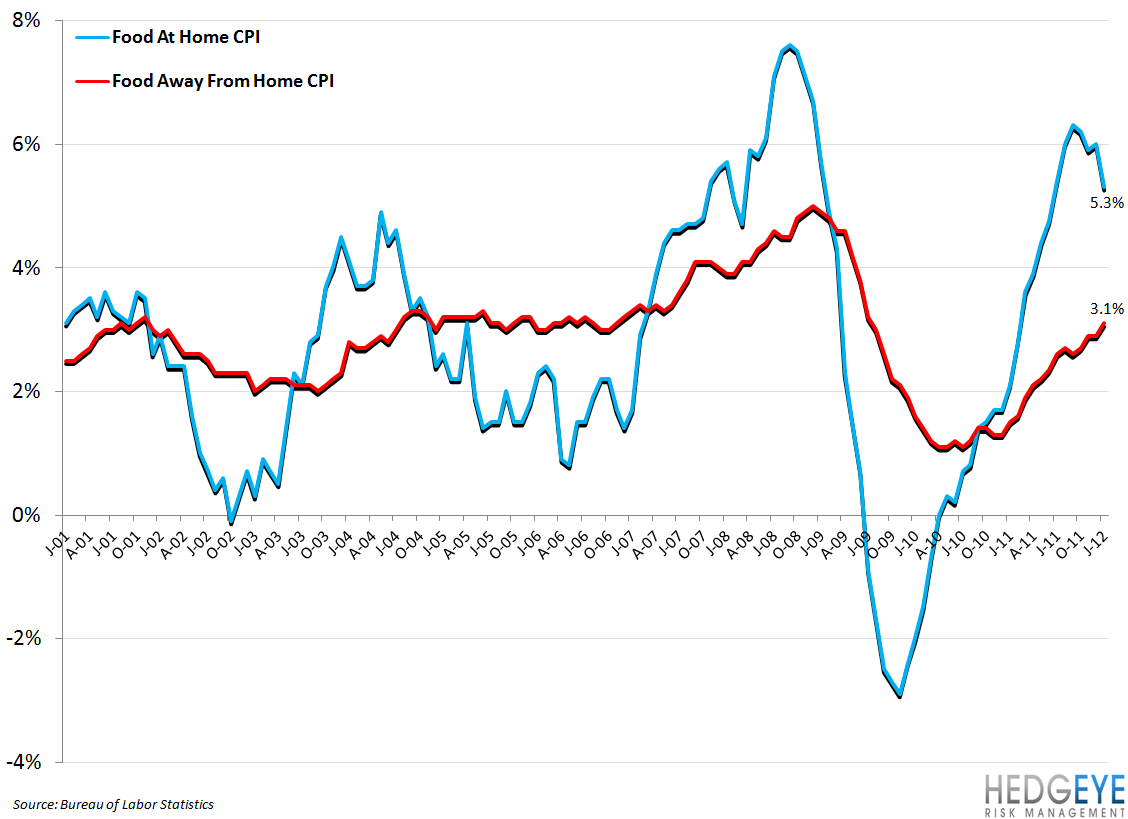

In January, Y/Y CPI growth for Food at Home decreased by 70 basis points to 5.3% from 6.0% in December. CPI for Food Away from Home gained 20 basis points to 3.1% from 2.9% in December.

This is a trend that we are continuing to monitor closely. 2011 was a year where restaurant margins were impacted by inflation but, due to strong top line trends, rising food costs did not have as severe an impact on earnings as some were anticipating. Management teams in the grocery space took significant levels of pricing during 2011 and we believe that this was a factor in helping restaurants attract customers. Food Away from Home CPI was far more benign as restaurant companies prioritized traffic over margin. Our view in 2012 is that, if the spread between these two CPI data points continues to narrow, the competitive benefit that the restaurant companies enjoyed in 2011 will shrink and any exposure to inflation will be felt more acutely on the bottom line.

As JACK CFO Jerry Rebel said on a recent earnings call, management teams pay close attention to this data when thinking about pricing so we will continue to monitor these trends closely.

Howard Penney

Managing Director

Rory Green

Analyst