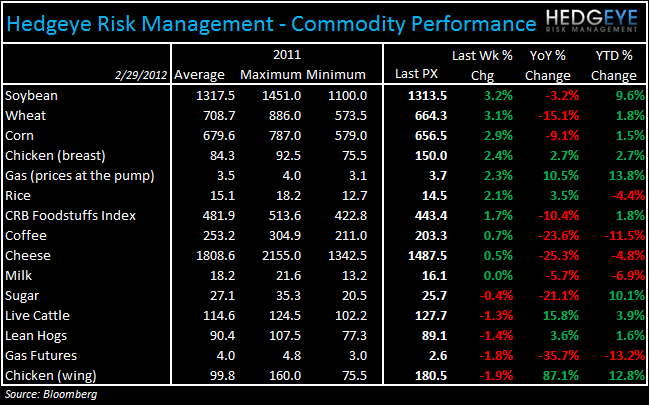

Grains were up over the last week while beef declined. The trend in beef prices is still positive, however, as grocery store beef prices re-set record highs and global demand for U.S. beef remains strong. Here is a table showing the trends for the commodity monitors we track. At the end of the post, we supply stacked line charts of each of the commodities below for the last few years of data.

CONSUMER CALLOUT

Gas prices continue to rise, the question is at what point it really starts to impair consumption if it has not already. Last Friday in NYC, Darden CEO Clarence Otis said, “I would say as we look back, we don't think the current levels, $4 current gas prices, no longer represents sticker shock. And so as we think about this improving trend that the industry has been on over the last two years that trend has been despite the fact that we've seen these levels before. And so, I think people especially at the income demos that we're talking about $4 … we don't see huge effect. We didn't see it the last time, which I think was roughly 12 months ago if I am not mistaken.”

SUPPLY AND DEMAND

Grains: Wheat and corn prices gained over the past week as shortfalls elsewhere in the world have led to investors buying U.S. grains

Corn: U.S. corn futures are trading strongly on growing export demand… Many dynamics are currently being factored into corn prices including gas prices, gasoline consumption, and ethanol margins, the U.S. Dollar, and demand from China… The USDA’s projections indicate that U.S. corn prices at the farm level are expected to average $5 a bushel for the ‘12/13 marketing year… The USDA’s calculations suggest that a combination of higher yields and higher acreage will generate an almost 2 billion bushel increase in US corn production come fall.

Wheat: Supplies are at record levels… prices are down -15.1% year-over-year despite gaining 3% this past week as concerns mounted around reduced acreage in Ukraine and freeze damage to wheat in Eastern Europe, Ukraine, and Southern Russia.

