TODAY’S S&P 500 SET-UP – March 2, 2012

As we look at today’s set up for the S&P 500, the range is 12 points or -0.81% downside to 1363 and 0.07% upside to 1375.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1033 (-1982)

- VOLUME: NYSE 814.48 (-26.71%)

- VIX: 17.26 -6.35% YTD PERFORMANCE: -26.24%

- SPX PUT/CALL RATIO: 2.29 from 2.48 (-7.66%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 40.85

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 2.01 from 2.03

- YIELD CURVE: 1.73 from 1.74

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: ISM New York

- 1pm: Baker Hughes rig count

- 8pm: Fed’s Bullard speaks on U.S. economy in Vancouver

GOVERNMENT:

- President Barack Obama visits wounded service members at Walter Reed hospital in Bethesda, Md.

- House not in session, Senate in session

- Senate meets to resume consideration of surface transportation bill, 10am

WHAT TO WATCH:

- Yelp priced 7.15m shares at $15 each in IPO after offering them at $12-$14 apiece

- European leaders agreed to provide capital faster for planned permanent bailout fund

- Settlement talks continue over blame for Deepwater Horizon sinking, oil spill; trial will otherwise begin March 5

- Sands China profit beat estimates on jump in Macau casino sales; watch LVS

- President Obama said to have told Wall Street donors that Democrats can’t unilaterally stop accepting money from big- dollar PACs

- U.S. ITC may announce whether it will review judge’s finding that Motorola Mobility infringed one Microsoft patent and not six others, 5pm

- Washington state Republican presidential caucuses take place tomorrow

EARNINGS:

- Big Lots (BIG) 6 a.m., $1.74

- Exelis (XLS) 7am, $0.56

- Genesco (GCO) 7:35am, $1.67

- TransAlta (TA CN) 8:54am, C$0.24

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

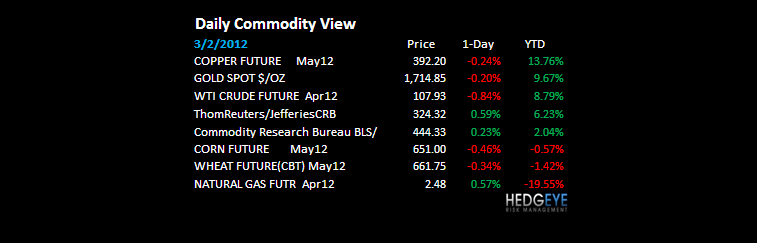

OIL – down 1% this morning but the lines that matter most continue to hold as the US Dollar’s bid remains fleeting. If Iran doesn’t send a missile somewhere soon, we’re going to need another line of storytelling out of Washington, fast. Immediate-term supports for Brent and WTI = $123.29 and 106.12, respectively.

- Copper Bull Streak Extends to Longest Since October: Commodities

- Oil Heads for Weekly Decline After Saudi Arabia Denies Sabotage

- Cocoa Falls as Rains May Boost Crops in West Africa; Sugar Rises

- Soybeans Set for Third Weekly Gain on U.S. Sales, Drought Woes

- Gold May Fall in London on Speculation Fed Will Refrain From QE3

- Copper May Decline as Shanghai Stockpiles Increase to a Record

- Bangladesh Plans to Import 100,000 Tons of Sugar From Brazil

- Palm Oil Posts First Weekly Decline in Four as Exports Weaken

- Economic Surprises Signal Rising Metals Demand: Chart of the Day

- Coal to Japan Seen Near Record in Xstrata Talks: Energy Markets

- Aluminium Bahrain Seeks to Keep Bribery Suit Against Alcoa Alive

- Palm Oil Imports by Pakistan to Slump as Strike Shuts Factories

- Oil Prices May Rise Next Week as Gasoline Gains, Survey Shows

- Oil Falls as Saudi Arabia Denies Sabotage

- Rubber Gains to 5-Month High as U.S. Data Boosts Demand Outlook

- Saudis Suffered No Sabotage to Oil Facilities, Ministry Says

- Russia Plans $8 Billion Siberia Investment to Boost Coal Exports

CURRENCIES

EUROPEAN MARKETS

RUSSIA – the most popular man with Putin right now has to be The Bernank. Putin gets paid in Petro-Dollars, and with the Petro straight up, Dollar straight down, what more could our comrade want heading into this weekend’s election? Russia +25.2% YTD. That’s probably a depression or deflation signal, or something.

ASIAN MARKETS

YEN – this is easily the most recognizable downward dog pattern that consensus still isn’t talking about. Straight down again (-0.46%) vs the USD this morning, the Japanese are about to engage in selling more sovereign debt than even the Americans and Europeans could. We have a 100 slide deck and conference call on Japan at 11AM EST today if you want to get up to speed on it.

MIDDLE EAST

The Hedgeye Macro Team