Rice and coffee prices were the big outlier to the downside over the past week. This is good news for PFCB and, particularly, the coffee companies like SBUX, PEET, DNKN, THI, GMCR, and CBOU.

The dollar showing weakness over the last week has coincided with strong price gains for most of the agricultural commodities that we follow. Gold, oil and the XLE also posted strong year-over-year gains as the Federal Reserve continues to, as Keith wrote in this morning’s Early Look, “legislate inflation”.

CONSUMER CALLOUT

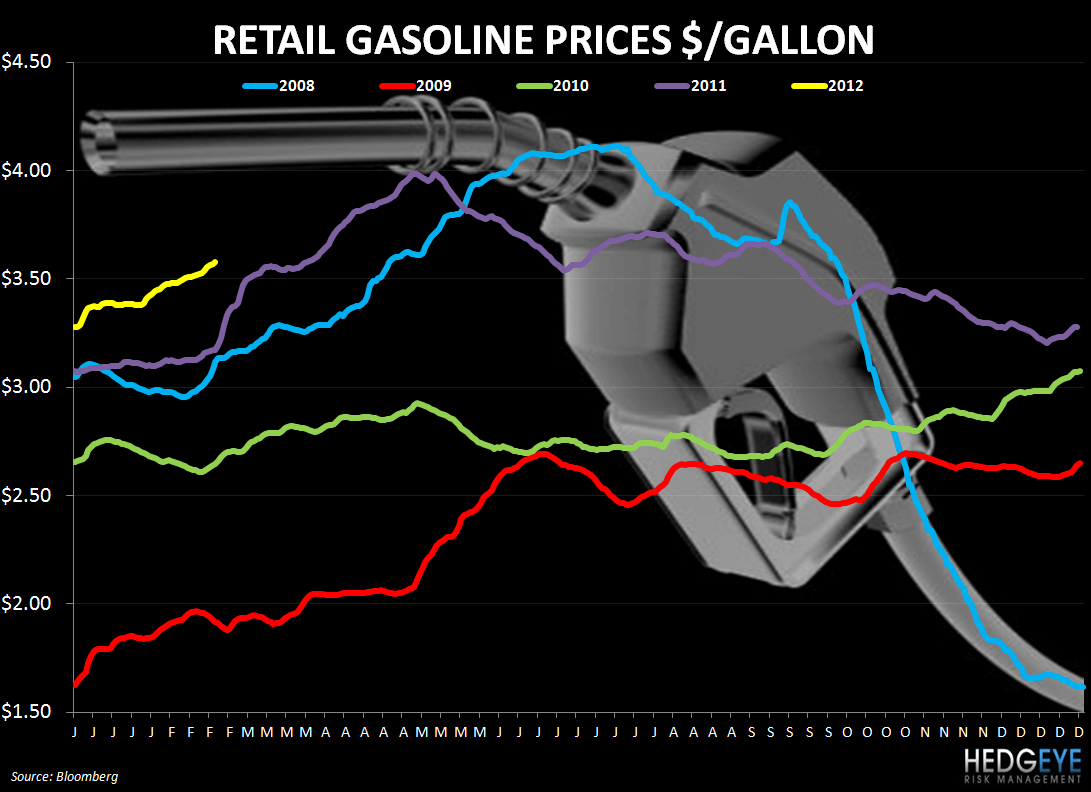

Gasoline Prices are creeping higher around the country with $4.00/gallon gas in California and media reports emerging of some gas stations demanding $6.00/gallon in Florida. At some point, this will negatively impact consumer spending.

RECENT COMPANY COMMENTARY

BEEF

TXRH: We expect approximately 8% food inflation in 2012, primarily due to higher beef costs…on the beef side we do have fixed price – pricing arrangements in effect for over 90% of our beef costs in 2012.