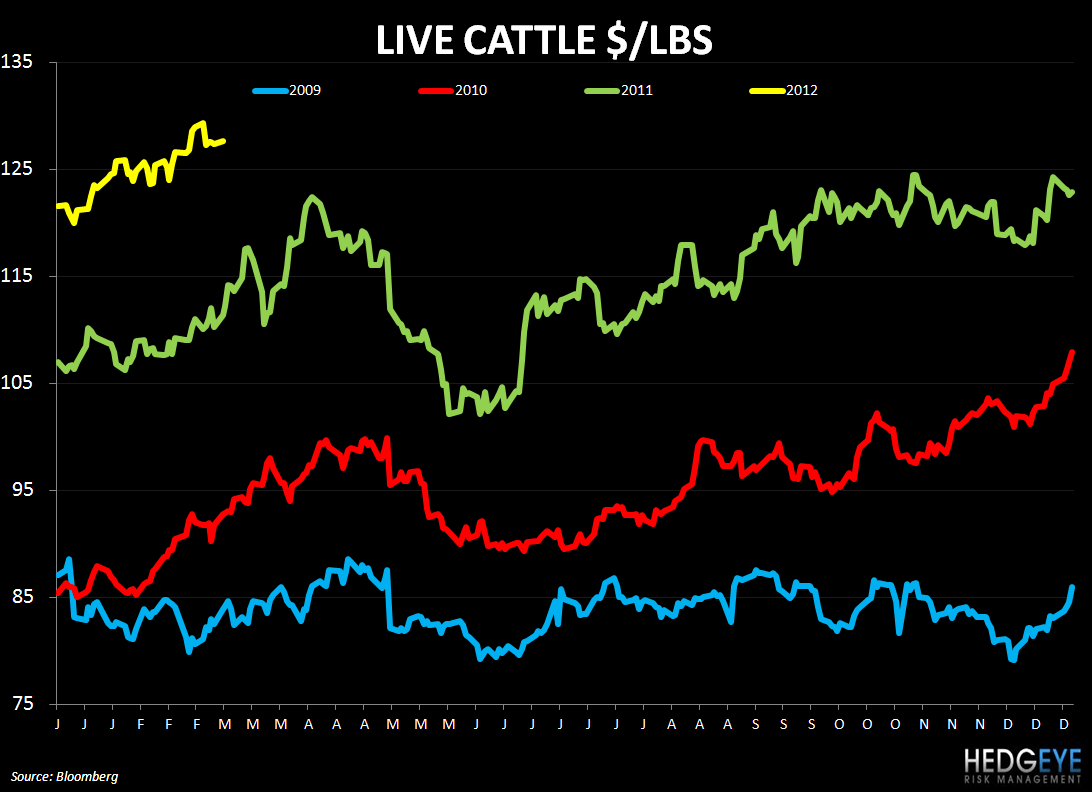

Beef: Global demand for beef remained strong in the first two months of the year, continuing to track above year-ago levels… Weather is improving prospects for farming in areas of Texas but some areas, like the Panhandle, are still suffering from adverse weather… Experts expect it will take a year for pastures to recover, however… the US cattle slaughter rate has declined below 600k per week in three of the last four weeks as fewer cows enter market… Slowing cattle placements in January slowed, confirming a continuing tightening of beef supplies

