TODAY’S S&P 500 SET-UP – February 24, 2012

As we look at today’s set up for the S&P 500, the range is 15 points or -0.69% downside to 1354 and 0.41% upside to 1369.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1314 (-1906)

- VOLUME: NYSE 763.09 (4.67%)

- VIX: 16.80 -7.64% YTD PERFORMANCE: -28.21%

- SPX PUT/CALL RATIO: 2.12 from 2.15 (-1.40%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 40.42

- 3-MONTH T-BILL YIELD: 0.09%

- 10-Year: 2.00 from 2.00

- YIELD CURVE: 1.70 from 1.70

MACRO DATA POINTS (Bloomberg Estimates):

- 9:55am: UMichigan Consumer, Feb (F), est. 73 (prior 72.5)

- 10:00am: New Home Sales, Jan., est. 315k, up 2.6% (prior 307k)

- 10:45am: Fed’s Williams speaks in New York

- 11:35am: Fed’s Bullard speaks on housing, monetary policy in New York

- 1pm: Baker Hughes rig count

- 1:30pm: Fed’s Plosser, Dudley speak on monetary policy in New York

GOVERNMENT:

- President Obama meets with Danish PM Helle Thorning-Schmidt to discuss European debt crisis in Chicago

- U.S. Dept of Agriculture discusses crop outlook

- Mitt Romney addresses Detroit Economic Club, 11:30am

- House, Senate meet in pro forma sessions

- NRC advisory panel meets to consider NextEra Energy Inc.’s Turkey Point extended power application, 8:30am

- FCC meets on provisions of National Broadband plan, 9am

WHAT TO WATCH:

- Apollo Global, others said to be near deal to acquire El Paso’s oil-exploration business for about $7b

- Purchases of new homes in U.S. probably rose 2.6% in January to a nine-month high, economists est.

- Bank of America is stopping sale of new home loans to Fannie Mae

- Wynn Resorts’s Macau unit ejected Kazuo Okada from its board; Phillipine President Aquino orders probe

- Lloyds posted full-year net loss that missed est.; Volkswagen reported record profit

- U.K. GDP shrank 0.2% in 4Q, in line with forecast

- Apple said to buy search startup Chomp for $50m

- Watch Watson Pharma; last business day before Feb. 26 PDUFA decision date on Prochieve for prevention of preterm labor

- G-20 finance ministers, central bank presidents to meet in Mexico City this weekend

- Warren Buffett to release annual letter to Berkshire Hathaway shareholders tomorrow

EARNINGS

- Enerplus (ERF CN) 6 a.m., C$0.23

- Alpha Natural Resources (ANR) 7 a.m., $0.26

- Endo Pharmaceuticals Holdings (ENDP) 7 a.m., $1.32

- Interpublic Group (IPG) 7 a.m., $0.39

- Pepco Holdings (POM) 7 a.m., $0.19

- Telephone & Data Systems (TDS) 7 a.m., $0.25

- Warner Chilcott (WCRX) 7 a.m., $0.90

- United States Cellular (USM) 7:04 a.m., $0.24

- Eldorado Gold (ELD CN) 7:30 a.m., $0.20

- EW Scripps (SSP) 7:30 a.m., $0.10

- J.C. Penney (JCP) 7:50 a.m., $0.67

- Pinnacle West Capital (PNW) 8 a.m., $0.04

- Washington Post (WPO), 8:30am, NA

- American Water Works (AWK) 4:30 p.m., $0.33

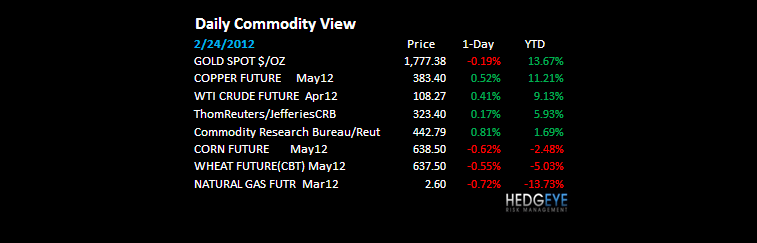

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

We couldn’t make up this #1 Headline on Bloomberg this morning if we tried – “STOCKS, OIL CLIMB ON GLOBAL ECONOMIC RECOVERY”

COPPER – the Doctor just doesn’t agree with this manic media headline at all – neither does the 10yr UST yield – both are failing at critical lines of resistance of $3.85/lb and 2.03%, respectively, this morning. Those who confuse inflation with growth will be doing it for the 3rd time since 2008.

