THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer

For the week ended 2/11, initial jobless claims came in at 348k versus expectations of 365k and 361k the week prior (revised from 358k).

Comments from CEO Keith McCullough

Consensus still focused on Greece and Rating Agency noise as Global Growth Slows – amazing:

- CHINA – after seeing its 1st y/y decline in Export growth in 2yrs (JAN -0.5%), this morning the Chinese reported a y/y decline in Foreign Direct Investment of -0.3% y/y. Chinese govt guys called it “grim” (see Bloomberg article) – volumes on the NYSE aren’t the only thing in the world that have slowed to a halt

- SPAIN – the Spaniards are selling as much pig paper as they can (34% of their YTD needs) before someone figures out that Growth Slowing is what is going to crush their citizenry next. This morning’s debt auction finally came in at a higher yield (2015 bonds at 3.33% vs 2.86% last) and the IBEX is the 1st major European mkt to snap my immediate-term TRADE line of 8653 (down -2.1% leading decliners in Europe).

- COPPER – breaking my mo mo line of 3.88/lb support was one of the many Growth Slowing signals that had me short SPY at 1355 yesterday. This morning, copper = down -1.1% and 10yr UST yields are straight down to 1.91% as well.

Japanese Yen down hard too. We’ll likely buy/cover on red today, but not because Global Growth isn’t slowing as inflation expectations accelerate.

KM

SUBSECTOR PERFORMANCE

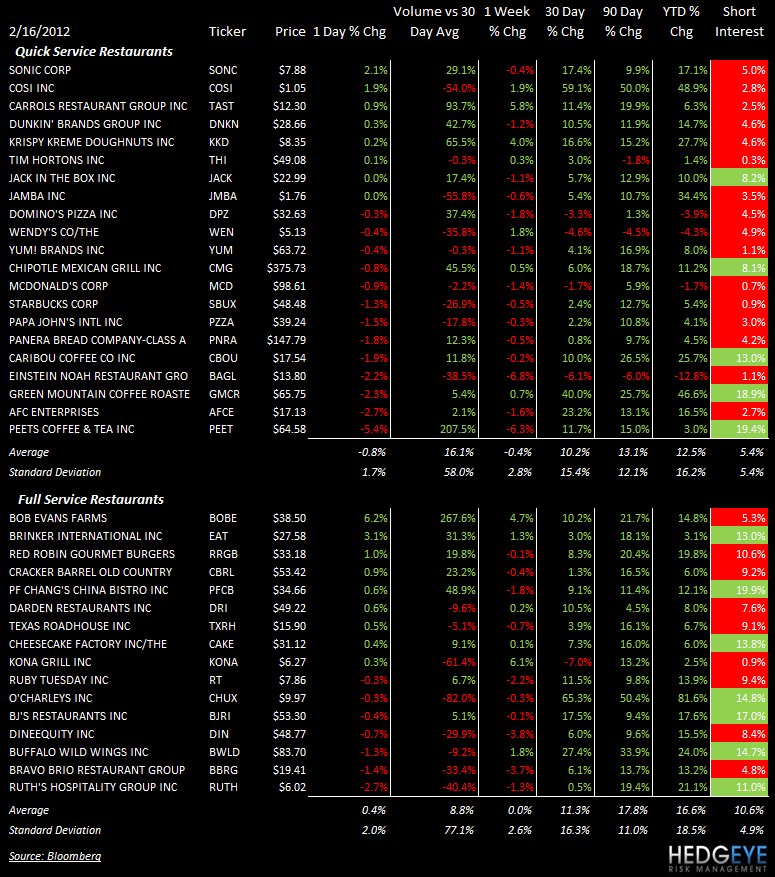

QUICK SERVICE

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

PEET: Peet’s Coffee traded down on accelerating volume on disappointing earnings yesterday.

CASUAL DINING

PFCB: P.F. Chang’s 4Q11 earnings hit the tape this morning. EPS came in at $0.30 ex-items versus $0.45 consensus. Comps at the Bistro came in at -2.4% versus -2.8% consensus. Pei Wei comps came in at -1.9% versus -2.7% consensus. The stock traded down on the print but is now up 4% in premarket trading. On the call, management is providing some positive commentary on the company’s outlook. We will have a more detailed post up later today.

BOBE: Bob Evans reported strong EPS of $0.69 versus $0.60 expectations on Tuesday and followed it up with a positive conference call yesterday, sending the stock higher. The company improved food and labor costs at both Bob Evans and Mimi’s Café.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

BOBE: Bob Evans Farms’ stock increased by 6.2% on accelerating volume.

EAT: Brinker management was in NYC yesterday and must have had some positive things to say.

PFCB: P.F. Chang’s eked out a small gain yesterday ahead of the print this morning. As we wrote above, initial reaction to the print was negative but the bid is above $36 as we approach the opening bell.

Howard Penney

Managing Director

Rory Green

Analyst