TODAY’S S&P 500 SET-UP – February 29, 2012

As we look at today’s set up for the S&P 500, the range is 15 points or -0.81% downside to 1361 and 0.28% upside to 1376.

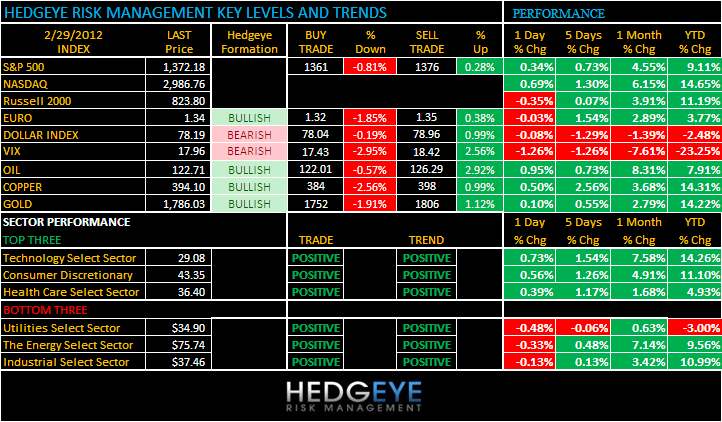

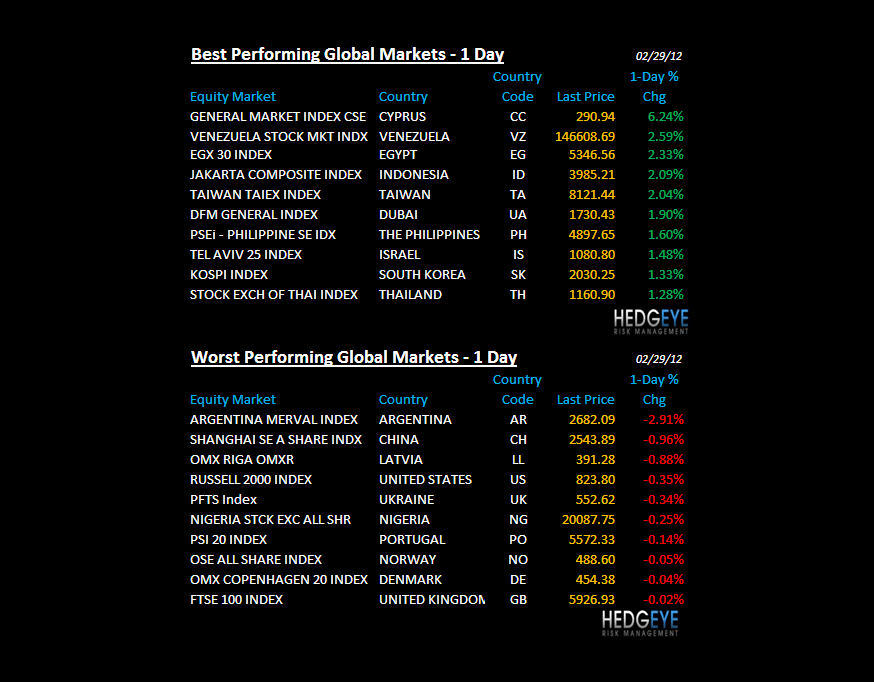

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 36 (62)

- VOLUME: NYSE 754.69 (3.04%)

- VIX: 17.96 -1.26% YTD PERFORMANCE: -23.25%

- SPX PUT/CALL RATIO: 1.33 from 2.36 (-43.64%)

CREDIT/ECONOMIC MARKET LOOK:

MONTH-END – with an oversupply in the asset management industry we continue to see the last 6 days of the month, trade significantly higher than the 1st 6 days of the new month – this was the case on the way down (May-Sep 2011) inasmuch as it is on the way up. The SP500 has been up for 4 consecutive days, so they may as well make it 5 into month-end and get it over with. AAPL is only up +17.5% for the month. Probably doesn’t impact the indices, right?

US DOLLAR – the next move here will be as critical as the down move has been since Bernanke signaled his Policy To Inflate on January 25th. Don’t forget that the USD is down -4.3% from its YTD high (that’s a lot) and that has had a huge impact on inflation expectations (TIP, GLD, OIL, etc). As we push past the LTRO (530B this morn) and into the March sovereign debt maturity spike in Japan (53T Yen), the USD should start trading on fresh factoring.

