TODAY’S S&P 500 SET-UP – February 21, 2012

As we look at today’s set up for the S&P 500, the range is 13 points or -0.82% downside to 1350 and 0.13% upside to 1363.

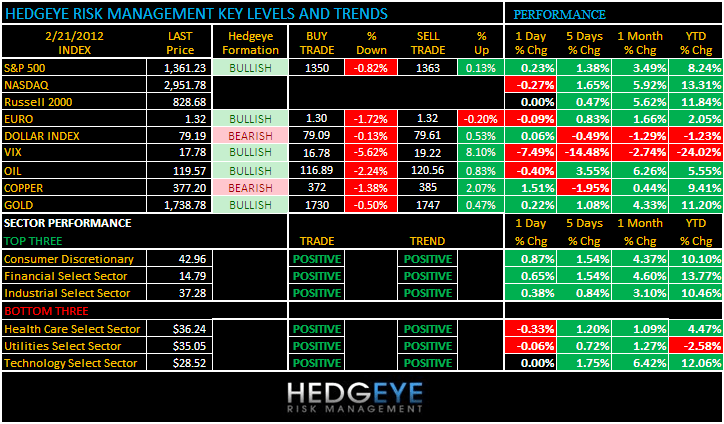

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 432 (-1109)

- VOLUME: NYSE 897.31 (11.36%)

- VIX: 17.78 -7.49% YTD PERFORMANCE: -24.02%

- SPX PUT/CALL RATIO: 2.31 from 1.45 (59.31%)

CREDIT/ECONOMIC MARKET LOOK:

10yr YIELD – this is the 2nd time this year that we’ve seen an intraday test of our 2.03% intermediate-term TREND line for 10yr Treasury yields. A sustained close > than this line could tip flows from bonds to stocks. But we need to see this confirm for at least 3 weeks in a row, not 6 hours.

- TED SPREAD: 41.68

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.03 from 2.00

- YIELD CURVE: 1.74 from 1.71

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed, Jan., est. 0.22 (prior 0.17)

- 11am: Export inspections: corn, soybeans, wheat

- 11:30am: U.S. to sell $33b 3-mo., $31b 6-mo. bills

- 1pm: U.S. to sell $35b 2-yr notes

GOVERNMENT:

- IAEA Inspectors return to Iran, Feb. 21-22

- House, Senate not in session

WHAT TO WATCH:

- Greece won a second bailout after European governments wrung concessions from private investors; European finance ministers approved $173b in aid

- Japanese billionaire Kazuo Okada, forced to sell stake in Wynn Resorts at discount, pledged to fight to protect his investment

- URS Corp. agreed to buy Flint Energy Services for C$1.25b

- Misys received rival bid from Vista Equity Partners, challenging previous agreement with Temenos

- TNT Express, in talks with UPS on takeover bid, said it plans to refocus operations in Europe

- FDA hosts media briefing on progress on drug shortages, noon

- China Telecom becomes second carrier in China to offer iPhone

- Barnes & Noble may give update on plans for its Nook e- reader unit when it reports 3Q results today

- Alibaba 4Q net income trails est.

- No U.S. IPOs scheduled: Bloomberg data

EARNINGS:

- Medco Health Solutions (MHS) 5:55 a.m., $1.17

- Dollar Thrifty Automotive Group (DTG) 6 a.m., $0.75

- Home Depot (HD) 6 a.m., $0.42

- Mylan (MYL) 6 a.m., $0.50

- Kraft Foods (KFT) 6:30 a.m., $0.57

- Rockwood Holdings (ROC) 6:30 a.m., $0.79

- Cracker Barrel Old Country Store (CBRL) 7 a.m., $1.14

- Dana Holding (DAN) 7 a.m., $0.38

- Wal-Mart Stores (WMT) 7 a.m., $1.45

- RadioShack (RSH) 7 a.m., $0.12

- Medtronic (MDT) 7:15 a.m., $0.84

- Clear Channel Outdoor Holdings (CCO) 8 a.m., $0.10

- Macy’s (M) 8 a.m., $1.65

- Saks (SKS) 8 a.m., $0.14

- Barnes & Noble (BKS) 8:30 a.m., $0.92

- Genuine Parts Co (GPC) 8:33 a.m., $0.83

- Expeditors International (EXPD) 9 a.m., $0.47

- Intuit (INTU) 4 p.m., $0.45

- Nabors Industries Ltd (NBR) 4 p.m., $0.50

- Chesapeake Energy (CHK) 4:01 p.m., $0.59

- Dell (DELL) 4:01 p.m., $0.52

- Brocade Communications Systems (BRCD) 4:04 p.m., $0.13

- Newfield Exploration Co (NFX) 4:04 p.m., $1.02

- HCC Insurance Holdings (HCC) 5 p.m., $0.67

- Range Resources (RRC) 5:06 p.m., $0.30

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – never in the history of Global Consumption has $100 handle per barrel (pick your flavor) not slowed Consumption. On the margin is where discretionary consumption matters and if we push toward $5 at the pump, we think you’ll see this time is not different. After being long Consumer Discretionary (XLY) for most of December-January (on Strong Dollar = Strong Consumption), we shorted it on Friday.

- Record Rice Crop Boosting Stockpiles to Decade High

- Oil Trades Near Nine-Month High as Europe Reaches Greek Aid Deal

- Copper Gains for a Second Day as Greece Wins Another Bailout

- Commodities Rally to Highest in More Than Six Months on Greece

- Soybeans Gain on Dry Weather in South America, China’s Purchase

- Gold Imports by India Seen Declining From Record on Prices

- Australia Seen Gaining Asian Wheat Market Share From U.S.

- Robusta Coffee Falls as Vietnam Sales May Advance; Cocoa Rises

- Gold May Gain a 2nd Day as Commodities Climb on Greece Bailout

- Copper Imports by China Decline for First Time in Eight Months

- Coal to India Beating China on Supply Shortfall: Energy Markets

- BP’s Maple Bonds Expose Drought Carney Frets: Canada Credit

- Russia Has Enough Grain to Continue Exports, Minister Says

- Raw Materials Rally as Greece Wins Bailout

- Oil Profits Slide Fastest Since Lehman Collapse on Gas: Energy

- Billionaire Fredriksen Sees Golar LNG Rates Surging: Freight

CURRENCIES

EUROPEAN MARKETS

FRANCE – now that we have a +18% German DAX rally (YTD) out of the way (Greece was +23% at its YTD peak), we can focus on separating the weak parts of European growth from the strong (Germany). France’s CAC40 fails to breakout above its long-term TAIL of 3565 resistance again. Growth Slowing in France is a major problem – so is Hollande’s continued momentum in the polls vs Sarkozy.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team