TODAY’S S&P 500 SET-UP – February 14, 2012

As we look at today’s set up for the S&P 500, the range is 20 points or -0.72% downside to 1342 and 0.76% upside to 1362.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1607 (3211)

- VOLUME: NYSE 682.65 (-9.06%)

- VIX: 19.04 -8.42% YTD PERFORMANCE: -18.63%

- SPX PUT/CALL RATIO: 2.38 from 1.40 (70.00%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – the 10yr continues to trade between the rock (TRADE support = 1.96%) and the harder place (TREND resistance = 2.03%); still signaling a US Growth Slowdown in FEB (sequentially) as the Yield Spread (10/2s) compresses by 5bps day/day here…

- TED SPREAD: 40.60

- 3-MONTH T-BILL YIELD: 0.09%

- 10-Year: 1.98 from 1.97

- YIELD CURVE: 1.70 from 1.69

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30 am: NFIB Small Business Optimism, Jan., est. 95.0 (prior 93.8)

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Import price index, Jan.; Y/y est. up 7.2% (prior gain 8.5%), M/m est. up 0.3% (prior drop 0.1%)

- 8:30am: Advance retail sales, Jan., est. up 0.8% (prior up 0.1%)

- 8:45am: Fed’s Plosser speaks on economy in Newark, Del.

- 10am: Geithner testifies before Senate Finance Committee

- 10am: Business Inventories, Dec., est up 0.4% (prior up 0.3%)

- 11am: Fed to purchase $4.25-$5b notes

- 11:30am: U.S. to sell $20b 64-day cash management bills

- 1pm: U.S. to sell $40b 4-week bills

- 4:30pm: API weekly inventories

- 5:40pm: Fed’s Lockhart speaks on economic outlook in Sarasota, Fla.

GOVERNMENT:

- House, Senate in session:

- Senate Budget committee hearing on proposed FY2013 budget

- Senate Finance committee hearing on proposed FY2013 budget

- GE holds conference on “American Competitiveness: What Works” (through 2/16)

WHAT TO WATCH:

- Moody’s cut debt ratings of Italy, Spain, Portugal, said may strip France, U.K. of top Aaa ratings

- Senate Finance, Budget committees to have budget hearings today on Obama’s proposed $3.8t budget plan

- Deadline today for 13-F filings with the SEC for 4Q

- Santorum draws even with Romney in poll showing they trail Obama

- Boeing signs record order from Lion Air for 230 planes worth $22.4b

- Fed to issue decision “soon” on Capital One, ING Direct deal

- U.S. Volcker rule faces harsh critics as effective date nears

- Bank of Japan added $128b to asset-purchase program, set 1% inflation target

- Google wins U.S. antitrust approval to buy Motorola Mobility

EARNINGS

- Michael Kors (KORS), premkt, $0.06

- Host Hotels & Resorts (HST) 6 a.m., $0.30

- ACI Worldwide (ACIW) 6:45 a.m., $0.72

- United Therapeutics (UTHR) 7 a.m., $0.82

- Marsh & McLennan (MMC) 7 a.m., $0.45

- Omnicom (OMC) 7 a.m., $0.95

- Fossil (FOSL) 7 a.m., $0.97

- Watson Pharmaceuticals (WPI) 7 a.m., $1.76

- Avon (AVP), 7 a.m., $0.53

- Generac Holdings (GNRC) 7 a.m., $0.63

- RioCan REIT (REI-U CN) 7:30 a.m., C$0.35

- Hospira (HSP) 7:32 a.m., $0.47

- Goodyear Tire & Rubber (GT) 8 a.m., $0.21

- HCP (HCP), 8 a.m., $0.68

- BorgWarner (BWA) 8 a.m., $1.17

- TransCanada (TRP) 8:11 a.m., C$0.55

- Valspar (VAL) 8:40 a.m., $0.48

- Textainer Group Holdings (TGH) 8:45 a.m., $0.99

- Zynga (ZNGA), post-mkt, $0.03

- Quest Software (QSFT) 4 p.m., $0.51

- FMC Technologies (FTI) 4 p.m., $0.50

- Hittite Microwave (HITT) 4 p.m., $0.53

- Bob Evans (BOBE) 4:01 p.m., $0.60

- American Capital (ACAS) 4:01 p.m. $0.20

- Hatteras Financial (HTS) 4:01 p.m., $0.90

- Chemed (CHE) 4:01 p.m., $1.48

- American Campus Communities (ACC) 4:01 p.m., $0.49

- Weight Watchers International (WTW) 4:01 p.m. $0.86

- Taleo (TLEO) 4:02 p.m., $0.23

- TastGroup Properties (EGP) 4:02 p.m., $0.78

- MetLife (MET) 4:03 p.m., $1.24

- Arch Capital Group (ACGL) 4:05 p.m., $0.62

- Masimo (MASI), 4:05 p.m., $0.23

- Sapient (SAPE), 4:05 p.m., $0.16

- Tanger Factory Outlet Centers (SKT) 4:05 p.m., $0.41

- j2 Global Inv. (JCOM) 4:15 p.m., $0.62

- Home Capital Group (HCG CN) 5:01 p.m., C$1.49

- Natural Resource Partners (NRP) 5:05 p.m., $0.48

- Valmont Industries (VMI) 5:30 p.m., $1.67

- Curtiss-Wright (CW) 5:35 p.m., $0.84

- Brookfield Office Properties (BOX-U CN) 5:45 p.m., C$0.35

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor took a good look at his long-term TAIL of resistance ($3.98/lb) and not only backed off but is now breaking down through 3.87/lb immediate-term TRADE support. Watching that global growth signal closely as Hong Kong’s Finance Secretary warned of potentially seeing a down y/y Q112 GDP growth print.

- Zinc Glut Rising to Two-Decade High Threatens Rally: Commodities

- Copper Swings Between Gains, Losses on Confidence, Rating Cuts

- Corn Declines as U.S. Acres May Increase to Highest Since 1944

- Oil Rises to Three-Week High as Iran Threat Counters Europe Debt

- Cocoa Falls as Rains May Help West African Crops; Sugar Drops

- Iron Ore May Advance Amid Seasonal Demand Increase, UBS Says

- Gold May Decline as Stronger Dollar Cuts Demand After Downgrades

- Wheat Exports From Australia Seen at Record as Output Gains

- BP Boosts Cash Before Trial Threatening Image: Corporate Finance

- Soybeans May Advance on Fibonacci, ADM Says: Technical Analysis

- BHP, Rio Approve $4.5 Billion Escondida Copper Mine Expansion

- Oil Supplies Expand to Five-Month High in Survey: Energy Markets

- China Shale Delay to Boost LNG Imports in Boon for Exxon: Energy

- Container Rates Rebounding 29% as Cargo to U.S. Expands: Freight

- U.S. Farmers to Plant Most Corn Acres Since 1944, USDA Says

- BP Must Face Investors’ Fraud Claims Spurred by Gulf Oil Spill

- Sino-Forest Truth May Never Be Known as Ardell Defends Founder

CURRENCIES

EUROPEAN MARKETS

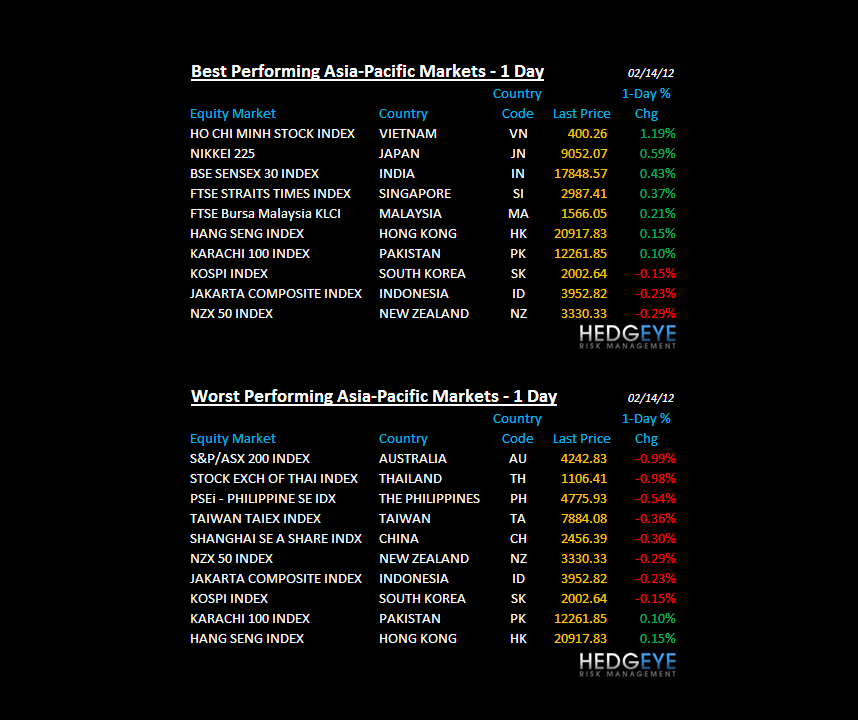

ASIAN MARKETS

JAPAN – evidently the Bank of Japan agrees with us in that they could have liquidity issues come the ides of March (massive sovereign debt spike). Surprisingly, the BOJ announced another 10 TRILLION Yens (lots of Yens) in easing last night; this lifted stocks and debauched the Yen. We’re finally seeing the 1.30 TREND line of YEN/USD snap. Stay tuned…

MIDDLE EAST

The Hedgeye Macro Team