February projection raised to 11-17% YoY growth.

Macau logged another big week, causing us to raise our February forecast yet again. We are now projecting full month February GGR will be in the range of HK$21.5-22.5 million, up 11-17% YoY.

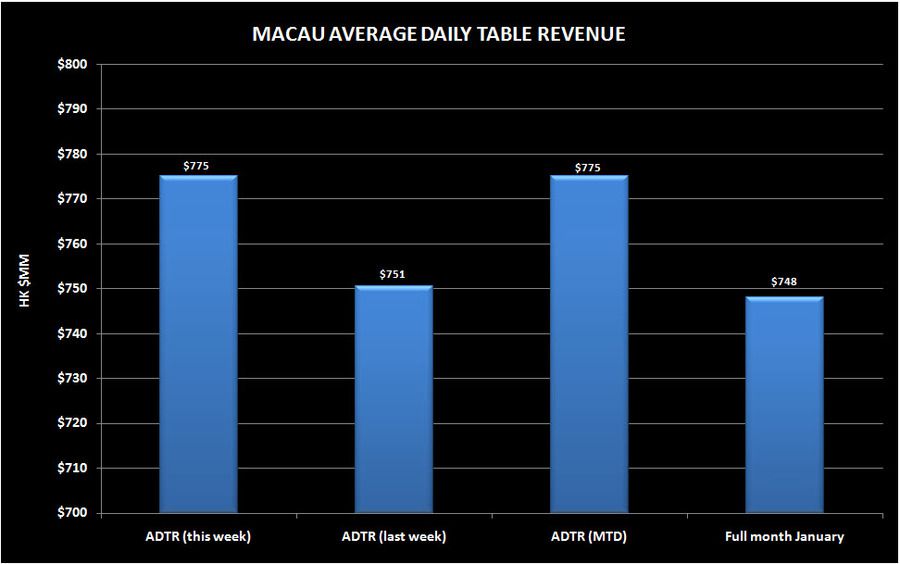

This past week, average daily table revenues (ADTR) were HK$775 million compared to HK$751 million the prior week. Month to date, ADTR was HK$775 million compared to HK$748 million for all of January.

In terms of market share, MGM was the big loser, dropping 200bps in one week. Galaxy lost more share this past week and its February share remains well below recent trend. MPEL and Wynn both gained share again as MPEL approaches its recent trend rate and Wynn remains above. LVS increased its share slightly and is in striking distance of its January share of 18.2%.