Conclusion: The price of oil globally continues to march higher despite miles driven in the United States declining to levels not seen since 1999. The fact that oil climbs higher despite this bearish demand statistic is a bullish indicator as to the resiliency of the price of oil.

Positions: Long BTE and Long XLE

We have a bullish view of oil, which is primarily driven by monetary policy and limited supply. On the first point, dovish, or inflationary, U.S. monetary policy is a headwind for the U.S. dollar and tailwind for those global commodities priced in the U.S. dollar. Over the last three years the correlations of both WTI and Brent versus the U.S. dollar are -0.65 and -0.66, respectively. The FOMC’s decision to extend “exceptionally low levels” for the federal funds rate through 2014 further supports this bullish factor.

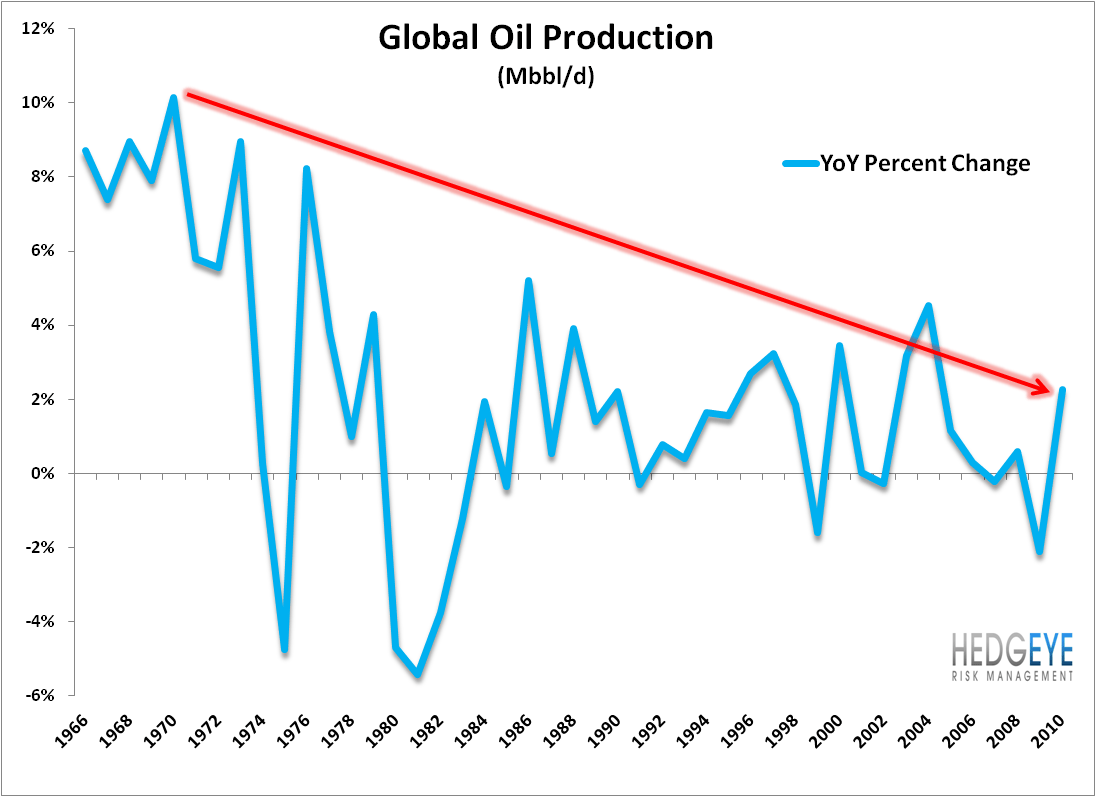

On the second factor of supply, in the chart below we highlight the trend in annual global oil production growth from 1966 – 2010. The trend is clearly that the world’s ability to grow year-over-year production has become increasingly limited in the last decade, especially versus the late 1960s and early 1970s when global oil production had a number of years of almost double digit year-over-year growth. Production from 2001 – 2010 grew at annual basis of only +0.94%, which is below the average annual growth since 1966 of +2.20%, but also occurred during a period in which the price of oil was up more than 400%. So, despite clear incentives to produce more, the world’s oil producers are seemingly unable to ramp production.

An emerging counter point to the bullish case for oil is declining demand for oil in the U.S., at least based on miles driven by U.S. consumers. In the chart below, we show finished motor gasoline supplied in the United States every week. As the chart shows, not only has this proxy for demand flat lined since 2004, but the most recent data points actually suggest meaningful year-over-year declines. In fact, in the most recently reported data from the Department of Energy, which was for the week ending February 3rd 2012, finished motor gasoline supplied was down -5.7% year-over-year. This data rhymes with the U.S. gasoline demand as reported by Master Card, which showed a -5.3% decline last week and the 24thstraight week of y-o-y gasoline demand decline.

From our perspective, we are seeing the real time impact of The Bernank Tax. The inflation of oil leads to, naturally, lower demand or use of gasoline, which is a headwind to economic activity and specifically consumption, which makes up 70% of U.S. GDP. Increasing energy prices also impacts consumer confidence. The most recent data point on this front is the University of Michigan Consumer Sentiment Survey, which today showed that current conditions sequentially declined to 79.6 in February versus 84.2 in January. Not surprising, given the The Bernank Tax, Brent is up almost 10% in the year-to-date.

Daryl G. Jones

Director of Research