This week’s earnings provide the latest look at the state of mid-tier department store retail, which is playing out as we outlined back in Q3. The bottom-line here is that inventory growth continues to outpace sales, which is fueling a highly competitive pricing environment in the mid-tier (i.e. more promotional) further widening the bifurcation between the low-end and high-end retailers. Good for JWN, SKS, as well as discount and dollar store players TJX, ROST, DLTR; Bad for KSS, JCP, SHLD, M, HBI & GPS.

Here are a few considerations for this week’s key themes:

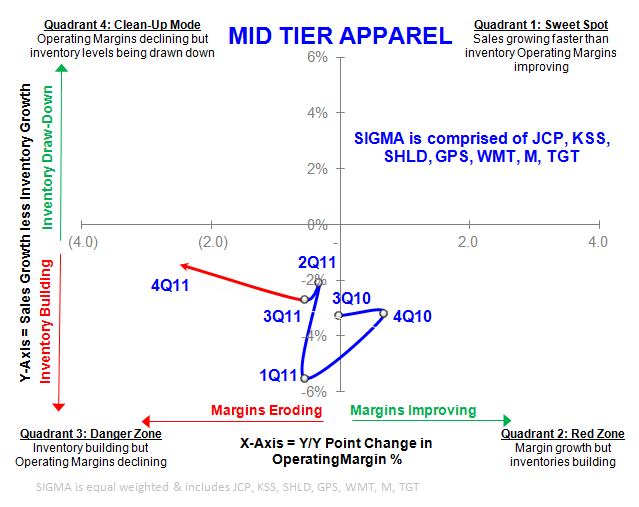

1) Inventory Growth: The trend of inventory growth outpacing sales continues to plague the mid-tier department stores as reflected in the chart below. Also worth noting are the three companies in this set that posted positive sales/inventory spreads: SHLD, JCP, and DDS. While a positive spread is a just that – positive on the margin, not all positive spreads are created equal, composition matters. In this regard, both SHLD and JCP achieved positive spreads by stripping inventories out faster than sales declined. This is considerably different in quality from TJX and DLTR which posted +11% and +13% sales growth respectively with inventories growing, but just at a slower rate.

Re WMT International… “Inventory management remains an area needing improvement” – Doug McMillon, CEO WMT Int’l

“High inventory levels led to increased markdowns and clearance, and unseasonably warm weather impacted several categories” – Lou D’Ambrosio, CEO SHLD

“I would expect inventory to be up at the end of the first quarter somewhere around 4% or so.” - Kevin Mansell, CEO KSS (compared to Q1 sales outlook for +3%)

2) Promotional Environment: The aforementioned factor is what continues to fuel the promotional fire currently ablaze in the mid-tier channel. With gas prices surging higher and discretionary wallets getting tighter, unloading excess inventory will weigh on margins through at least the 1H effecting not only those directly operating in the mid-tier, but also those selling into it (e.g. HBI).

Re Q4…“a highly promotional competitive environment” – Charles Holley, CFO WMT

“We lost some of our leadership on the price element of our value equation; we didn't have enough consistent excitement in our merchandise content; and our sense is our marketing message did not cut through, especially in a highly promotional fourth quarter.” – Kevin Mansell, CEO KSS

“Our promotional cadence should have been more surgical, and cost actions could have been taken earlier.” – Lou D’Ambrosio, CEO SHLD

“In terms of promotional activity, I think that we're always challenging our teams. Last year was not necessarily our best year on this front” – Glenn Murphy, CEO GPS

“competitive intensity reached an all-time high during the holiday season. Research indicates that across retail, two out of three holiday season purchases in gift giving categories were on some sort of promotion, and these promotional discounts were significant, ranging from 25% in some categories to more than 50% in others.” – Gregg Steinhafel, CEO TGT

3) High/Low End Bifurcation: Consistent with what we’ve seen since the 2H of F11, the high-end continues to outperform its more price sensitive peers. While high-end growth is starting to decelerate on the margin, the mid-tier is declining at a faster rate. We expect this reality to persist over the intermediate-term as discretionary spending remains constricted at the lower end. The other fact to consider here is that due to the excess inventory in the mid-tier channel, discounters like TJX, ROST and even dollar stores DLTR, etc. will continue to benefit from better product flow providing a traffic tailwind as evidenced by strong top-line results. .

Casey Flavin

Director