TODAY’S S&P 500 SET-UP – February 15, 2012

As we look at today’s set up for the S&P 500, the range is 15 points or -0.41% downside to 1345 and 0.70% upside to 1360.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -815 (-2422)

- VOLUME: NYSE 743.55 (8.92%)

- VIX: 19.54 2.63% YTD PERFORMANCE: -16.50%

- SPX PUT/CALL RATIO: 1.53 from 2.38 (-35.71%)

CREDIT/ECONOMIC MARKET LOOK:

10yr – the bond market says Growth Slowing is a bigger problem than inflation rising. UST 10yr is now breaking our only line of remaining support (1.96%) into a Bearish Formation (bearish yields on all 3 risk mgt durations – TRADE, TREND, and TAIL), so this will be a very interesting day. Bond yields breaking down have front run US Growth expectations for a long time now.

- TED SPREAD: 39.08

- 3-MONTH T-BILL YIELD: 0.11%

- 10-Year: 1.94 from 1.94

- YIELD CURVE: 1.67 from 1.65

MACRO DATA POINTS (Bloomberg Estimates):

- 5:30am: Bank of England releases growth, inflation forecasts

- 7am: MBA Mortgage Applications, prior up 7.5%

- 8:30am: Empire Manufacturing, Feb., est. 15 (prior 13.48)

- 9am: Net Long-term TIC Flows, Dec., est. $45b (prior $59.8b)

- 9:15am: Industrial Production, Jan, est up 0.7% (prior up 0.4%)

- 9:15am: Fed’s Fisher speaks in San Marcos, Texas

- 10am: NAHB Housing Market index, Feb., est. 26 (prior 25)

- 10:30am: DoE crude inventories,e st. build 1600k (prior build 304k)

- 2pm: FOMC minutes from Jan. 24-25 meeting

GOVERNMENT:

- Treasury Secretary Tim Geithner, Defense Secretary Leon Panetta, HHS Secretary Kathleen Sebelius, other Cabinet officials testify before Congress on Obama budget, 10am

- Chinese Vice President Xi Jinping delivers address at U.S.- China Business Council luncheon, noon

- Senate, House in session

WHAT TO WATCH:

- U.S. industrial production may have accelerated 0.7% in Jan., economists est., would be biggest gain in six months

- German, Franch 4Q GDP beats ests., Italy slips into recession; euro-area economy shrinks 0.3%

- Obama tells Xi China’s rise comes with duty on trade, rights

- Yahoo-Alibaba talks falter as investor steps up pressure

- U.S. investigating Goldman analyst on insider tips, WSJ says

- Berkshire takes Liberty Media, DaVita stakes as Weschler joins

- LightSquared to be blocked by FCC after U.S. interference report

- Citigroup, others release monthly credit-card delinquencies, charge-offs

- Nasdaq, Bats websites attacked; trading systems unaffected

- China pledges to invest in Europe’s bailout funds, hold euros

- Goldman Sachs Technology and Internet Conference includes presentations from Microsoft, Cisco, eBay

EARNINGS:

- Cimarex Energy (XEC) 6 a.m., $1.31

- Cenovous (CVE CN) 6 a.m., $0.53

- Calumet Specialty Products (CLMT) 6:30 a.m., $0.48

- WellCare (WCG) 6:30 a.m., $1.19

- Amtrust Financial Services Inv (AFSI), 7 a.m., $0.63

- Comcast (CMCSA) 7 a.m., $0.42

- Deere (DE) 7 a.m., $1.24

- Incyte (INCY) 7 a.m., ($0.41)

- Abercrombie & Fitch (ANF) 7 a.m., $1.12

- Henry Schein (HSIC) 7 a.m., $1.12

- Avista (AVA), 7:05 a.m., $0.45

- Penske Automotive (PAG) 7:25 a.m., $0.41

- Owens Corning (OC) 7:30 a.m., $0.48

- Watsco (WSO), 7:30 a.m., $0.34

- Scana (SCG) 7:30 a.m., $0.78

- Atlas Air Worldwide Holdings (AAWW) 7:37 a.m., $1.91

- Devon Energy (DVN) 7:55 a.m., $1.49

- Six Flags Entertainment (SIX) 8 a.m., ($0.86)

- Dr Pepper Snapple (DPS) 8 a.m., $0.74

- Dean Foods (DF) 8 a.m., $0.23

- Mine Safety Appliances (MSA) 8:30 a.m., $0.59

- Allete (ALE) 8:30 a.m., $0.57

- Clearwire (CLWR) 4 p.m., ($0.37)

- Itron (ITRI) 4 p.m., $1.00

- Stifel Financial (SF) 4 p.m., $0.43

- NetApp (NTAP) 4 p.m., $0.58

- Trinity Industries (TRN) 4:01 p.m., $0.44

- CBS Corp (CBS) 4:01 p.m., $0.53

- Hanesbrand Inc. (HBI) 4:01 p.m., $0.51

- Ancestry.com Inc (ACOM) 4:01 p.m. $0.34

- Athenahealth (ATHN) 4:01 p.m., $0.24

- Equinix (EQIX) 4:01 p.m., $0.46

- Netlogic Microsystems (NETL) 4:02 p.m., $0.37

- Glimcher Realty Trust (GRT) 4:02 p.m., $0.21

- Jarden Corp. (JAH) 4:05 p.m., $0.91

- Morningstar Inc. (MORN), 4:05 p.m., $0.56

- Russel Metals (RUS CN) 4:05 p.m., $0.40

- Agilent Technologies (A) 4:05 p.m., $0.69

- National Health Investors (NHI) 4:07 p.m., $0.76

- Marriott Internationa (MAR) 4:10 p.m., $0.47

- Tesla Motors (TSLA) 4:10 p.m., ($0.62)

