After the close, JACK reported a decent quarter on nearly every metric, but the quarter also highlights why the company is not getting the “full” valuations it deserves. Our thesis for owning the stock today is centered on improving operating performance and better valuation stemming from a less volatile business model. We will learn additional details on the conference call at 11am but it is likely that much more will emerge at the analyst meeting next week.

JACK is reporting FY Guidance (9/12) of GAAP EPS of $1.15-1.40 and operating EPS $0.95-1.10. The reality is that the only number that matters is what the core earnings power of the company is. So when the popular financial press is reporting that it is “unclear which range is comparable to FactSet $1.32” we immediately have a problem we don’t need to have. When things are unclear or uncertain, people shy away. By the end of FY12, this issue should be going away – a net positive.

Included in operating earnings this quarter were re-image incentive payments of $5.7 million, or approximately $0.08 per share versus $0.02 last year and $0.06 per share in impairment charges.

Operating EPS Calculation

GAAP: $0.27

Refranchising Gain: ($0.02)

Franchise payments: $0.08

Impairment charge: $0.06

Operating EPS: $0.39

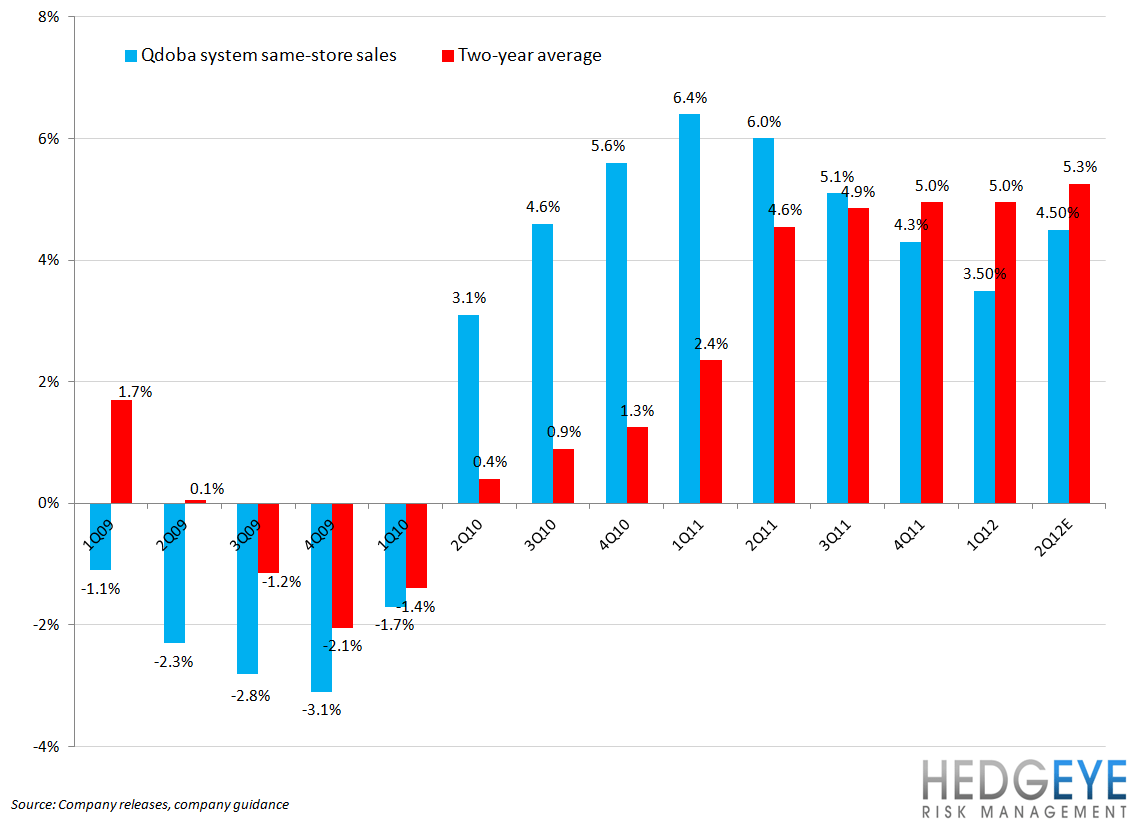

In 1Q12 Jack in the Box company same-store sales were 5.3% versus consensus +4.1% and guidance of +4-5%. Franchise same-store sales were 2.8%, bringing the system same-store sales number to 3.6%. Qdoba system same-store sales were 3.8% versus consensus +2.9% and guidance for +2-3%.

Consolidated restaurant operating margin was 13.5% vs. 12.6% last year with an 8% increase in commodity costs. This represents the second quarter in a row where the company is operating with positive same-store sales and expanding margins – the “Nirvana” quadrant in the chart below. Typically, companies operating in that quadrant are awarded a higher multiple by the Street.

In the press release, management upped its same-store sales guidance for the fiscal year 2012 to +3-4% at Jack in the Box restaurants versus prior guidance of +2-4% and +4-5% at Qdoba system restaurants versus prior guidance of +3-5%. Given that the bulk of the Jack-In-The-Box restaurants are in “non-weather” states, the favorable impact of weather in the first calendar quarter will be much less significant than for others in the space.

From an operating perspective, JACK reported a strong quarter. More details to come at 11 a.m.

Howard Penney

Managing Director

Rory Green

Analyst