RevPAR and Baccarat have been the focus areas of investors but high margin slot revenue has been quietly creeping up and growth looks sustainable.

Could slots be the next big thing? We think slots will be the big delta for the Strip and relative to expectations and margins, that’s where the leverage is. Consider this, the incremental margin on an increase in slot play per visitor is around 90%. The incremental margin on an increase in slot play due to an additional visitation is nearly the same. There is no other important revenue driver in Las Vegas that has this type of economics.

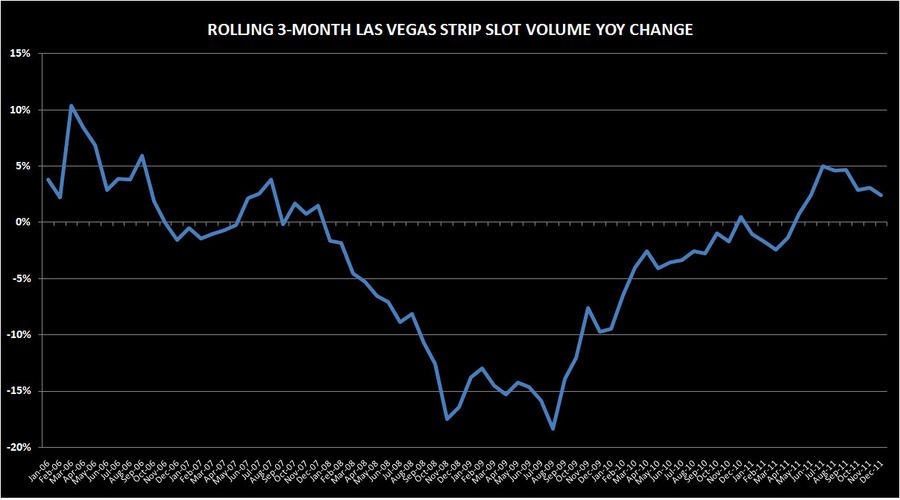

Without a doubt, slots are a profitable business. Yet, they’ve been in a long time slump, until recently. Every other Las Vegas revenue driver has been in recovery mode for some time. Slot volume growth was consistently negative from November 2007 until October 2010 (with the exception of a slight gain in February 2010). Since then they've been inconsistent. It’s only during the 2nd half of 2011 did we see more a trend of positivity. We think 2012 will be the first meaningfully positive year for slot growth since 2006.

The following chart shows the recent monthly performance of the Strip’s slot business and our projections for 2012. We model sequential seasonality using a 3 month moving average, adjusted for historical seasonality and GDP. We would caution that the monthly projections can be volatile but directionally, our model has been accurate. For instance, we think it is unlikely that we will see a double digit growth month, but we do think March growth will accelerate. Annually, our model is less volatile and is currently projecting 2012 growth of 4-5%.

Most importantly, if the slot business recovers as we expect, the flow through should be a major tailwind for Strip earnings (MGM and the 2nd derivative, BYD) and the stocks with significant exposure to the Strip. There is still a long way to go for slot volume. In Q4 2011, slot volumes were 21% lower than levels achieved in Q4 2006. If our projection for 2012 is met, slot volumes would still be 19% below 2007. Now if only the Macro will behave.