TODAY’S S&P 500 SET-UP – February 27, 2012

As we look at today’s set up for the S&P 500, the range is 13 points or -0.64% downside to 1357 and 0.31% upside to 1370.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 272 (-1042)

- VOLUME: NYSE 640.97 (-16.00%)

- VIX: 17.31 3.04% YTD PERFORMANCE: -26.03%

- SPX PUT/CALL RATIO: 2.26 from 2.12 (6.60%)

CREDIT/ECONOMIC MARKET LOOK:

10YR – its been a while since the 10-yr bond yield was more wrong than the US stock market on growth expectations. At every turn in the last year, bond yields have told you all you need to know about US Growth Slowing. After failing at the 2.03% TREND line last week, snapping the 1.97% TRADE line puts 1.91% back in play.

- TED SPREAD: 39.40

- 3-MONTH T-BILL YIELD: 0.09%

- 10-Year: 1.94 from 1.98

- YIELD CURVE: 1.65 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Pending Home Sales, Jan., est. 1.0% (prior -3.5%)

- 10:30am: Dallas Fed, est. 15.5 (prior 15.3)

- 11:30am: U.S. selling $33b 3-month bills, $31b 6-month bills

GOVERNMENT:

- Obama hosts dinner for National Governors Association

- House, Senate in session:

- House Judiciary panel meets on “Regulatory Freeze for Jobs Act of 2012,” which provides that no agency may take any significant regulatory action until unemployment rate is hits, or falls below 6.0%, 4pm

WHAT TO WATCH:

- BP, plaintiffs suing over 2010 Gulf of Mexico oil spill said to be discussing $14b accord; liability trial originally scheduled to start today postponed for week

- Elpida sought bankruptcy protection in Japan’s largest filing in two yrs; watch suppliers, Micron Technology

- Nokia introduced lower-priced Windows phone at Mobile World Congress

- Berkshire’s Warren Buffett says he’s “on the prowl” for large acquisitions

- G-20 nations rebuffed German-led calls to come to Europe’s rescue as it battles the sovereign debt crisis

- Vulcan Materials, Martin Marietta face off in Delaware Chancery Court tomorrow in trial over $4.7b takeover

- HSBC said it’s on “clear trajectory” to meeting its profitability target next year

- Russian, Ukrainian security services foiled plan to assassinate Vladimir Putin, Russia’s Channel One said

- Sprint Nextel said to have abandoned plans to buy MetroPCS Communications

EARNINGS:

- AES (AES) 6 a.m., $0.22

- Lowe’s (LOW) 6 a.m., $0.23

- Quicksilver Resources (KWK) 6:44 a.m., $0.00

- Visteon (VC) 7 a.m., $0.79

- Dendreon (DNDN) 7 a.m., $(0.60)

- El Paso (EP) 7:30 a.m., $0.30

- El Paso Pipeline Partners (EPB) 7:30 a.m., $0.63

- Charter Communications (CHTR) 8 a.m., $(0.19)

- Valeant Pharmaceuticals (VRX CN) 8 a.m., $0.84

- Southwestern Energy (SWN) 4 p.m., $0.47

- Priceline.com (PCLN) 4:01 p.m., $5.06

- Human Genome Sciences (HGSI) 4:01 p.m., $(0.41)

- URS (URS) 4:05 p.m., $0.98

- Western Gas Partners (WES) 4:05 p.m., $0.43

- Sina (SINA) 4:30 p.m., $0.21

- Universal Health Services (UHS) 5 p.m., $0.90

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Bullish Futures Exceed 1 Million First Time in 2012: Commodities

- Iran Drives Hedge Fund Oil Bets to 10-Month High: Energy Markets

- Oil Snaps Longest Rally in Two Years as IMF Warns on Economy

- Commodity Investments May Climb as Much as $40 Billion in 2012

- Copper Falls on Demand Concern as Europe’s Debt Crisis Persists

- Gold Declines in London as Prices Near 3-Month High Curb Demand

- BP Preparing New Plan With Reliance for India’s Biggest Gas Area

- 8S.Korea Offers to Cut Iran Oil Imports by 15%-20%: Yonhap

- Corn Falls on Speculation U.S. Growers to Boost Output to Record

- South Korea Delays Bill Challenging Top-Emitter Ranking: Energy

- U.K. Gas Rises on LNG Concern; Power Rises After Biomass Blaze

- India Road-Building Hits Record as Builders Pay to Work: Freight

- European Union Says Cereal Production May Reach Three-Year High

- Iran Drives Fund Oil Bets to 10-Month High

- Robusta Coffee Falls as Vietnam’s Exports May Rise; Sugar Climbs

- Fuel-Oil Discount Widens; Gasoil, Naphtha Rise: Oil Products

- BP Said to Weigh $14 Billion Gulf of Mexico Oil Spill Accord

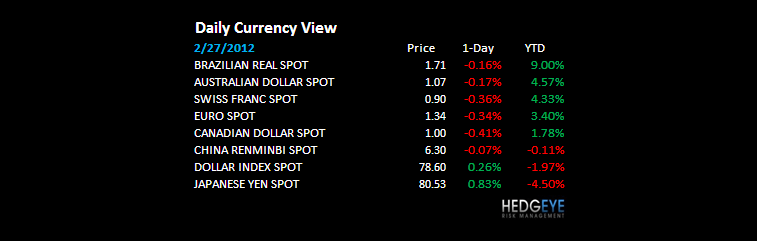

CURRENCIES

EUROPEAN MARKETS

FRANCE – another +0.6% sequential ramp in producer prices this month is only going to perpetuate the stagflation we see in France, Spain and Italy. Who cares about Greece when these 3 majors will have a much larger say in global growth expectations. The CAC’s TAIL remains broken and now the immediate-term TRADE line is under fire (3439). We re-shorted France (EWQ) late last week.

ASIAN MARKETS

INDIA – obviously a country that is short oil is a country that is going to have a stagflation problem with oil prices ripping like this. That wasn’t new to the Indians last week, but evidently it mattered to their stock market today – at down -2.8% in a straight line, that’s the problem with bearish market SKEW. India’s Yield Curve has gone to flat.

MIDDLE EAST

The Hedgeye Macro Team