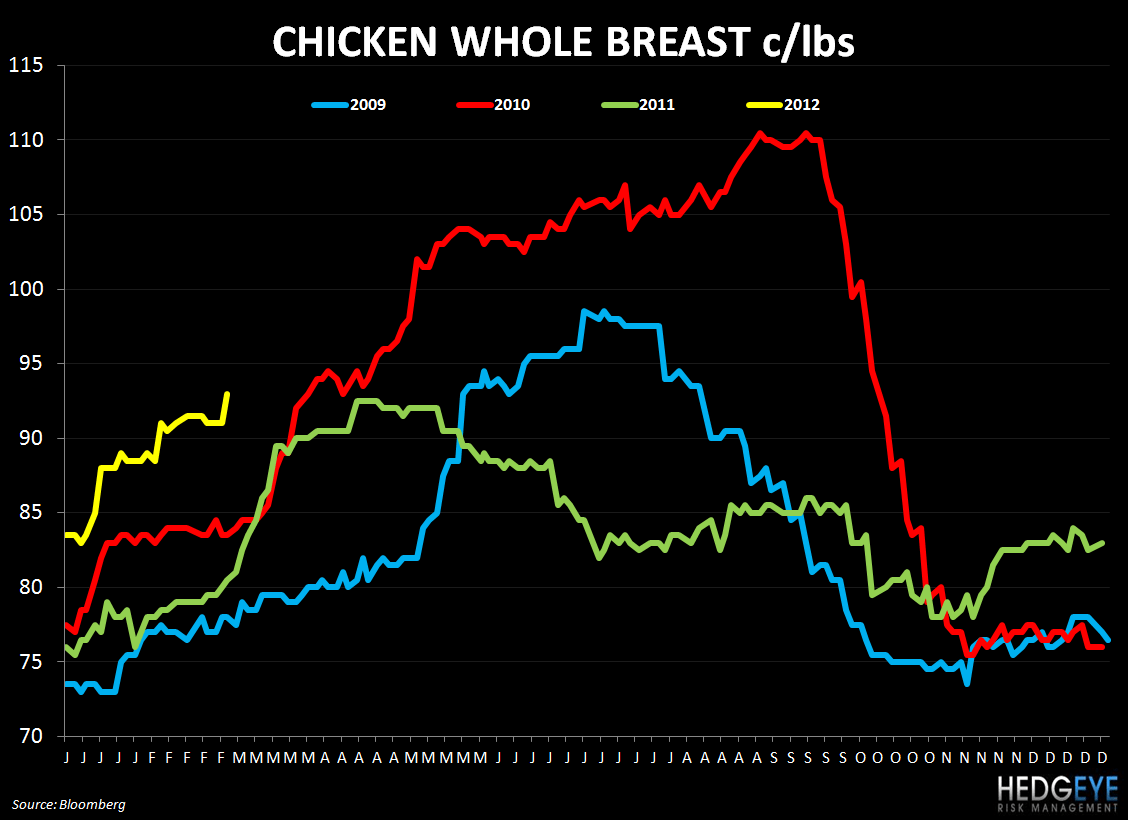

Chicken: Egg sets placements continue to contract at around the same rate, according to the Broiler Hatchery report released by the USDA today.

RECENT COMPANY COMMENTARY

Beef: Most companies are expecting beef cost inflation to be up mid-to-high single digits versus last year

TXRH: We expect approximately 8% food inflation in 2012, primarily due to higher beef costs…on the beef side we do have fixed price – pricing arrangements in effect for over 90% of our beef costs in 2012.

CBRL: To the continued pressure on ground beef prices and other commodities partly offset by lower average dairy and produce prices, along with benefits from our supply chain initiatives, we expect cost of sales to increase 60 basis points to 80 basis points over 2011 to near 26% in 2012.

RUTH: We project 2012 beef inflation to be between 5% and 8%. We currently have purchase agreements for beef representing approximately 30% of our needs through August of 2012, which represents an approximate 7% premium compared to the prior years.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans. Beef costs will be especially challenging due to protracted supply shortages, despite recent reductions in grain prices.

MCD: As we look at our guidance for 2012, we've built another mid-teens increase for beef, expecting that the dynamics in the marketplaces that we see, and are expecting, will continue.

DRI: U.S. beef production will continue decline though over the next 24 months, placing continued upward pressure on beef prices because of the slow economic recovery hamburger and value oriented beef, cattle beef are in high demand and can be priced accordingly by the packers. At Darden we purchased mainly tenderloins and other premium steakcuts, while we expect pricing for our beef products to increase by 12% our pricing has been tempered by consumers' resistance to record higher retail prices for premium stakes and the resulting shift to value oriented cuts and as you can see beef is approximately 14% of our cost basket … We have 75% of our beef requirements contracted for fiscal 2012 and 40% of the June to December usage under contract for fiscal 2013.

SONC: One item to note is that we recently locked in our beef contract for calendar year 2012… given the potential for beef costs going even higher, which there are a lot of reports out there that speculate that could happen, that we chose to go with making this more of a known quantity here, and the idea of having a set price for the next 12 months, we feel like would be good for our business, adds some predictability to the business.