- Copper Traders Most Bullish in Two Months on Demand: Commodities

- U.S. Soybean Output May Rise to 3.25 Billion Bushels, USDA Says

- Oil Rises a Seventh Day in Longest Winning Streak in Two Years

- Gold May Gain in London as Weaker Dollar Spurs Investor Demand

- Corn Declines as U.S. Acreage Expands, Ukraine Sales to Climb

- Oenophile Chinese Purchase Bordeaux for $470 Mainland Bottles

- Copper Heads for First Weekly Gain in Three Before U.S. Data

- Rubber Caps Best Gain in Five Weeks as Oil Rally Boosts Appeal

- Statoil $1.2 Billion Tanzania Find May Hold Oil in New Play

- Billionaires Vie for Railway to $40 Billion Coal Region: Energy

- Glencore Will Notify EU of Xstrata Bid for Merger Review

- Baosteel Spurs Dim Sum Revival on Cost Advantage: China Credit

- Mentor of Central Bankers Fischer Rues Complacency in New Growth

- Billionaires Vie for Australian Coal Rail

- Gold’s Bull Run May Drive Price to $5,000, Wyke Forecasts

- Cotton Exports From India Slows as Crisis Cools Apparel Demand

- U.S. Corn Crop May Reach Record 14.27 Billion Bushels, USDA Says

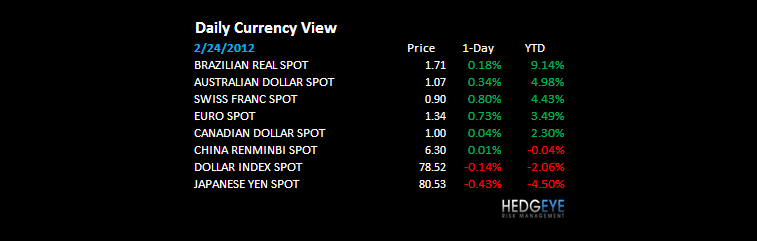

CURRENCIES

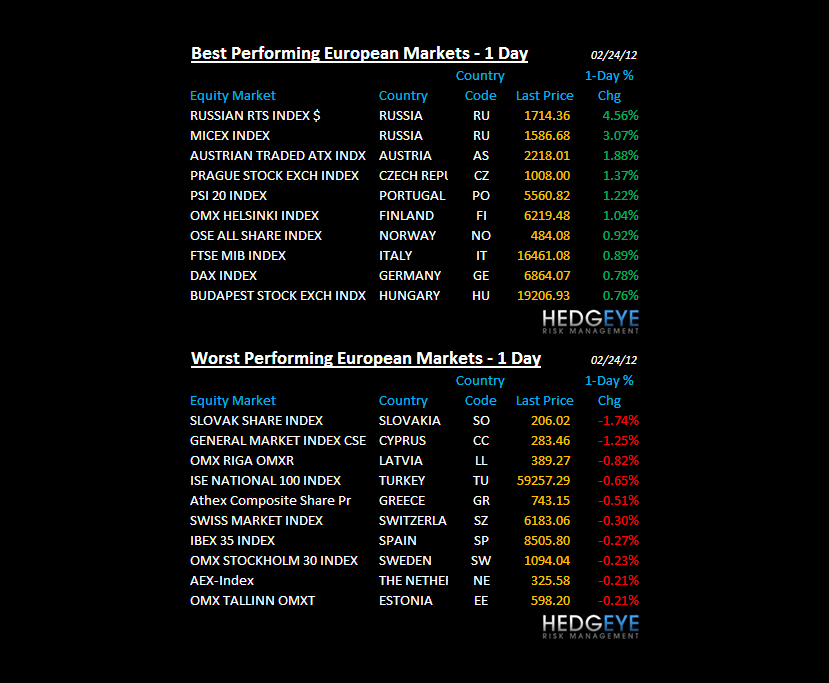

EUROPEAN MARKETS

RUSSIA – which is obviously a PetroDollar Equity market continues to rage higher as inflation expectations do. The RTSI is up another +2.4% this morning and +22% for the YTD as President Obama blames oil rising on “Wall Street Speculators” (dollar down be damned).

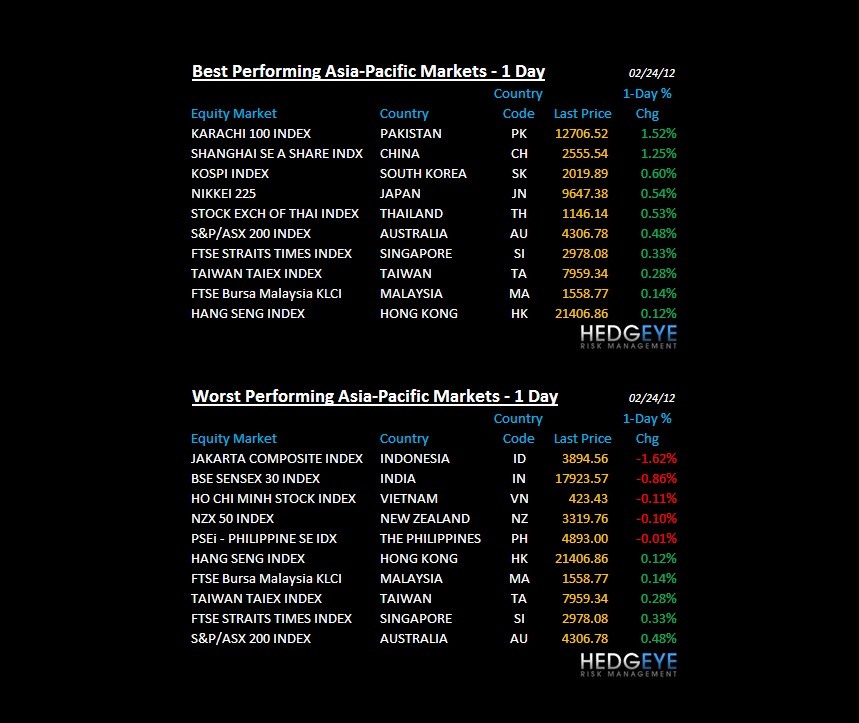

ASIAN MARKETS

YEN – How one of the world’s top 3 currencies can collapse like this and it not be called out by consensus is far beyond my reach. The Yen is down -6% for the month-to-date! It’s not a straight line down, but its close – reminds me of the Euro falling off its highs in April of 2011 and consensus saying “hey, buy European exporters!” – we continue to see this sovereign debt maturity spike (March) in Japan as the why on Yen…

MIDDLE EAST

The Hedgeye Macro Team