Here are three points that we think are important to keep in context when looking at GPS’ 4Q results.

It’s tough to get too excited when a company beats, but still has EPS down 26%. There are three things to consider with GPS…

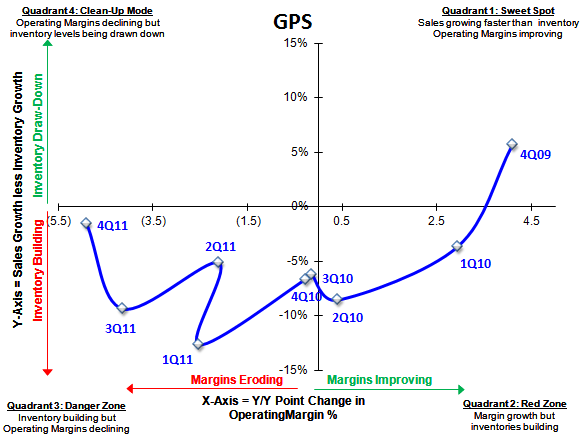

1) The 10% margin guidance target for this year actually might be within a stone’s throw of achievable. It’s so tough to tell with this company given the extreme volatility it sees in its business day to day. But its SIGMA shows a fairly encouraging trend after building inventories throughout the past eight quarters. BUT, the wildcard still remains in JC Penney’s hands. We’re already seeing stepped-up promotional cadence at JCP and KSS. More mid-tier retailers (even Macy’s mid-tier) will follow. To think that this won’t impact GPS is downright wreckless.

2) We get the whole Lampert-esque stock buyback model here. But the reality is that GPS is almost out of gas. Having net cash of $1.5-$2bn and buying $1bn each year is a pretty good place to be. But GPS is flirting with having net debt as opposed to cash. The company announced a new $1bn program yesterday, but we’d be surprised if it executed on it.

3) Longer-term margins: I can give a dozen reasons why any kind of respectable margin GPS printed in the past is no longer a reality. But the best chart I can show is below. It shows GPS’ employee count versus operating margin. This is a human capital business – think sales, marketing, R&D, etc… Good companies invest into their infrastructures in order to (re)gain share. Gap has taken its employee base down by 20,000 employees (13%) over four years. You want a 12% margin again? Find me 20,000 employees. That’ll cost about $1.2bn, or $1.45 per share. Then that’s GPS’ new base to grow from. Perhaps I’m oversimplifying this. But directionally, it’s spot on.

<chart6>