TODAY’S S&P 500 SET-UP – February 16, 2012

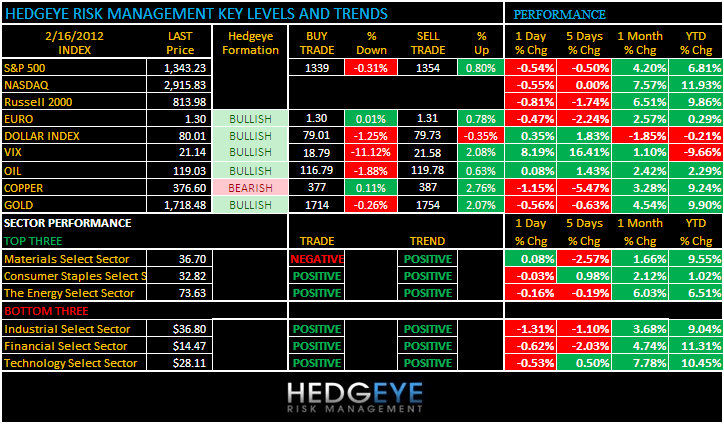

As we look at today’s set up for the S&P 500, the range is 15 points or -0.31% downside to 1339 and 0.80% upside to 1354.

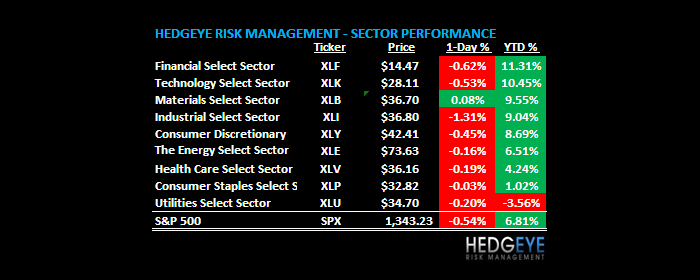

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -468 (347)

- VOLUME: NYSE 806.39 (8.45%)

- VIX: 21.14 8.19% YTD PERFORMANCE: -9.66%

- SPX PUT/CALL RATIO: 2.40 from 1.53 (56.86%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 38.83

- 3-MONTH T-BILL YIELD: 0.11%

- 10-Year: 1.91 from 1.93

- YIELD CURVE: 1.65 from 1.67

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: PPI, M/m, Jan., est. 0.4% (from -0.1%)

- 8:30am: Jobless Claims, wk of Feb. 11, est. 365k (prior 358k)

- 8:30am: Housing Starts, Jan., est. 675k (prior 657k)

- 8:30am, Building Permits, Jan., est. 680k, (prior 671k revised)

- 9:00am: Bernanke speaks on community banking in Arlington, Va.

- 9:45am: Bloomberg Consumer Comfort, week Feb. 12, est. -42.0 (prior -41.7)

- 10am: Philadelphia Fed., Feb., est. 9.0 (prior 7.3)

- 10am: 30-yr mortgage rates, Freddie Mac

- 10:30am: EIA natural gas storage

- 1pm: U.S. to sell $9b 30-yr TIPS

- U.S. Treasury to announce 2-, 5-, 7-yr auction sizes

GOVERNMENT:

- President Obama attends campaign events in California

- Chinese Vice President Xi Jinping visits Iowa

- House, Senate in session:

- House Energy and Commerce Committee hears from FCC Chairman Julius Genachowski on its budget. 9am

- Senate Energy Committee hears from Energy Secretary Steven Chu on the Energy Department’s 2013 budget request. 9:30am

- Senate Budget Committee hears from Treasury Secretary Timothy Geithner on the president’s 2013 budget request. 10am

- House Homeland Security Committee holds hearing on monitoring of social networking and media. 10am

- House Appropriations subcommittee hears from Defense Secretary Leon Panetta and Joint Chiefs Chairman Martin Dempsey on the 2013 defense budget request. 10am

- House Appropriations Committee hears from Interior Secretary Ken Salazar on his department’s budget request. 1:30pm

- House Budget Committee hears from Treasury Secretary Timothy Geithner on the president’s budget request. 2pm

- Senate Homeland Security Committee hears from Homeland Security Secretary Janet Napolitano on Cybersecurity Act. 2:30pm

WHAT TO WATCH:

- Europe is set to make “all the necessary decisions” on Greece rescue on Feb. 20: Luxembourg prime minister

- Morgan Stanley, UBS may be cut up to three levels by Moody’s

- U.S. officials said to have intensified their focus on banks, Taiwan in insider-trading probe

- Summers, Clinton said to be lead contenders for World Bank president

- IAG says taking AMR stake in bankruptcy is “not on table”

- Florida foreclosures climb 14% as lenders resume home seizures: RealtyTrac

- House-Senate negotiators announce payroll deal completed

- ABB falls as 4Q results show margin pressure

- Cap Gemini reaches 6-month high on higher margin forecast

EARNINGS:

