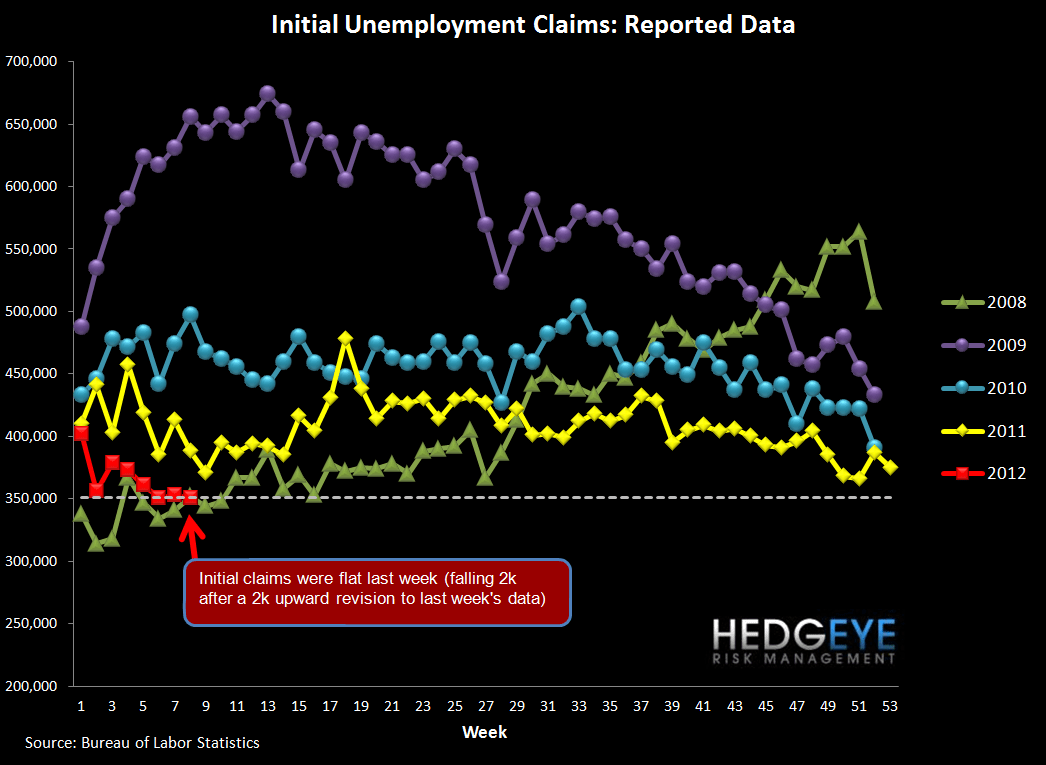

Initial Claims Flat for the Third Week

The headline initial claims number came in flat, falling 2k after the upward revision to the prior week's data. Rolling claims fell 5.5k to 354k. On a non-seasonally adjusted basis, claims fell 15k to 332k.

In our note last week, we walked through a quantification of the distortion in seasonal adjustment factors arising from the Lehman shock in 2008. Because the Labor Department uses a five-year lookback to create its seaosnal adjustment, the 2008 shock is still percolating through the data.

The seasonal distortion plays out as follows. Claims are understated in the last weeks of February by the largest amount. From now through May, the understatement disappears. Absent an underlying trend in the series, this effect would drive claims higher by about 20k over the course of the next three months. By July, the distortion reappears, this time as an overstatement, pushing claims slightly higher still. From July through year-end, the distortion disappears, and the underlying trend will be reflected in the weekly data.

2-10 Spread

The 2-10 spread tightened 3 bps versus last week to 167 bps as of yesterday. The ten-year bond yield decreased 3 bps to 197 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky