Conclusion: HBI’s quarter might be fine, but we think the market knows it. A wide gap remains in pricing for core product amongst HBI’s largest customers, and this is at a time when competition will heat up. Cost will come down in 2H, but we think price comes down faster. If HBI is up on the print, we’d short it.

We’re still seeing a meaningful price disparity for HBI product across Mid and Discount channels. There’s a lot of ways we can slice the numbers, but there’s no disputing the inconsistency we’re seeing at retail. Of particular note is Kohl’s, who is pricing product 50% above JCP – and that’s after BOGO incentives. WMT and Amazon are nearly the same step down yet again, but for product that is almost identical to KSS and JCP (something tells us that Ron Johnson is keenly aware of this). With over half of HBI’s EBIT coming from US mass and department store channels – the very channels that we think will face considerable pressure and volatility in 1H12 – we still think that HBI has meaningful earnings risk.

How to play it? The company whiffed the third quarter, and took 4Q down to a level that is consistent with their visibility at the time – likely with some breathing room. But we don’t think that 4Q is the issue here. HBI is banking on maintaining price increases in 2H. But we simply don’t think that industry dynamics will allow them to stick. In addition to the dominos that we expect to fall due to actions at JCP/KSS/SHLD and subsequently Macy’s, Target, Wal-Mart and perhaps Amazon, bulls should note that we already saw WMT cut 7 points of revenue out of HBI’s core due to a shift to private label. This is BEFORE competition started to heat up.

A common response here is “what about easier cotton compares?” That’s valid, but we think that price will come down at a greater rate than cost. That’s bad.

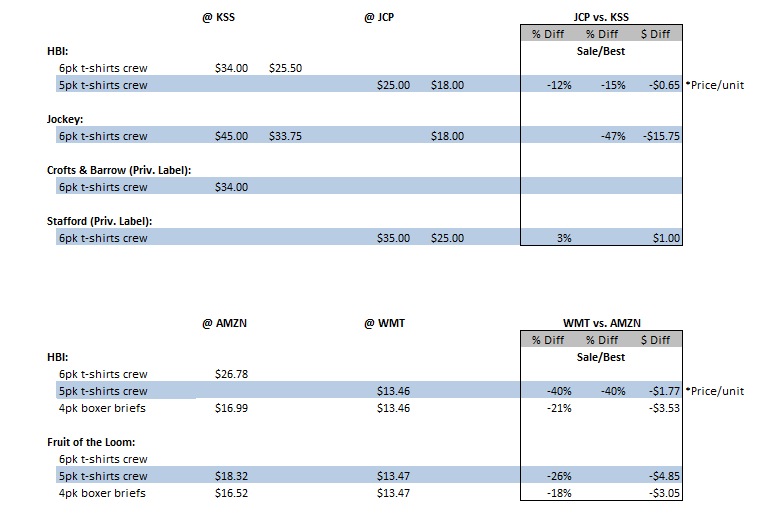

Here’s a snapshot of Hanes, Gildan/Starter, and private label pricing at the mid-tier as represented by JCP and KSS as well as WMT and AMZN along with some interesting callouts:

- There is a significant price differential between JCP and KSS in like-for-like basic men’s underwear (6pk crew t-shirts). On a price/unit basis, JCP now prices Hanes 12-15% lower than KSS.

- The other common brand Jockey, is priced 47% lower at JCP in this category.

- In Private Label, JCP’s Stafford line is actually priced 3% higher than KSS’s Crofts & Barrow.

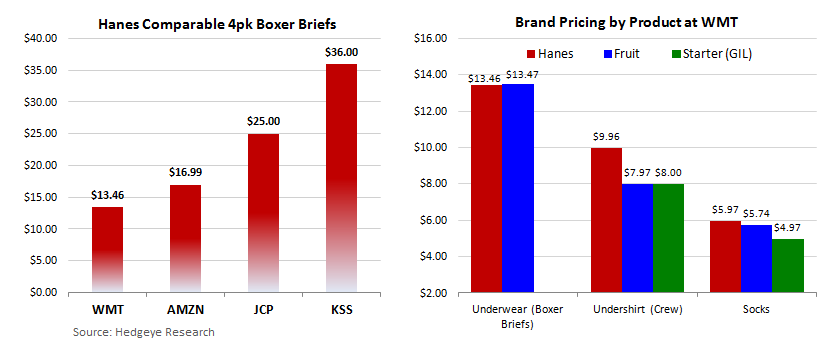

- Comparable men’s underwear (Hanes 4pk boxer briefs) had the most significant price disparity ($13.46 at WMT; $16.99 at AMZN; $25 at JCP; $36 at KSS) between retailers. At a 167% premium, KSS will need to seriously visit its current price positioning.

- At WMT, Hanes maintains its 10%-20% premium positioning, or $1-$2 price gap differential from competitors Fruit of the Loom and Starter in the underwear segment (crew t-shirts and tanks) as well as socks, while boxer briefs are indeed now at parity.

- In looking at AMZN’s online pricing, it appears WMT is the only retailer where the two brands are at pricing parity in the boxer brief category.