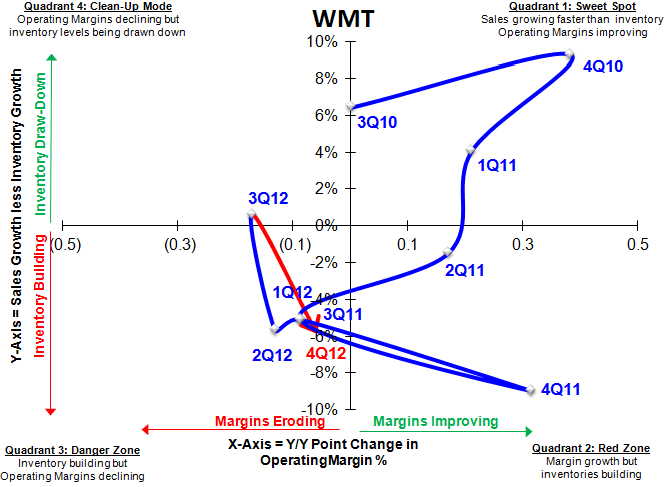

Mass (WMT) underperforms while high-end (M & SKS) charges on consistent with recent trends.

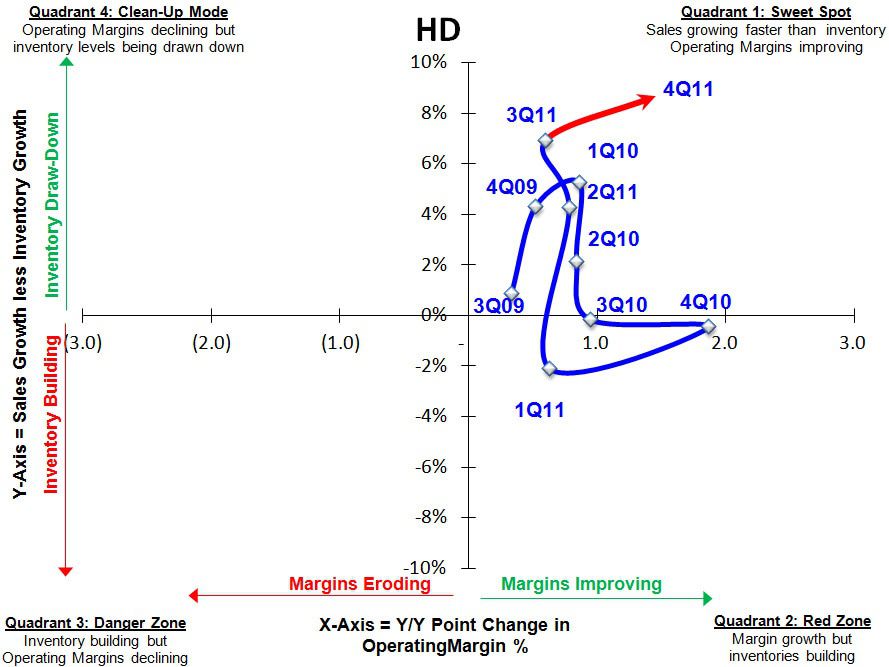

In light of HD’s strong quarter as well as M and SKS coming in better than expected, WMT’s underperformance is the clear callout from today’s earnings. Consistent with what we’ve been seeing across retail, inventory growth outpaced sales growth with HD the sole exception. That’s gross margin bearish for those companies not named HD. Interestingly, M cited a decision to hold onto cold weather apparel while SKS noted earlier receipts of Spring orders as a contributor to higher inventory levels at year-end - decisions don't that have the same risk profile. While HD and SKS both highlighted a more benign promotional environment, the mass channel continues to be highly price competitive and remains at greatest risk in the 1H from a margin perspective.

The most notable thematic category callout is undoubtedly Home. Yes, HD posted big numbers this quarter, but more notable was WMT posting the first positive comp in the Home category in over 2.5 years and M also highlighting category strength.

Here are a few company specific takeaways:

WMT: Walmart posted its second consecutive miss in as many quarters for the first time in five years reflecting a sequential revenue deceleration across all businesses despite favorable layaway sales. Headwinds in the form of tougher top-line comps and higher gas prices will remain challenging near-term. In addition, higher inventory levels driven by international growth up 25% was not simply due to Fx and acquisitions, which accounted for only 6pts of growth in the quarter. Despite favorable gross margin comps over the next few quarters, this development is gross margin bearish near-term.