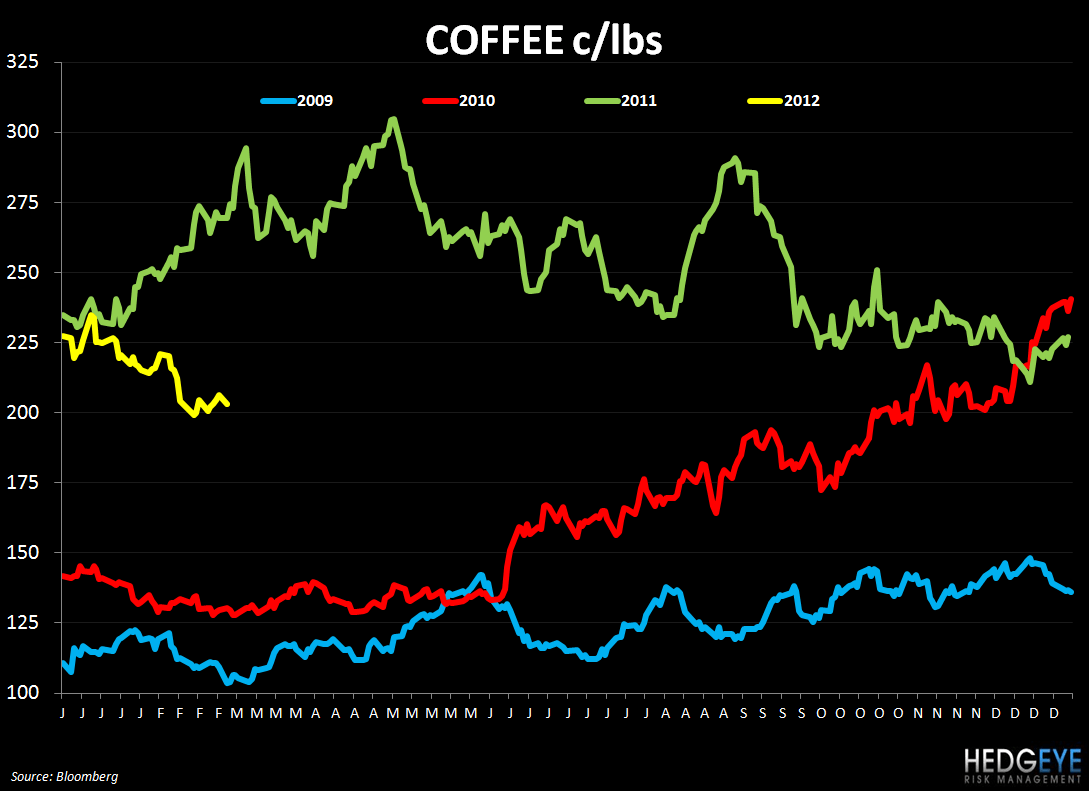

Coffee: Prices are now down -24% versus last year

PEET: We expect 2012 coffee costs to rise 12% instead of last year's 42%.

SBUX: We've taken advantage of the recent declines in the C-price to lock in more of our coffee needs for fiscal 2013. We now have six months of our fiscal 2013 requirements secured at costs moderately favorable to 2012.