- TED SPREAD: 39.09

- 3-MONTH T-BILL YIELD: 0.10%

- 10-Year: 1.93 from 1.94

- YIELD CURVE: 1.65 from 1.65

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Apps, week of Feb. 24, (prior -4.5%)

- 8:30am: 4Q GDP (second revision), est. 2.8% (prior 2.8%)

- 8:30am: Personal Consumption (second revision), est. 2.0% (prior 2.0%)

- 9:30am: Fed’s Fisher speaks on U.S. economy in Mexico City

- 9:45am: Chicago Purchasing Managers, Feb., est. 61.0 from 60.2

- 10:00am: NAPM-Milwaukee, Feb., est. 58.8 (prior 58.4)

- 10:00am: Fed’s Bernanke delivers semi-annual monetary policy report in Washington

- 10:30am: DOE inventories

- 1:00pm: Fed’s Plosser speaks on economy in New York

- 2:00pm: Beige Book

GOVERNMENT:

- President Obama hosts dinner for armed forces personnel in Operation Iraqi Freedom and Operation New Dawn

- 8am: Transportation Secretary LaHood speaks at high speed rail summit in D.C.

- House, Senate in session:

- 10am: House Transportation panel hearing on cruise ship safety and lessons from the Costa Concordia accident

- 10am: House Agriculture holds hearing on CFTC agenda

- 10am: House Ways and Means hearing on Obama trade policy

WHAT TO WATCH:

- Fed Chairman Bernanke gives testimony on monetary policy, U.S. economy; watch comments on labor mkt, any indication of QE3, 10am

- Romney wins Michigan narrowly, triumphs easily in Arizona; Republican primary now moves to 12 states in March

- ECB lends banks EU529.5b for 3 yrs; est. EU470b. Total number of bidders: 800

- Apple says giving Proview iPad brand would hurt consumers

- Apple is poised to break $500b market cap; will hold March 7 event to unveil new iPad

- Rule that may require all cars, light trucks sold in the U.S. to have rear-view cameras won’t be issued until the end of the year: U.S. regulators

- Goldman Sachs, Wells Fargo, JPMorgan Chase are among banks that may face civil claims tied to sales of mortgage-backed securities.

- NY Comptroller Thomas P. DiNapoli to discuss Wall Street bonus figures at 8:30am on MSNBC

- Beige book released at 2pm; watch for comments on labor market

- India GDP grows the least since 2009, adding rate-cut pressure

- Japan, S. Korea report larger-than-forecast industrial production

- Standard Chartered profit climbs to record for eighth year

EARNINGS:

- Joy Global (JOY) 6:00am, $1.36

- Staples (SPLS) 6:00am, $0.41

- Carter’s (CRI) 6:30am, $0.44

- Starwood Property Trust (STWD) 6:30am, $0.44

- ITT (ITT) 7:00am, $0.35

- Hospitality Properties Trust (HPT) 7:01am, $0.79

- Liz Claiborne (LIZ) 7:27am, $0.14

- Accretive Health (AH) 7:30am, $0.16

- CenterPoint Energy (CNP) 8:02am, $0.19

- Fannie Mae (FNMA) 8:30am, NA

- Sotheby’s (BID) 4:00pm, $1.25

- Edison International (EIX) 4:00pm, $0.46

- Finisar (FNSR) 4:00pm, $0.23

- MBIA (MBI) 4:00pm

- PetSmart (PETM) 4:02pm, $0.90

- Babcock & Wilcox (BWC) 4:05pm, $0.41

- McDermott International (MDR) 4:06pm, $0.19

- Greif (GEF) 4:07pm, $0.58

- Darling International (DAR) 4:30pm, $0.33

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – 2 down days does not even a hyper short-term TRADE make. Both Brent and WTI have corrected to their most immediate-term TRADE lines of support ($122.01 and $105.46, respectively) and bounced. Bernanke’s semi-annual USD Debauchery speech is today, so that should be interesting to watch in real time vs TIP, GLD, OIL, etc. Inflation from here is not growth. Déjà vu Q1 2011.

- Jewelers Want Platinum for Asians After Gold Vaults: Commodities

- Americans Pay More as Sanctions Lift Iran Profit: Energy Markets

- Oil Set for Best Month Since October on Recovery Signs, Iran

- Soybeans Set for Best Monthly Gain in a Year on Parched Crops

- Iran to Take Gold Payments From Trade Partners, Agency Says

- Natural Gas Near Bottom, Avoid Short Bets, Morgan Stanley Says

- Gold May Gain for a Second Day on ECB Lending; Platinum Climbs

- Aluminum Fee to Japan Gains for First Time in Three Quarters

- Asia Faces Sugar Deficit as Demand Increases, McNeill Says

- Corn Shipments From India to Miss Forecast on Pests, Rupee

- Oil Surge to Record Endangers Europe’s Growth Dash: Euro Credit

- Lumber May Extend Rally as China, U.S. Demand Gain, Ekstrom Says

- Robusta Coffee Rises as Traders Bet on Higher Price; Sugar Falls

- Oil Surge Endangers Europe’s Growth Dash

- Copper Rises, Heads for Back-to-Back Monthly Gains on Stockpiles

- Iraq Plans to Cut Daily Kirkuk Crude Oil Exports by 5% in March

- Palm Oil Has Best Monthly Gain Since 2010 as Supplies Decline

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team