- Inventory growth (+11.7%) not just acquisition related; int’l +18.6% ex Fx and Acq.

- Called out strength in basics category in Apparel.

- Home category posted first positive comp in 2.5yrs.

- Repurchased 23mm shs in Q4 = 115mm F12 = 3.2% of F11 shares outstanding and remains on track to go private within the next 9-10yrs.

- Outlook:

- 1Q13 guidance $1.01-$1.06 vs. $1.05E

- WMT US comps flat -to-+2%

- Sam's Club +3%-5%

- FY13 guidance $4.72-$4.92 vs. $4.90E

HD: Home Depot posted strong Q4 earnings of $0.50 ex items vs. $0.42E driven by notable top line performance with comps up +5.7% (vs. 2.2E). Strength in the top line was driven primarily by unseasonably warm weather (positive 200-250 bps impact in Q4) and resulted in a meaningful 200 bps acceleration in the underlying 2yr trend. The intermediate term setup over the next three quarters becomes progressively more favorable for both the top and bottom line with inventories well positioned into 2012 down 30 bps sequentially to -2.8% yy.

- HD leveraged SG&A nearly 100bps which, combined with gross margin expansion (+29bps vs. +26bpsE) drove operating margin expansion ahead of expectations +145bps vs. +68bpsE.

- Guided FY2012 EPS to $2.79 vs. $2.76E with the top line targeted to grow 4% vs. 3%E; Operating margin is expected to expand +50bps breaching the 10% margin rate one year ahead of the long term goal.

- 2012 promotional cadence expected to see no major differences relative to 2011.

- Management was “very pleased” with February trends Month-to date (Note: February comp is the most difficult in Q1 coming off 10% growth in January US store comp).

- 13/14 departments posted positive comps (8/13 outperformed the company average & 13/14 saw positive growth in total transactions) – Millwork sole negative underperforming dept.

- Positive comps in all 40 top US Markets- FL & CA saw 8thconsecutive quarter of comp growth indicative of widespread performance in markets less effected by weather related abnormalities.

M: EPS came in above expectations $1.70 (adj) vs. $1.65E driven by slightly better than expected gross margins (-33 bps vs. -50bpsE) and SG&A leverage.

- AURs +9%; Transactions +1%; UPT -4%.

- Starting to see impact of omni channel strategy benefit inventory turnover, which will be a key driver of gross margin expansion in ’12 as M enables nearly 300 stores to ship directly.

- Expect DTC to maintain current growth rates and exceed $2Bn in ’12.

- Q: Can you update us on price optimization?:A: “It's proven to be a little more complicated than we originally thought, but initial tests are looking good.” Needless to say, this initiative is not expected to yield benefits until 2H, but management appears to be hedging the magnitude a bit.

- Inventories were up +7.5% (down -2.1% seq) reflecting decision to hold onto cold weather apparel longer than usual. This could prove to be a savvy call, or added overhang in Q1. TBD.

- M Guided FY2012 EPS to $3.25-$3.30 vs. $3.27 and Comps +3.5% vs. +3.3E

SKS: EPS came in above expectations $0.17 (adj) vs. $0.14E driven by better than expected revenue growth (+6.8% vs. +4.5%E) and tight cost control (SG&A +4.7% vs. 15%E) offsetting weaker than expected gross margins (GM -21bps vs. -10bpsE).

- Categories of strength: women’s and men’s contemporary apparel, handbags, fine jewelry, fragrances, and men’s accessories

- NYC Flagship comps in-line with corporate avg.

- Project Evolution – SKS’ shift towards becoming an omni channel retailer will account for $30mm of total $110-$120mm in F12 CapEx and another $8mm in SG&A.

- Within read-to-wear, full-price selling is currently below expectations and could pressure Q2 GMs if persistent when seasonal clearance occurs. Thought to be a fashion move away from more classic brands.

- More notably in aggregate across categories, full-price selling is back to or above pre-recession levels.

- Inventories +7.5% (up 1.3pts seq) reflect earlier receipt of Spring orders accounting for ~1.5pts of increase. Which would you prefer to have on-hand, leftover winter apparel or upcoming Spring product? The tale of the tape will be gauged by the thermometer in Q1 between SKS and M.

- Maintaining 8% Operating margin goal and believe they can get there with current store base.

- SKS expects FY 2012 comps to be +5%-7% vs. 4.8E with Gross Margin up modestly over 40.8% in FY11 vs. +17E and SG&A as a percent of sales to be flat

Casey Flavin & Matt Darula