The bottom line is that the raw math suggests that there is no way the company is going to provide guidance in line with current consensus. Right now the current consensus is for 4Q11 EPS of $0.45, down 30% y/y and bringing the full year to $1.61, down 20% y/y. We think $0.43-$0.44 is more realistic and therefore so is $1.50 to $1.55 for 2012 EPS guidance.

Right out of the box, management needs to offset $0.26 to $0.30 of incremental EPS pressure in 2012 coming from share based compensation expense and incremental pre-openings costs. There are some offsets to those costs, but improving same-store sales trends in 2H12 will be one of the biggest contributors as the company begins to leverage the incremental labor costs implemented in 2Q11. Therefore, if the company can pull off a flat year in 2012, that will imply a strong year operationally and should go some way towards convincing investors that the turnaround is in motion.

As we said in our PFCB note two weeks ago, the “the road to recovery” for PFCB is 18 months in the making and the plan should come together in 2012, with management’s messaging taking a more distinctly positive tone in 2H12. In our aforementioned post of 2/6, “PFCB – The Queen Mary”, we summarized the evolution of the turnaround and the reason why we are close to the bottom that the top:

- DISCOVERY AND EVOLUTION: 2010 was the year of admitting to the real problems and 2011 was the year of planning for the future.

- IMPLEMENTATION AND EXECUTION: Now 2012 becomes the year of executing - new menu items, new look and new price points. The Irvine store will play a key role in this process.

- GETTING THE SYSTEM MOTIVATED: The onus in on management to get the employee base geared up for the changes, manage costs and driving consumer awareness of the changes taking place at PF Chang’s.

- CONTINUE TO EVOLVE: As a company, PFCB is not going to play defense, rather it is going on to be offensive in its strategy.

Here are some incremental thoughts around the messaging from the most recent earnings transcript and our view on those topics as we approach earnings this week:

THE PLAN: The challenge is converting that PF Chang’s brand equity into top-line momentum. The path to increasing traffic includes improving entry level pricing, enhancing our overall price-value equations, providing more differentiated options at lunch, and increasing menu diversity.

HEDGEYE: To-date, the details of how the plan will unfold and the implication for margins is still an unknown to the Street. See our note from 2/6, “The Queen Mary” for details.

REMODEL SPENDING: Management has discussed plans to invest in a Bistro remodel program, with the expectation of spending around $25 million 2012.

HEDGEYE: Management is still working through some of the design elements from the “Irvine Project” so we do not see this number being revised significantly higher.

IMPAIRMENT CHARGES: Last quarter there was a charge of $4.8 million or $0.16 per share related to one Bistro location in Corte Madera, California and two Pei Wei locations (one in Farmington Hills, Michigan and one in Chino Hills, California). We’re assuming that their 4Q11 quarterly analysis will identify more locations that need to be closed or written down.

HEDGEYE: This needs to happen sooner rather than later and will, in our view, help grow EBITDA in 2012.

LOWER GUIDANCE: The last full-year EPS range offered as guidance for 2011 was $1.60 to $1.70, assuming comp trends “will improve slightly from where they were in Q3” since, the company claimed, there were “easier comparisons coming up at the Bistro in the fourth quarter”. The company still expects full year comps to be down 2% to 3% at both concepts.

HEDGEYE: This is a difficult call to make, but given the risk/reward setup, we are a buyer on weakness after the earnings event. We think consensus FY12 EPS is likely to come down due to outlier estimates but we are a buyer on weakness once this quarter is behind us. This quarter should mark the bottom in negative revisions and the upside in the stock, in our view, far outstrips the downside. We believe that sales could be choppy for a couple of quarters, but – as we maintained with EAT in May 2010 – we believe that management is doing the correct things and that earnings revisions should turn, albeit slowly (like the Queen Mary).

