Greece Unemployment Rate

Friday: Feb. Germany Consumer Price Index - Final; Jan. Germany Exports, Imports, Current Account, and Trade Balance; Q4 Eurozone Labor Costs; Feb. UK GfK Inflation Next 12 Mths; Jan. UK Industrial and Manufacturing Production, PPI Input and Output, and NIESR GDP Estimate; Jan. France Manufacturing and Industrial Production, and Central Government Balance; Jan. Italy Industrial Production; Feb. Greece CPI; Q4 Greece GDP - Final

Extended Calendar Call-Outs:

20 March: Greece’s €14.5 billion Bond Redemption due.

April: French Elections (Round 1) begins to conclude in May.

29 April: Potential Greek Presidential Elections

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst