This note was originally published at 8am on February 03, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“With the fearful strain that is on me night and day, if I did not laugh I should die.”

-Abraham Lincoln

In one of my favorite books, Team of Rivals, by Doris Kearns Goodwin, you get an introspective sense of Lincoln as a human being. To me, his greatest leadership quality was being a realist. That’s different than being an optimist.

If I wasn’t optimistic about my family, partners, and firm, I wouldn’t have invested most of my net wealth into building this company. It wasn’t easy committing free-market capital that could fail during the thralls of 2008. But I wouldn’t have done this if it was. The fearful strain that we bear, night and day, is the most important part of who we are and what we create.

In Chapter 5 of “Thinking, Fast and Slow”, Daniel Kahneman explains the difference between being at Cognitive Ease and experiencing Cognitive Strain. “Cognitive strain is affected by both the current level of effort and the presence of unmet demands.” And “easy is a sign that things are going well – no threats, no major news, no need to redirect attention or mobilize effort.” (page 59)

Easy is as easy does. There is nothing easy about being a leader in this country who has to deal with this market and meet a payroll every month. Don’t ask a talking head or a politician in America about that. They have no idea what it means to sit in this seat every morning embracing the uncertainties of whatever risks the next central plan brings.

Back to the Global Macro Grind…

I’m personally experiencing Cognitive Strain this morning – I have to deal with being short the SP500, the daily dirty laundry list of threats to my company’s competitive position, and whatever this power-ball ticket on the US Employment Report brings at 830AM.

And I like it …

There’s no whining in winning. No matter what you throw at my senior management team every morning, we’ll suck it up and turn that into our own positive momentum. There a plenty of good teams in this business. Only the great ones get how to work together.

Back to this short SPY position.

What do I do with it this morning if the employment report is better than expected? What do I do if it’s worse?

Actually, the answer to those 2 questions is precisely why I have the position on – under both scenarios I know exactly what I am going to do. These are the risk management setups that we spend hundreds of hours preparing for. Very infrequently do Short Selling Opportunities like this present themselves with these odds.

That doesn’t mean the market is going to blow up. All it means is that my probability-weighted setup won’t get me run-over if I am wrong. No one ever went broke booking a gain either.

Across my three core risk management durations (TRADE, TREND, and TAIL), here are the scenarios I’m looking at:

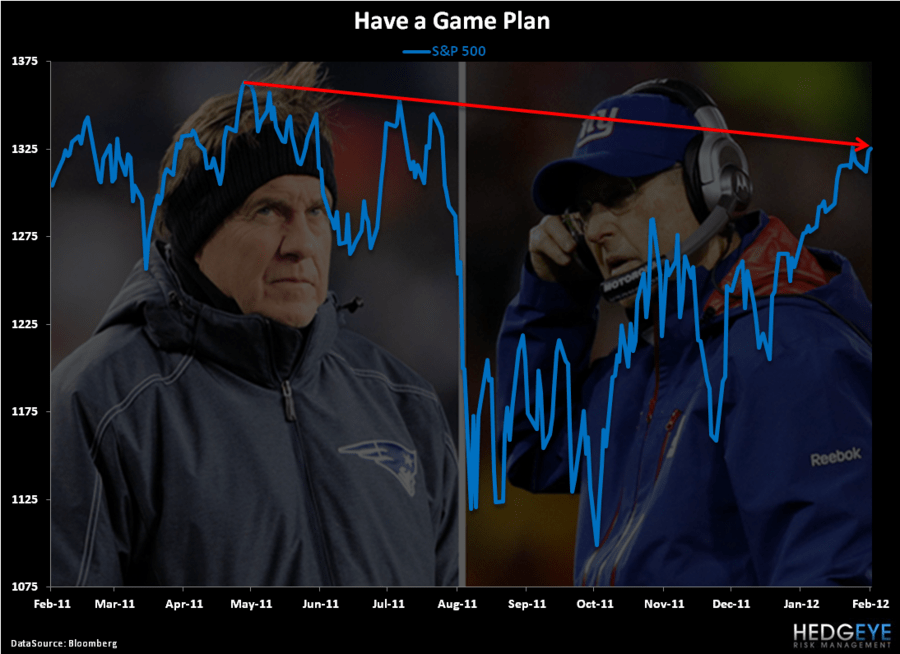

- SP500 goes up – I wait and watch for 1333, and short it again there (lower long-term high)

- SP500 goes up, and up – I wait and watch for 1363, and short it again there (lower long-term high)

- SP500 goes down – I wait and watch for 1318 to hold – if it does, I book the gain – if it doesn’t I smile

It’s really not that complicated. There really is no Cognitive Strain associated with the SPY position itself. My personal strain tends to be cumulative. It occurs when everything else about running my company hits me from all directions at once, and then – bang! A central planner says or does something that I didn’t see coming.

I’m not alone in this country thinking about stress this way. I’ll bet that 100% of small business owners agree with me on this. How do I deal with Cognitive Strain perpetuated by the Bernankes and Geithners of this world? Follow me on Twitter, and you’ll figure that out in a hurry. “If I did not laugh,” I’d hand in the keys to this Made in America company to Wesley Mouch.

My immediate-term support and resistance lines for Gold, Oil (Brent), EUR/USD, Shanghai Composite, and the SP500 are now $1721-1779, $110.84-112.36, $1.30-1.32, 2282-2344, and 1318-1333.

Best of luck out there today and enjoy watching some Red, White, and Blue Leadership on the field on Sunday,

KM

Keith R. McCullough

Chief Executive Officer