SALES

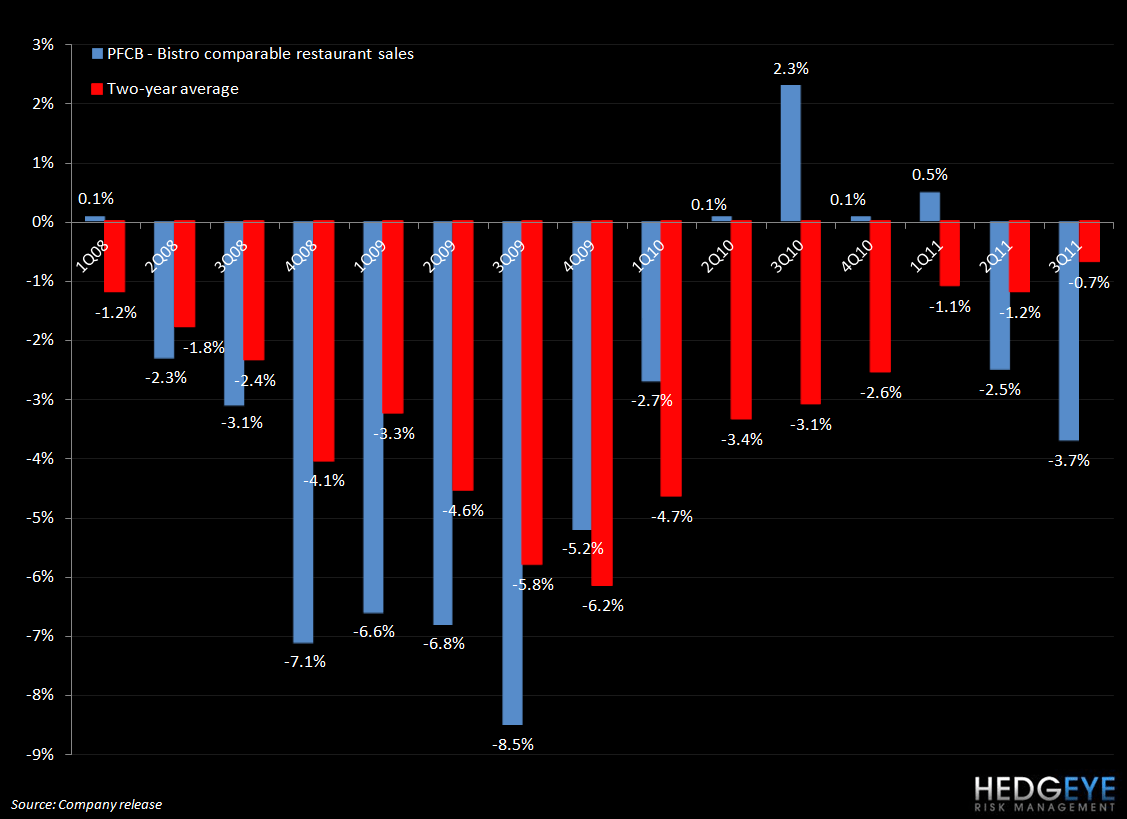

We suspect that the current trends have improved at the Bistro, along with the rest of the industry. Here is a recap of 3Q11 performance for the Bistro.

- Bistro revenues were down 3.5% in the third quarter with comp sales coming at a negative 3.7%

- The impact of Hurricane Irene, which resulted in 75 closed store days and cost about 40 basis points of comp sales during 3Q11

- Bistro sales softness was widespread across all day-parts but weekdays continue to perform slightly better than a weekend, that’s like a reflection of the ongoing strength of our business guests

- From a geographic perspective, the Bistro saw negative comps in most states. Some of the weakness in the northeast was due to the hurricane

- The good news is that we are seeing some sequential trends flatten out a bit in large states like California, Arizona and Nevada

- Comp trends in Florida actually improved sequentially in 3Q11

- As the quarter progressed and year-over-year comparisons got a little bit easier, we saw overall comps get stronger

- Two-year trends have shown some improvements in recent months

The messaging from Pei We last quarter was not good and I don’t hold out much hope for Pei Wei in its current form.

- Pei Wei 3Q11 quarter comp sales were down 3.6%

- Pei Wei sales softness was also widespread as Texas, Arizona, Florida and California which collectively represent two-thirds of our business remain negative

HEDGEYE: This quarter is less important than the forward commentary which we think will be more positive than the Street expects. The Bistro has a strong January and some of the current initiatives are showing favorable trends in the test markets – any incremental positive or less-bad messaging around Pei Wei is an added bonus.

EXPENSES

While much of the focus is around top line trends and deducing whether or not the company is turning its concepts around, commodity inflation and other factors are pressuring margins. Here is a recap of commentary on these items from the 3Q earnings call.

- Commodity costs were higher for most of their product basket, with cost of sales increasing about 50 basis points - Beef, wok oil, and Asian import prices all climbed, but with the benefit of contractual price rebate on poultry

- Without the poultry rebate, cost of sales would have been up more than a 100 basis points, consistent with expectations of 4% to 5% commodities cost pressure.

- Consolidated labor expense increased about 110 basis points. This includes the cost of targeted investments in staffing to support the Bistro guest experience and some pressure from new staff labor and efficiencies at Pei Wei.

- Operating expenses increased 120 bps in 2Q11 on sales deleverage as well as a number of cost pressures that were unique to 3Q11 (including additional supplies and printing costs related to the re-launch of Happy Hour, and the write-off of Bistro card printing expenses.)

- Overall, the top line and cost pressures added up to 340bps decrease in Bistro restaurant operating margins down to 16% and a 200 basis point decline in Pei Wei margins to 13.9%.

- Projecting commodities inflation of 4% to 5% in 4Q. Inflation pressure should moderate in 2012

- Continued pressure on the labor line, but some of the operating expense increases should moderate in 4Q11. In total, restaurant operating margins are expected to decline about 150 basis points for a full year (excluding asset impairment charges).

HEDGEYE: Without an improvement in top line trends, the expense side of the equation is going to be a drag on EPS in 2012.

Howard Penney

Managing Director

Rory Green

Analyst