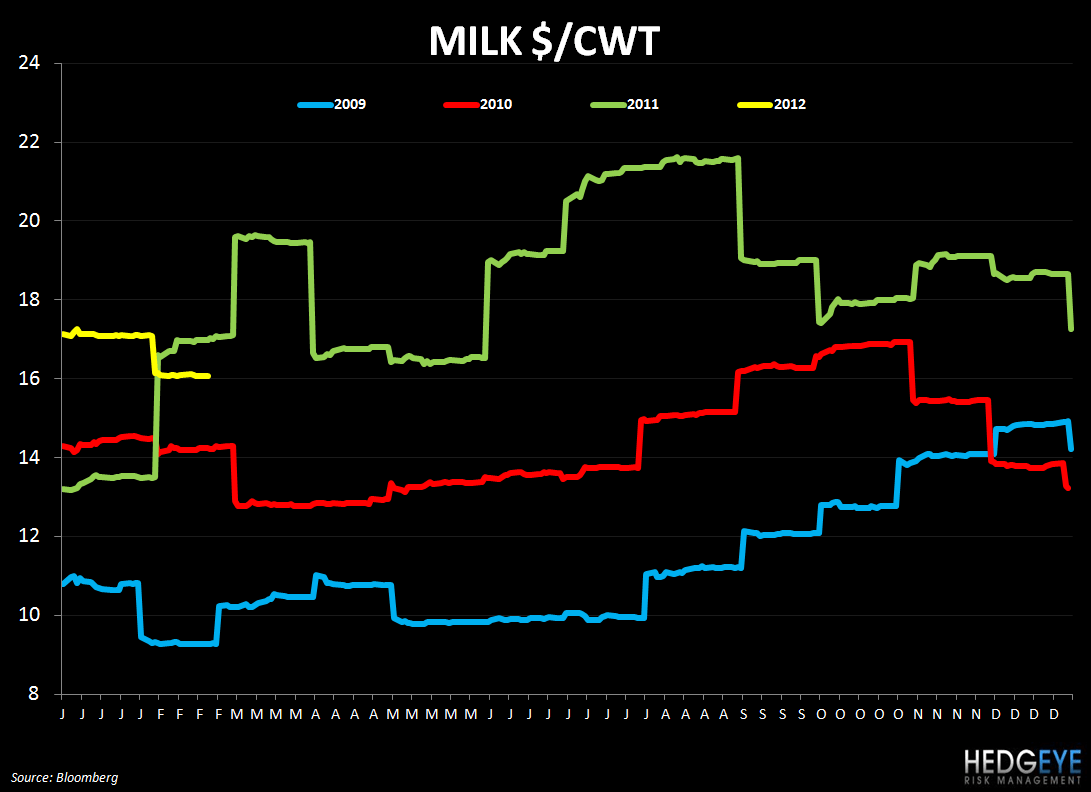

CBRL: To the continued pressure on ground beef prices and other commodities partly offset by lower average dairy and produce prices, along with benefits from our supply chain initiatives, we expect cost of sales to increase 60 basis points to 80 basis points over 2011 to near 26% in 2012.

RUTH: We project 2012 beef inflation to be between 5% and 8%. We currently have purchase agreements for beef representing approximately 30% of our needs through August of 2012, which represents an approximate 7% premium compared to the prior years.

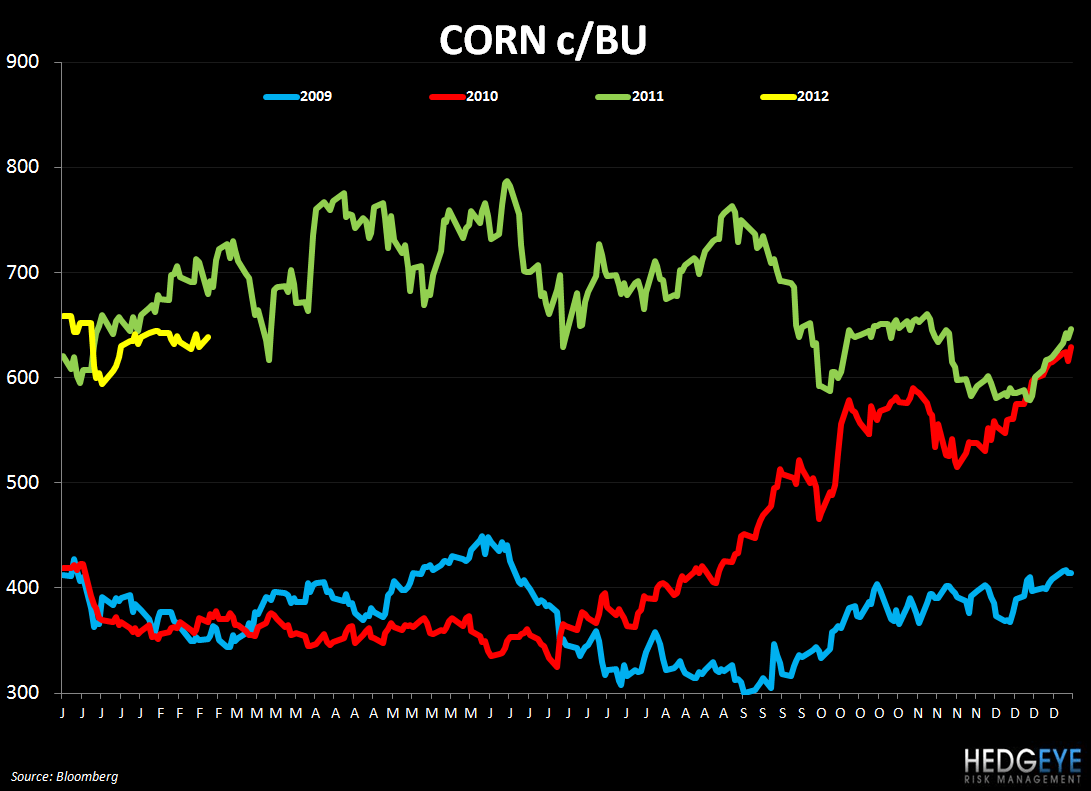

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans. Beef costs will be especially challenging due to protracted supply shortages, despite recent reductions in grain prices.

MCD: As we look at our guidance for 2012, we've built another mid-teens increase for beef, expecting that the dynamics in the marketplaces that we see, and are expecting, will continue.

SONC: One item to note is that we recently locked in our beef contract for calendar year 2012… given the potential for beef costs going even higher, which there are a lot of reports out there that speculate that could happen, that we chose to go with making this more of a known quantity here, and the idea of having a set price for the next 12 months, we feel like would be good for our business, adds some predictability to the business.

COFFEE

PEET: We expect 2012 coffee costs to rise 12% instead of last year's 42%.

SBUX: We've taken advantage of the recent declines in the C-price to lock in more of our coffee needs for fiscal 2013. We now have six months of our fiscal 2013 requirements secured at costs moderately favorable to 2012.

DAIRY

TXRH: The volatility around that 8% estimate for food cost inflation would really be driven by produce and dairy. Those are of the biggest components that we float around the market, and that's about 15% to 20% of our total cost of sales.

CMG: While we're cautiously optimistic we'll see more reasonable prices in 2012 for avocados, dairy and produce, we expect these benefits will be more than offset by higher costs for our beef, chicken, rice and beans.

SUPPLY & DEMAND

Beef – WEN, JACK, CMG, TXRH

Beef prices are a significant input cost for many restaurant companies. The chart of beef prices in the last section of this post shows that prices are now up 17.3% year-over-year, despite the fact that prices have been up year on year for over two years now. TXRH said that it expects 8% food inflation in 2012 primarily due to higher beef costs.

SUPPLY

Texas AgriLife Extension Service personnel, according to CattleNetwork, said that most of Texas received rain in the third week of February, helping to green up pastures and winter wheat.

Total frozen beef supplies were up 7% on January 31st, 2012 versus last year.

An investigation by the federal Canadian Food Inspection Agency has resulted in charges against a Manitoba veterinarian and livestock operators for illegally and intentionally exporting cattle in breach of U.S. and Canadian laws.

Canadian beef supplies have been shrinking since 2005 and are likely to shrink further in the short-term according to statistics released by the Canadian government Monday. The Canadian beef cow herd is down 20% from its peak in ’05 despite shipments to the U.S. being down 24% in 2011 versus the year prior and cow slaughter rates being off 13%. The numbers, according to CattleNetwork, do not add up. The ag website does say, however, that the North American calf crop is down roughly 9% in the past 10 years.

Analysts are expecting U.S. feedlots to have reduced cattle purchases in January as supplies of available animals declined. On Friday, the USDA will release inventory estimates at 3 p.m.

DEMAND

The lead February contract in overnight electronic action hit an all-time high of 129.05 cents, surpassing Tuesday’s 128.97 top and indicating strong demand.

Cattle in the Chinese region of Ningxia Hui were found to have foot-and-mouth disease.

Coffee – SBUX, PEET, DNKN, CBOU, THI, MCD

SUPPLY

Coffee dropped significantly as stockpiles climbed and producers sought to increase sales in Brazil, the world’s top grower.

Coffee inventories monitored by ICE Futures U.S. have jumped 24% since the end of October.

Brazilian permits for exports February to-date surged 26% versus January, according to Cacafe, Brazil’s Council of Coffee Exporters.

DEMAND

Coffee speculators decreased their net-long position in coffee futures in the week ended 2/14.

Chicken Wings - BWLD

SUPPLY

Total frozen poultry supplies on January 31st, 2012 were down 11% year-over-year.

Brazil may boost broiler-chicken production by 3% to a record 13.25 million metric tons in 2012 versus 12.9 million in 2011, according to the USDA. The increase is down from an earlier forecast of 5% growth in production.

The six-week moving average egg sets number declined sequentially from -5.46% for the week ended 2/11 to -5.49% for the week ended 2/18. This is a bullish data point for chicken wing prices; supply is not showing any sign of picking up quickly and beef costs remain at extremely high levels.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst