This note was originally published at 8am on February 16, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We don’t want a society where when you lose your job you live in a trailer home, like in the U.S.”

-Nicholas Sarkozy

Over the course of my 13 years in this business, I’ve seen bubbles in Tech, Housing, and Keynesian Economics. Now the bubble in dumb politicians has gone global.

I know some people don’t like being called names. That’s why I call those ones in particular names. Sometimes, if you want to creatively destruct dogmas, you just have to pick a fight. That’s pretty easy to do with the left leaning leader of France.

Ironically enough, American politicians are now competing with the Japanese and Europeans on who can lean the most left in market interventions. When I left Canada in 1994, I never would have thunk I would see the day. It’s sad to watch.

Back to the Global Macro Grind…

I didn’t short the SP500 yesterday at 11:58AM (1355) because I wanted to pick a fight – it’s because my process had it immediate-term TRADE overbought. The process obviously isn’t perfect, but it is repeatable – and when I get something right, I know why.

Yesterday I wrote about being wrong and how I deal with my own issues. If you couldn’t tell, I have a lot of issues. My goal in life is to improve upon them. In addition to President Sarkozy, politicians who understand Keynesian Policies To Inflate are having some issues of their own this morning:

- JAPAN – the Yen continues to go down in a straight line this week, down another -0.54% this morning to $78.80 vs USD

- SPAIN – the Spaniards are having a tough time selling pig paper at lower yields (2.3B EUR in 2015 bonds priced at higher yields)

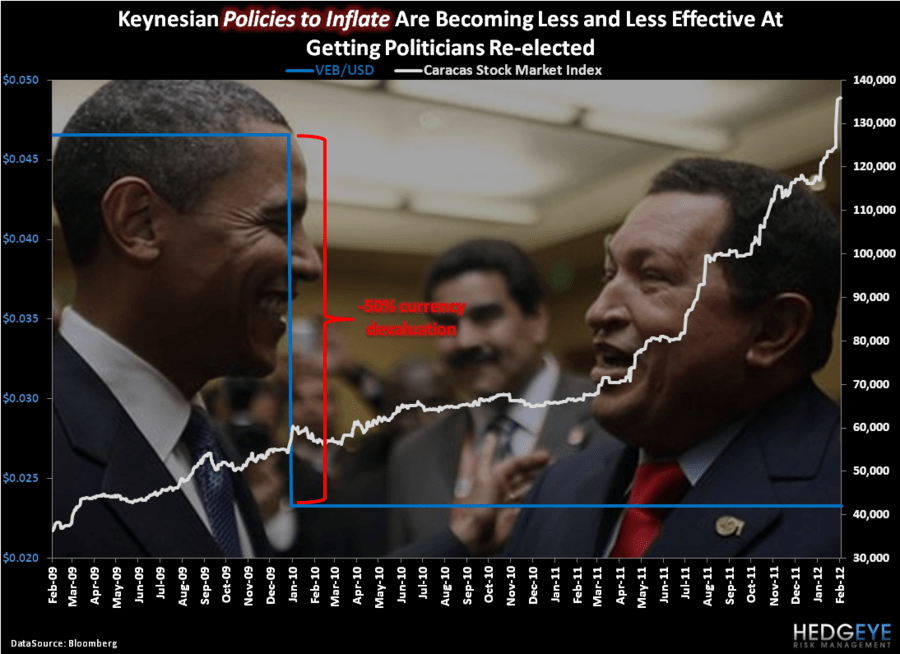

- VENEZUELA –the Latin American FX debaucherer, Hugo Chavez, has fallen behind his Presidential challenger, big time

Venezuela?

Yeah, I know you probably wanted someone to write to you about Greece or whatever a 12-month late Ratings Agency is thinking about what they should have warned you about 12 months ago…

Instead, consider the following about the Hugo Trailer Homes model (see chart):

- Collapse the currency

- Inflate the stock market

- Lose the Election

Last year, when almost 90% of country stock markets closed down for the YTD (sorry to remind everyone), Venezuela was up +79.1%. That was the best performing stock market in the world by a Madoff mile.

Instead of made for TV “rallies” on no volume (or inflows from The People), what does a Policy To Inflate get you in Venezuela, Wisconsin, or Milan?

Angry (and hungry) people.

We’ve never seen a $100 handle on the price of oil (pick your vintage – Brent, WTI, etc.) not Slow Global Growth. Now maybe the Sell-Side Strategists who told you to buy everything Global Equities on green last February are telling you it’s “Different This Time”, but I’m on the other side of that trade.

I can see exactly where perma-bulls are coming from – their risk management models have not changed. And that’s actually sad too. One of the many globally interconnected reasons I shorted SPY at 1355 instead of chasing it yesterday was that US Industrial Production Growth for January was reported at 0.00%.

Nice round number – and while The Bernank might like the ring of the zero percent thing, stock and commodity markets did not:

- US Industrials (XLI) were the worst performing S&P Sector of the day at -1.3%

- Dr Copper snapped its immediate-term TRADE line of $3.88/lb and is down another -1.1% this morning

- SP500 closed down for the 3rdday in the last 4

These are simply the facts. And I get paid to report them to you in the order that they are received.

Last week, I wrote a note telling you what I thought you should focus on instead of Greece:

- Japan’s Sovereign Debt Maturity Spike in March

- China’s Growth Slowing Sequentially (China’s Foreign Direct Investment reported overnight was down y/y!)

- The almost hyper global inflation/deflation relationship driven by policies driving the US Dollar

The bad news is that most of this is becoming new news to consensus. The Good news is where this all started is beginning to end – the US Dollar stabilizing in the last 48 hours is the most bullish fundamental factor I have in my notebook this morning.

While that may not be good for the guy who bought the Basic Materials ETF (XLB) or Freeport McMoran (FCX) at last week’s top, Deflating The Inflation is great for all my friends who grew up in Trailer Homes.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, US Dollar Index, Spain’s IBEX, Shanghai Composite, and the SP500 are now $1714-1754, $116.79-119.79, $1.30-1.31, $79.01-79.73, 8444-8653, 2340-2389, and 1339-1354, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer