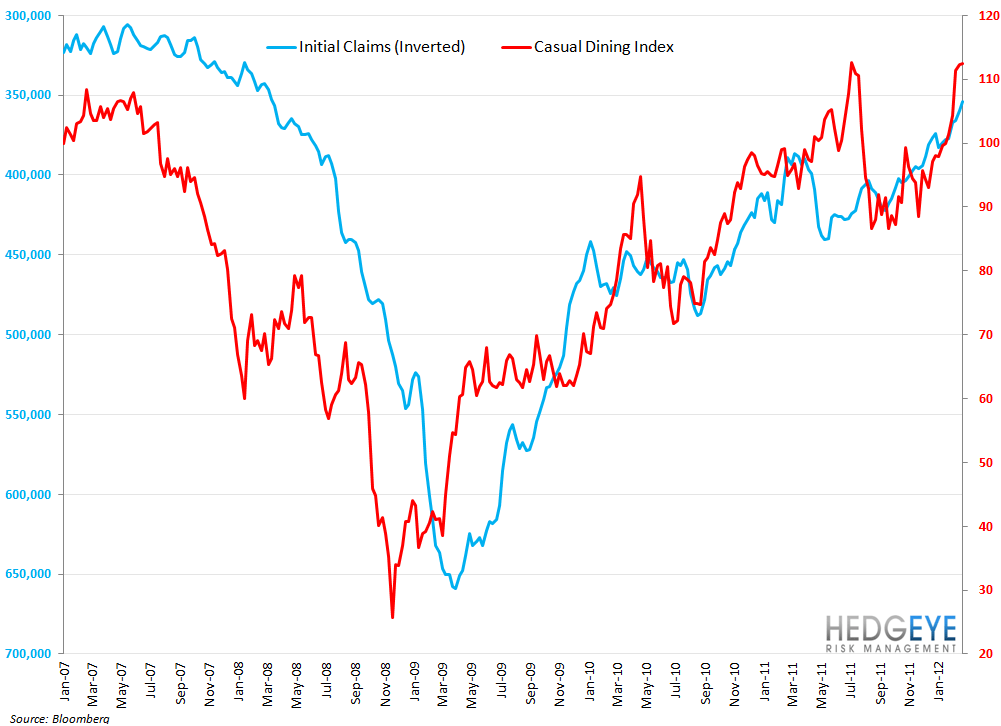

Two transient factors have been positively impacting restaurants’ top-line numbers recently. A distortion in initial jobless claims and – for certain companies – a favorable weather impact have been boosting revenues year-to-date.

The Hedgeye Financials team conducted an interesting analysis on initial jobless claims recently and, specifically, the implications therein of the Lehman bankruptcy-related shock to the labor economy in late 2008 and early 2009. We have been attempting to process what the read through of this analysis is for our space. Our conclusion is that the impact of a recently-favorable distortion to the headline seasonally adjusted initial claims data, coupled with the impact of favorable weather versus 2011, may have boosted top line numbers for many restaurant companies year-to-date.

The phrase given to the aforementioned initial claims issue by the Hedgeye Financials team is “The Ghost of Lehman”. They explained the impact of Lehman’s demise on the Labor Department’s construction of the seasonal adjustment factor. They write:

“Lehman's Ghost is a distortion in the seasonal adjustment factors that the Department of Labor is using to treat jobless claims arising from the shock in the series in late 2008 - early 2009. The Labor Department uses a five-year lookback in constructing its seasonal adjustment factor, which means that the '08-'09 shock continues to skew the data. Essentially, the seasonal adjustment sees the increase in claims in September 2008 - February 2009 and reads it as a seasonal factor rather than as a bona fide shock.”

To estimate the extent of the distortion from the seasonal factor on this week's data, we examined the YoY increase in NSA claims in February 2009 (+88%) and then backed out the average YoY growth from September 2008 to February 2009 (+60%). So the February 2009 growth is 28% above trend, YoY. This should be a rough approximation of the contribution of the seasonal factor from that year. Since the overall seasonal adjustment takes a five-year average, we divide this number by five to get a 5.6% increase. The conclusion is that this week's claims data is 5.6% understated. Instead of being 351k, it should really be 372k.”

If the analysis is correct, and we have passed the maximum benefit to restaurant stocks by way of the seasonal adjustment distortion, restaurant stocks’ outperformance could begin to reverse in the coming months. The Financials team contends that “from now through May, the understatement disappears…by July, the distortion reappears, this time as an overstatement, pushing claims higher still. From July through year-end, the distortion disappears, and the underlying trend will be reflected in the weekly data.”

There are clearly a lot of moving parts under the hood where the labor statistics are concerned and, while we are not stating that the jobs market is not showing some improvement, we would caution clients against over-exuberance. The claims data, distorted or not, are important drivers of restaurant stocks (albeit more so for casual dining) and to the extent that the claims data becomes marginally less positive as the seasonal adjustment becomes a headwind, we would expect to see a marginal slowdown in restaurant stocks’ performance (again, more so in the casual dining space).

The quick service and casual dining spaces have, year-to-date, outperformed the S&P 500 by 320bps and 718bps, respectively. Many names are up on a rope at these levels and, given the Ghost of Winter 2011 – the favorable year-to-date weather impact – combined with the possibility of the Ghost of Lehman distortion going away, we see a likely inflection to the negative side in sentiment around the top line over the next 3-4 months. We are cautious on the broader space at this point. The weather impact, which we discussed in our recent post “WINTER WONDERLAND”, is a wildcard currently given that the impact on different companies within our space will largely depend on their respective store bases’ geographic dispersions and disclosure from management as to the magnitude of any weather impact is not likely (until it is being lapped next year!). The Ghost of Lehman, however, will be far more visible if the analysis is correct, in the jobs data going forward.

While a more benign cost inflation outlook, improving sales trends, and increased pricing have fueled the space’s outperformance year-to-date, it is clear that investors could become spooked if favorable factors turn negative or, even, less positive. Given how lofty expectations have become, we believe that heading through 2Q we could see the top line begin to disappoint. We believe that the casual dining space is most at risk given its leverage to jobless claims and the outsized performance of that category year-to-date.

Howard Penney

Managing Director

Rory Green

Analyst