- Huntsman (HUN) 6am, $0.28

- Nexen (NXY CN) 6am, C$0.44

- SPX (SPW) 6am, $1.75

- DENTSPLY International (XRAY) 6am, $0.52

- Penn West Petroleum Ltd (PWT CN) 6:30am, C$0.15

- Barrick Gold (ABX CN) 7am, $1.26

- Discovery Communications (DISCA) 7am, $0.69

- DTE Energy (DTE) 7am, $0.80

- Duke Energy (DUK) 7am, $0.22

- Frontier Communications (FTR) 7am, $0.05

- OGE Energy (OGE) 7am, $0.35

- JM Smucker (SJM) 7am, $1.41

- TRW Automotive Holdings (TRW) 7am, $1.55

- VF (VFC) 7am, $2.31

- DirecTV (DTV) 7:30am, $0.92

- General Motors (GM) 7:30am, $0.41

- Hyatt Hotels (H) 7:30am, $0.13

- Health Care REIT (HCN) 7:30am, $0.90

- Progress Energy (PGN) 7:30am, $0.53

- Molson Coors Brewing (TAP) 7:30am, $0.70

- Waste Management (WM) 7:30am, $0.60

- Apache (APA) 8am, $2.87

- Reliance Steel & Aluminum (RS) 8:50am, C$0.78

- Finning International (FTT CN) 8:56am, $0.34

- PG&E (PCG) 9:04am, $0.85

- CI Financial (CIX CN) 11:17am, C$0.31

- Advance Auto Parts (AAP) Pre-Mkt, $0.75

- Nordstrom (JWN) 4pm, $1.10

- Allscripts Healthcare (MDRX) 4pm, $0.25

- DaVita (DVA) 4:01pm, $1.49

- Aruba Networks (ARUN) 4:03pm, $0.15

- Applied Materials (AMAT) 4:04pm, $0.12

- SunPower (SPWR) 4:05pm, $(0.06)

- Baidu (BIDU) 4:30pm, $5.69

- EOG Resources (EOG) 4:35pm, $0.87

- Fairfax Financial Holdings Ltd (FFH CN) 5:01pm, $(2.60)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – breaking our mo mo line of 3.88/lb support was one of the many Growth Slowing signals that had us short SPY at 1355 yesterday. This morning, copper = down -1.1% and 10yr UST yields are straight down to 1.91% as well.

- Biggest Mining Deals No Promise of Xstrata Bonanza: Commodities

- Oil Declines From Five-Week High After Greek Bailout Delayed

- China May Become World’s Biggest Gold User, Beating India

- Commodities Drop From Six-Month High on Greek Default Concern

- Gold Drops as Greece Bailout Concerns Boost Demand for Dollar

- Soybeans Drop as Debt-Crisis Concerns Eclipse China’s Purchases

- Robusta Coffee Swings Between Gains, Losses; Cocoa Retreats

- U.K. Natural Gas Contracts Decline on Lower Demand; Power Falls

- U.S. Says Iran’s Nuclear Breakthrough Is ‘Hype;’ Oil Pares Gain

- Spain’s Cepsa Secures Crude From U.A.E. in Case of Iran Loss

- Barrick Gold Earnings Trail Estimates as Mining Costs Increase

- Rising Pump Prices in China to Cut Refining Loss: Energy Markets

- Impala Calls for Help to Restart World-Biggest Platinum Mine

- China Seen Topping India This Year on Gold

- Gold Demand Fell 2.1% in Fourth Quarter on Jewelry, WGC Says

- NYSE Liffe Wants to Start Delivery Limits on London Commodities

- Malaysian Palm-Oil Exports Seen Rising 10%, Paring Reserves

CURRENCIES

EUROPEAN MARKETS

SPAIN – the Spaniards are selling as much pig paper as they can (34% of their YTD needs) before someone figures out that Growth Slowing is what is going to crush their citizenry next. This morning’s debt auction finally came in at a higher yield (2015 bonds at 3.33% vs 2.86% last) and the IBEX is the 1st major European market to snap my immediate-term TRADE line of 8653 (down -2.1% leading decliners in Europe).

ASIAN MARKETS

CHINA – after seeing its 1st y/y decline in Export growth in 2yrs (JAN -0.5%), this morning the Chinese reported a y/y decline in Foreign Direct Investment of -0.3% y/y. Chinese government guys called it “grim” (see Bloomberg article) – volumes on the NYSE aren’t the only thing in the world that have slowed to a halt.

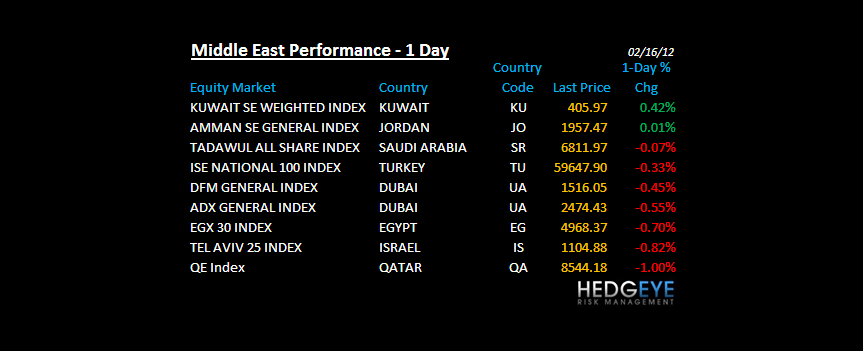

MIDDLE EAST

The Hedgeye Macro Team