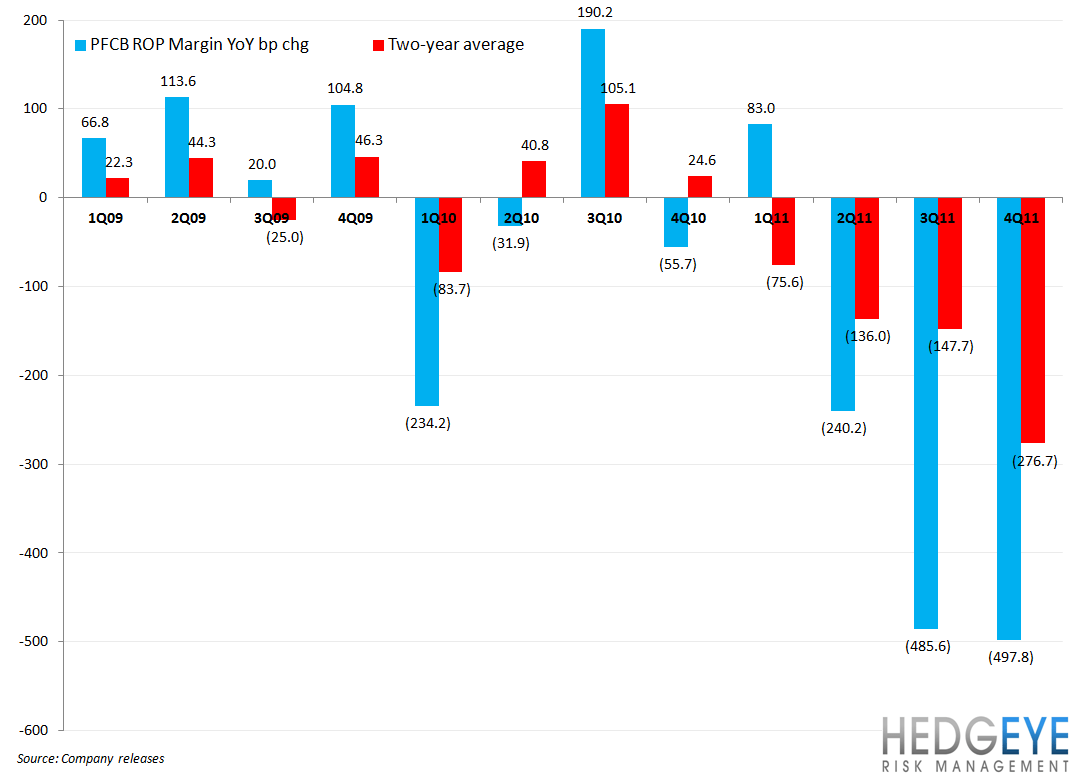

As we have been writing consistently in the run up to today’s earnings, we are buyers of PFCB on down days over the next three months (TREND duration). 4Q11 performance was below consensus, with EPS ex-items of $0.30 versus $0.45 consensus. Management’s statement at the top of the press release, that 2012 will be an inflection point, was lent credence by top-line beats at the Bistro and at Pei Wei in 4Q11 as well as positive commentary on current trends at both concepts. While 4Q11 results were disappointing from an EPS perspective, management articulated a comprehensive plan to fix the P.F. Chang’s Bistro brand and provided evidence that the plan is working. Given that PFCB is trading at 6.1x EV/EBITDA NTM versus one of the worst run companies in the restaurant space (RT) at 6.6x, we continue to believe this gap will close as people become more comfortable with management’s strategy to turn around both concepts. Today, management also upped the dividend by 10% so the stock has a yield of 3.2%.

Nearly every restaurant concept gets a second chance; for the P.F. Chang’s brand its time is getting closer. There remains much work to be done but the risk/reward favors the longs at this price.

Coming into today, the street was not in tune to the reality of the current numbers thus the miss relative to consensus. It was really hard to get aggressively long the stock ahead of this quarter, but we believe the stock is near the bottom from an earnings revisions standpoint and may even overshoot to the downside given the severe bearishness surrounding the stock. That being said, we’re betting that the turn in operating performance for PFCB will begins to take hold in 2012. As management suggested today, that will be more evident in 2H12. If the current initiatives are real and sustainable 2012 will be the inflection point for PFCB.