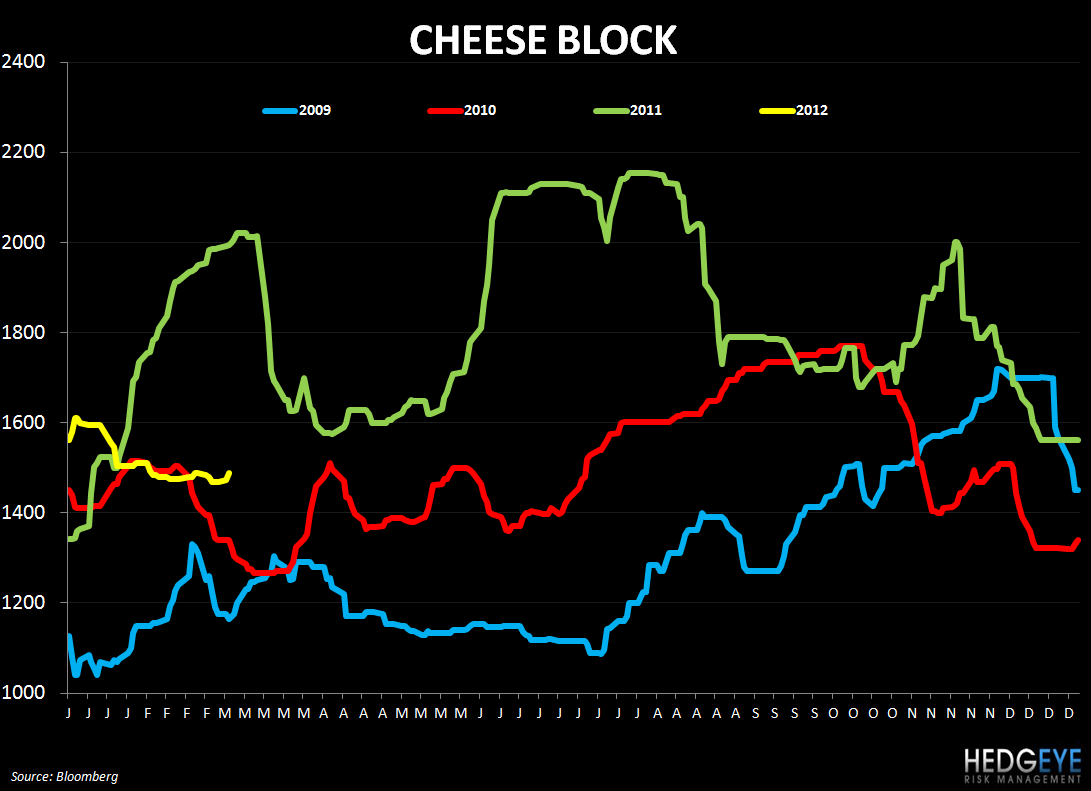

Dairy: CAKE, DPZ, PZZA, TXRH and others could benefit from favorable cheese costs this year

TXRH: The volatility around that 8% estimate for food cost inflation would really be driven by produce and dairy. Those are of the biggest components that we float around the market, and that's about 15% to 20% of our total cost of sales.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

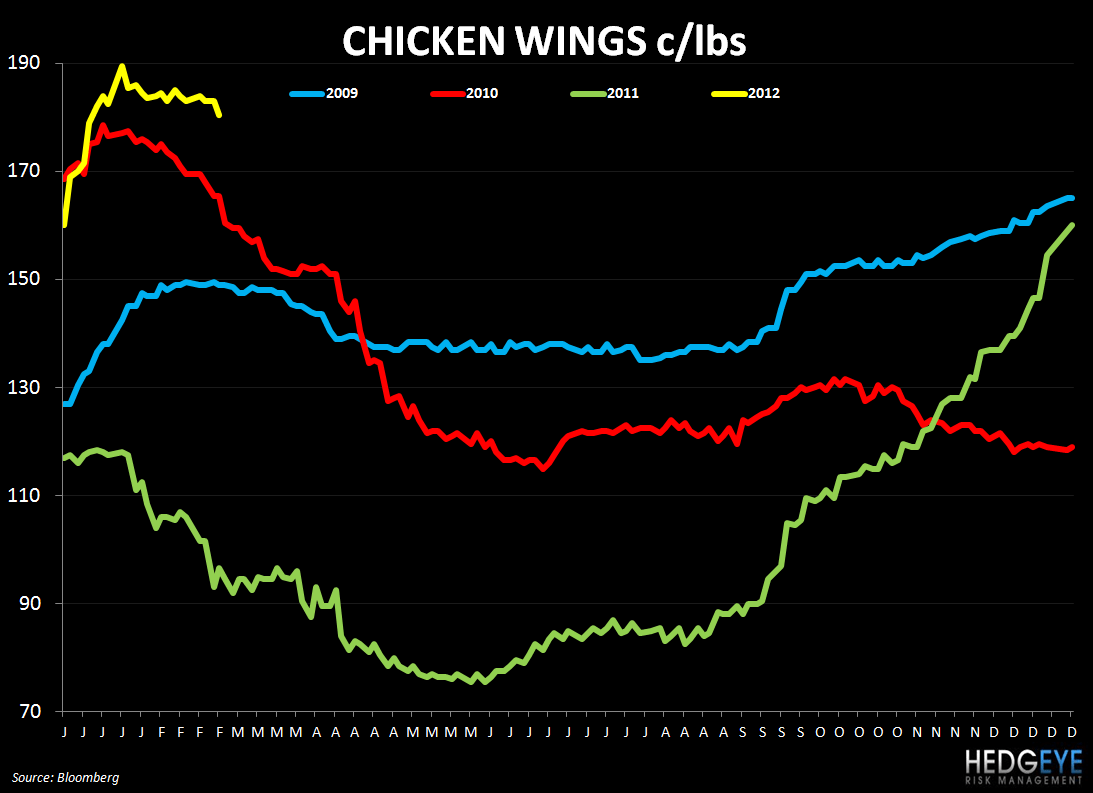

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst