TODAY’S S&P 500 SET-UP – February 22, 2012

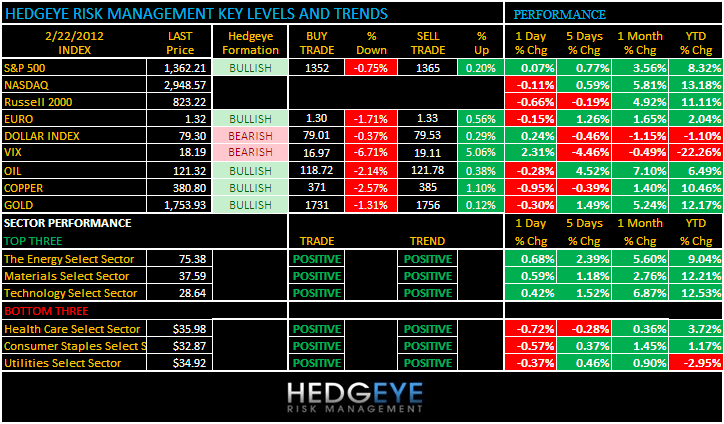

As we look at today’s set up for the S&P 500, the range is 13 points or -0.75% downside to 1352 and 0.20% upside to 1365.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 8 (-424)

- VOLUME: NYSE 797.99 (-11.07%)

- VIX: 18.19 2.31% YTD PERFORMANCE: -22.26%

- SPX PUT/CALL RATIO: 1.42 from 2.31 (-38.53%)

CREDIT/ECONOMIC MARKET LOOK:

GROWTH – pick your overnight economic data point, from German PMI slowing sequentially in FEB to 50.1 vs 51 JAN to Taiwan Exports dropping -8.6% y/y in JAN, we think we’re just getting started here. What happens on the margin m/m matters most. Inflation, from these levels, slows growth.

INFLATION – Italian CPI +3.2% y/y JAN (stagflation), India CPI pops to +7.7% JAN vs 6.6% DEC, and Hong Kong CPI up to 6.1% JAN vs 5.7% DEC –these are all JAN numbers that don’t include this rip in the CRB Index, Oil, etc in FEB.

- TED SPREAD: 42.65

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.05 from 2.06

- YIELD CURVE: 1.75 from 1.76

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage, week of Feb. 17, (prior -1.0%)

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 10am: Revisions: Existing Home Sales

- 10am: Existing Home Sales, Jan., est. 4.66m (prior 4.61m)

- 11:30am: U.S. to sell $40b 4-week bills

- 1pm: U.S. to sell $35b 5-yr notes

- 4:30pm: API inventories

GOVERNMENT/POLITICS:

- Quinnipiac University holds news conference on national poll on 2012 GOP contenders, presidential matchups, 10am

- Republican presidential candidates face off in Mesa, Ariz. in debate sponsored by CNN, 8pm

- House, Senate not in session

WHAT TO WATCH:

- Obama administration said to propose today to cut U.S. corporate tax rate to 28% from 35%

- Sales of previously owned U.S. houses may have climbed 1.1% in Jan. to highest level since May 2010, economists est.

- J&J picked Alex Gorsky to be new CEO

- SAP said to partner with Samsung to push corporate use of Google’s Android

- U.S. Consumer Financial Protection Bureau starting inquiry into bank checking account overdraft policies

- Peugeot says in alliance talks after report of GM discussions

- European services and manufacturing output unexpectedly shrank in February

- France Telecom cut its dividend forecast

- Goldman Sachs cut its 12-month forecast for commodity returns to 12% from 15%

- Shell bids $1.6b for African oil explorer Cove Energy

- Pimco said to be quitting American Securitization Forum over silence on foreclosure settlement

- Solyndra begins piecemeal auction after failing to attract bids for whole company

EARNINGS:

- Donaldson (DCI) 6am, $0.71

- Lamar Advertising (LAMR) 6am, $0.00

- Quanta Services (PWR) 6am, $0.36

- RR Donnelley (RRD) 6:30am, $0.43

- Rogers Communications (RCI/B CN) 6:45am, C$0.65

- Chico’s FAS (CHS) 6:55am, $0.11

- El Paso Electric (EE) 7am, $0.19

- AGL Resources (GAS) 7am, $0.93

- Windstream (WIN) 7am, $0.20

- Dollar Tree (DLTR) 7:31am, $1.58

- Canadian Utilities (CU CN) 8:07am, C$0.95

- TJX Cos (TJX) 8:22am, $0.63

- MGM Resorts International (MGM) 8:30am, $(0.20)

- Washington Post (WPO) 8:30am, N/A

- Eaton Vance (EV) 9am, $0.43

- Analog Devices (ADI) 4pm, $0.48

- Equity One (EQY) 4pm, $0.28

- Whiting Petroleum (WLL) 4:00pm, $0.97

- Express Scripts (ESRX) 4:01pm, $0.85

- Jack in the Box (JACK) 4:01pm, $0.25

- Williams Cos (WMB) 4:01pm, $0.41

- Williams Partners LP (WPZ) 4:01pm, $0.98

- Fluor (FLR) 4:05pm, $0.82

- Hewlett-Packard (HPQ) 4:05pm, $0.87

- QEP Resources (QEP) 4:05pm, $0.45

- Flowserve (FLS) 4:09pm, $2.29

- Boston Beer (SAM) 4:15pm, $1.10

- Hertz Global Holdings (HTZ) 4:18pm, $0.20

- Yamana Gold (YRI CN) 4:28pm, $0.24

- Concho Resources (CXO) 4:30pm, $1.18

- Ltd Brands (LTD) 4:30pm, $1.46

- Continental Resources (CLR) 4:34pm, $0.78

- Liberty Global (LBTYA) 5:00pm, $0.16

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Record Nickel Supply Expanding Glut Thwarts Rally: Commodities

- Goldman Lowers Commodity Return Forecast, Stays Overweight

- Copper Falls as Chinese, European Manufacturing Keeps Shrinking

- Crude Oil Falls From Nine-Month High on Signs of Europe Slowdown

- Russia Seeks ‘Foothold’ in Asian Wheat Market to Rival U.S.

- Cocoa Climbs in London After Gains in New York; Sugar Advances

- Soybeans Decline as Rainfall in Argentina May Improve Crops

- Gold May Decline as Rally to Two-Week High Spurs Investor Sales

- BHP Billiton’s $5.25 Billion Bond Offer Leads New-Issue Revival

- Rubber Climbs to 5-Month High on Declining Supply, Greek Bailout

- Investor Rogers Compares Myanmar Reforms to China’s Opening

- Seaway Seen Sending Oil Supply to 5-Month High: Energy Markets

- Obama, Bush and Reagan Show Threat to Gold Run: Chart of the Day

- Spring Lambing in U.K. Turns Deadly as Schmallenberg Kills Young

- Russia to Keep Exporting Grain to Iran Unless UN Imposes Ban

- Shell Bids $1.6 Billion for African Oil Explorer Cove Energy

- Risk of Oil-Price Surge Rising on Supply, Goldman Sachs Says

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

YEN – complete meltdown on our immediate-term TRADE duration with the Japanese Yen in free-fall, accelerating to the downside this morning to 80.16 vs USD. At the same time, short-term UST’s are spiking above our TREND line of 0.26% and 10s are above the critical 2.03% line this morning. Big sovereign debt maturity spike in Japan in March.

MIDDLE EAST

The Hedgeye Macro Team