PFCB is focused on altering the price value proposition in four core areas:

- Menu innovation

- Improved service

- Lower price dining options

- Reimaging of the restaurants base

At the PF Chang’s concept initiatives have led to a number of changes:

- Introduction of the specific lunch menu (increase frequency)

- The Irvine Project (elevate the guest experience)

- Investments in both labor and technology (focus on guest satisfaction)

- Broader brand marketing (more communication with customers)

At Pei Wei the changes include:

- Rollout of new small plates

- Introduction of a lower priced complete meal offering called Diner Selects

- Advanced plans for a new Pei Wei format called Pei Wei Asian Market

- New LTO - Thai Basal Chicken

PFCB has launched a more compelling lunch experience with lower priced offerings (smaller portions), faster ticket times, and more lunch-specific menu items. The test includes 20 menu items served with a choice of soup or salad, each priced under $10 in stores throughout Arizona and two stores in Dallas; the test included a marketing campaign on television, radio, print ads, billboard and social media. The tests have driven guest traffic up around 20% at lunch, which more than offset the average check declined 10%, leaving lunch with positive comps around 10%. The company plans to introduce the new lunch menu across the Pei Wei system.

As we have written before, the benefits of the Irvine Project will be broad and varied. The exercise is allowing management to plan meticulously for the reimaging and remodeling program that is expected to elevate the Bistro business. Using the Irvine Project as an example, management is selecting the best aspects of that design and incorporating them into the system-wide program. Along with the new look and feel of the restaurant itself, changes at the Bistro will include a new menu with enhanced small plates, a separate lunch menu, a new wine list and enhanced beer selection, new staff uniforms, and an updated music system. In short, the restaurant is still called P.F. Chang’s but almost everything everything else that the customer sees has changed: new look restaurant, staff, menu, and new music. All of this equals a new customer experience.

April 2nd will be an important date to be aware of as management will launch the Bistro Triple Dragon initiative which blends “a number of the key initiatives including our new lunch menu, some of the best items from our innovation Bistro menu; new music and a new look for our service teams. All of these are designed to elevate our guest experience and energize our employee team”.

The company is planning significant media support behind the April 2nd launch of the Triple Dragon initiative to help ensure that the changes are effectively communicated. A second initiative is being planned for the fall which will include adding sushi and other vegetarian items to the menu. Consumer research conducted by the company has indicated that these items would be well-received by customers.

Turning to Pei Wei, the company had previously expressed awareness that the price-value proposition at the concept needed improvement. Along those lines, on October 10th, management rolled out several new lower priced menu offerings to the entire Pei Wei system. This initiative was labeled “Diner Selects” and a 400 basis point improvement in traffic and a “negligible” decline in average check at Pei Wei since October 10th, as a result of the initiative, was underscored by management. The initiative was supported by nationwide marketing. “Diner Selects” has a starting price point of $6.25 and features five (smaller portions) of signature entrees combined with rice and the customer’s choice of a spring roll, soup, or Asian slaw. There are also three new small plates included in the offering that are priced at $3.95 each.

The most important initiative at Pei Wei is the introduction of the Pei Wei Asian market which is a higher margin form of the current Pei Wei format. According to management, Pei Wei Asian Market was developed based on direct consumer research and addresses both price point and speed of service issues that were identified as main barriers to greater guest of frequency at Pei Wei. The new format gives the company greater real estate flexibility and carries a smaller store footprint of about 2,500 square feet versus the current format’s area of 3,200 square feet. The end game is that the concept will carry higher operating margins as well as a lower sales hurdle requirement than the existing store base. Importantly, management is changing three or four of the planned new stores for 2012 are Pei Wei Asian Market.

The Global Brands business continues to perform exceptionally well, with the company seeing accelerated development in 2012 and beyond. Additionally, the company ended the year with $50 million in cash and announced it will be buying back 16% of the current enterprise vale on the company as soon as they can.

There is no question in my mind that there are still a number of skeptics about the PFCB turnaround plan. After all, the stock is at the bottom of our Hedgeye Restaurants Sentiment Score Card. 4Q11 was a mess and 1Q12 will likely be another. After that, we expect better sales trends and margins at the Bistro and Pei Wei to head back to 18% and 16%, respectively. Rarely does anything move in a straight line, but we think that earnings revisions are now in a bottoming process and The Queen Mary (2/6 post) is starting to turn.

Howard Penney

Managing Director

Rory Green

Analyst