The short interest is showing a lot of pain for the bears in QSR. In casual dining, the shorts are piling into Brinker.

The top quality QSR names continue to win people over; SBUX and MCD saw a reduction in short interest as a percentage of float for the two weeks ended 2/15 despite short interest in the two stocks declining to 0.9% and 0.7%, respectively.

The most recent data, released last night and reflecting the short interest level as of the settlement date 2/15, shows that the QSR space remains intimidating for the bears. This is not surprising given the hiring trends in QSR and the resilience of many QSR businesses through dire economic conditions. Casual dining is typically far more vulnerable in such downturns and, given the concern around increasing gas prices and the hyper-competitive discounting environment in the industry, it is understandable that the shorts might focus their attention on that category before turning to QSR.

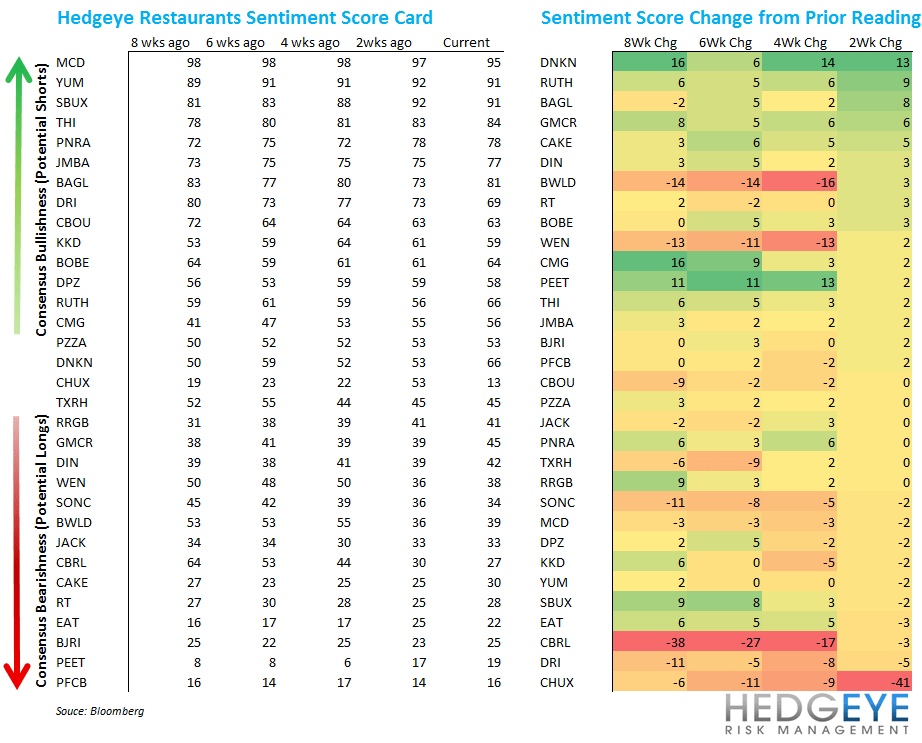

Below is our sentiment scorecard. MCD, YUM and SBUX continue to reign supreme and EAT and PFCB continue to struggle to attract any love whatsoever from the investment community. We have been positive on EAT for 18 months and have been positive on PFCB for just over one month.

SENTIMENT SCORECARD

SHORT INTEREST

QSR CALL OUTS

- CBOU and THI saw upticks in short interest over the most recent two weeks of data. CBOU reported a strong 4Q but it seems investors in the stock were ahead of it and sold on the news. THI is up 9% month-to-date, most of that coming on the back of strong earnings on the 23rd. The fact that coffee costs are coming down is bullish for this space

- MCD and SBUX are so high on the sentiment scorecard; short interest is so low, that any miss versus expectations could lead to sizeable decreases in their respective stock prices. As yet, we are not seeing any deterioration in the fundamental outlook for those companies

CASUAL DINING CALL OUTS

- CBRL short interest is rising as gas prices go higher

- EAT short interest gained during the first half of the year but the stock has bounced back strongly over the last three days; we think some shorts are covering here. EAT has had a great run, and investors are likely to wait for further evidence from the management team that the turnaround is continuing before pushing the stock substantially higher. We continue to like the name, especially relative to competitors like DIN and RT, but have other longs higher on our list (JACK, PFCB & YUM)

- PFCB is squeezing the shorts and, with short interest as a percentage of float at just under 20%, there is plenty of room for more bears to capitulate if the fundamental outlook continues to improve on the margin.

- CAKE guided down 1Q12 EPS and that hurt the stock.

- BWLD ran over the shorts and caused a reversal of the prior trend of increasing bearishness in the name.

Howard Penney

Managing Director

Rory Green

Analyst