Conclusion: We expect a good Q4 out of FL Thursday. With heightened anticipation over Hicks’ new long-term strategic plan to be unveiled at next week’s analyst day we don’t expect near-term momentum to slow just yet. That’s a consensus call, but we think the consensus is right.

TRADE (3-Weeks or Less):

We’re at $0.55 for FL on a comp assumption of +8% for the quarter headed into Thursday’s print, which is ahead of the Street at $0.51 and +6.5% respectively. The latest NPD data which is a component of our (statistically-valid) comp predictive model, supports our above consensus view.

- Sales held in at a MSD rate in January to end the quarter up +7% in the Athletic Specialty channel outpacing the total industry. As a result we have increased our comp expectations by 1pt to +8%.

- In light of sales coming in stronger at quarter end, we have increased our GM estimates to 100bps over last year driven by +80bps in occupancy leverage and +20bps from merchandise margin.

- The modest upside in merchandise margin reflects a sequential deceleration in light of the change in promotional cadence and store events that were lapped in Q4.

- We expect SG&A to come in up +6.5% yy in Q4 reflecting +8% core growth spending offset in part by $4-$5mm in Fx benefit.

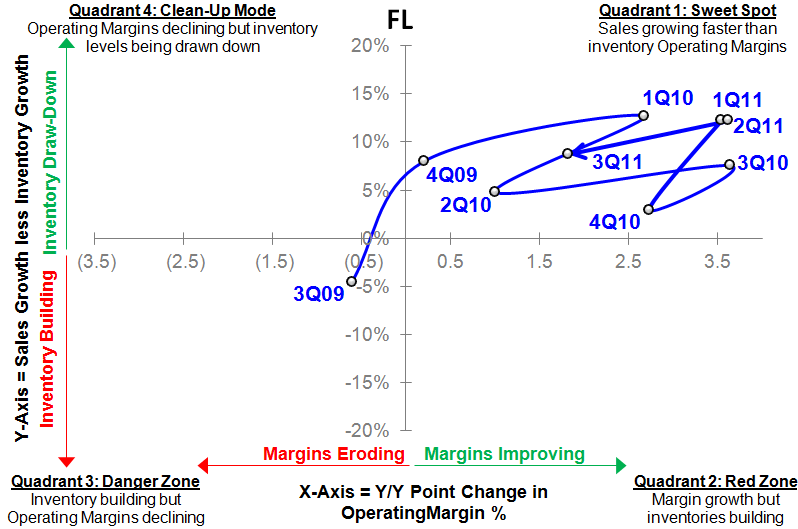

TREND (3-Months or More):

We’ve had 10% comps over the past year, 40% EBIT growth, and seven consecutive quarters of improvement in the sales/inventory spread. It’s worth noting that over this precise seven quarter period, FL has beaten every quarter by a weighted average of 32%.

Growth will slow on the margin as FL faces increasingly tougher comps in the 1H in addition to slower growth out of Europe limiting significant upside surprises to earnings over the intermediate-term.

TAIL (3-Years or Less):

Hicks delivered on his 5-year plan 3-years ahead of schedule. The company is hosting an analyst meeting next week on March 6thto outline its new strategic plan. We expect the focus to remain on the next leg of improving apparel assortment and mix, growing the international store footprint (more productive than domestic base), and expanding its digital platform one part of FL’s business that we think is truly underappreciated.

We expect the company to earn $2.35 in F13 and generate mid-teens earnings growth over the next 2-3 years. That gets you a low-to-mid $30s stock. If Hicks throws out goals of 10% EBIT margins as expected and sales/avg. sq. ft. of $450+ and $6.5Bn in sales, investors will start looking at $2.75 in earnings power, and a $40 stock. We’ll see what’s unveiled next week.

Casey Flavin

Director