- Intrepid Potash (IPI), 4:15 p.m., $0.30

- C&J Energy Services (CJES) 4:15 p.m., $0.91

- Avis Budget Group (CAR) 4:15 p.m., $0.06

- Regency Energy Partners (RGP) 4:15 p.m., $0.13

- Kinross Gold (K CN) 4:15 p.m., $0.21

- CF Industries Holdings (CF) 4:18 p.m., $6.82

- Nvidia Corp. (NVDA) 4:19 p.m. $0.24

- Delphi Financial Group (DFG) 4:20 p.m. $0.88

- Agnico-Eagle Mines (AEM) 4:30 p.m., $0.47

- ION Geophysical (IO) 4:30 p.m., $0.16

- CenturyLink (CTL) 4:48 p.m., $0.61

- Federal Realty Investment Trust (FRT) 5 p.m., $0.98

- Oceaneering International Inc (OII) 5 p.m., $0.52

- MEMC Electronic Materials (WFR) 5:03 p.m., ($0.08)

- Georgia Gulf Corp. (GGC) 5:09 p.m., $0.12

- Energy Transfer Partners (ETP) 5:09 p.m., $0.66

- Sun Life Financial (SLF CN) 5:10 p.m., (C$0.60)

- Goldcorp (G CN) 5:15 p.m. $0.60

- Energy Transfer Equity (ETE) 5:15 p.m., $0.42

- Terex Corp. (TEX) 5:27 p.m., ($0.25)

- Cliffs Natural Resources (CLF) 5:42 p.m., $1.43

- Vectren Corp (VVC) 6:01 p.m., $0.57

- Vulcan Materials (VMC) 6:12 p.m., ($0.37)

- Manning & Napier (MN), postmkt, $0.25

- Westport Innovations (WPRT), postmkt, ($0.20)

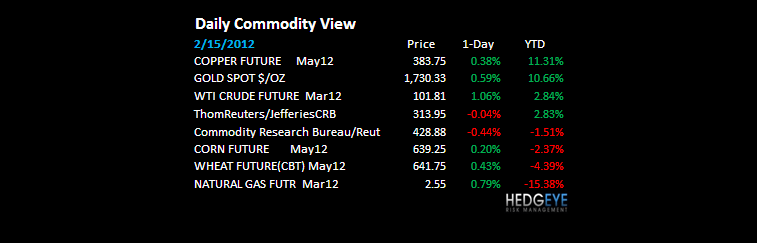

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – Brent or WTI, take your pick – both are in what we call a Bullish Formation (bullish TRADE, TREND, and TAIL) – and both have a systematic ability to infect (slow) Consumption growth both in the US and around the world. Feels like Q1/Q2 of 2011 all over again where consensus is still anchoring on the last 2 quarters of US GDP growth being good (it was).

- Coal Miner Turns Dealmaker at London Metal Exchange: Commodities

- Paulson Joins Tudor Selling SPDR Gold Shares as Soros Buys

- Crude Oil Advances as China Pledges Help on European Debt Crisis

- Commodities Climb to Six-Month High as Growth May Revive Demand

- Wheat Gains as Frost May Curb Ukrainian Production, Exports

- Cocoa Rises as Olam Says Beans Have ‘More Upside’; Coffee Gains

- Gold May Rise After China’s Pledge to Aid Europe Weakens Dollar

- Copper May Rise on Chinese Vow to Help Resolve Euro Debt Crisis

- China Steel Price Shows Asia Optimism Overdone: Chart of the Day

- Oil Refiners to Have Surplus Capacity in 2012, Barclays Says

- Brent Oil May Rise to $120 on Low Spare Supply, Goldman Says

- Asia Naphtha Refining Profits Reach Two-Week High: Oil Products

- Drillers Trailing High Yield Amid Fracking Boom: Canada Credit

- Chavez Misses $10 Billion a Month Curbing Oil Spending: Energy

- Nickel May Test Lower End of Range Trading: Technical Analysis

- Vancouver Could Handle More Kinder Morgan Oil, Port CEO Says

- Iran Oil Premium Defies Analysts Rejecting Risk: Energy Markets

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – the Nikkei busted a surprisingly bullish move = +2.3% overnight as the Yen remained under central planning pressure (-0.2% at 78.15 USD/YEN); the Nikkei getting squeezed like France’s CAC did right up to its long-term TAIL of resistance (TAILS: Nikkei = 9397, CAC = 3556) is what it is – largely a Pain Trade that tends to capitulate as the end of the rally nears. We’re long China, short Japan.

MIDDLE EAST

The Hedgeye Macro Team