A Year in the Making ...

The long-rumored servicer settlement details are out at last, with a final announcement expected later today. We've dug in to the details, and it looks like a strong win for the banks. Of the $26B total value (per the WSJ), only about $5B is in the form of cash payment. The balance is from principal write-downs and economic benefit of refinancing. That's a sweetheart deal, especially considering that the principal write-downs can involve mortgages that the servicers don't even own. For details, see below.

Quick Take on the Details:

- $26 billion settlement, including CA & NY (WSJ)

- $4-5 billion in cash payments by the banks to foreclosed homeowners

- $21-22 billion in principal forgiveness and underwater refinancing assistance

- Of the $21-22 billion, $17 billion will apply to mortgage-backed securities investors, having no impact on the banks.

- The remaining $3-5 billion will be principal forgiveness and underwater refinancing

- Principal Write-Downs: Banks must effect $17B of principal write-downs for current borrowers.

Hedgeye: Banks are using the best kind of money to pay for these principal write-downs: other people's money. Yes, this $17B will come out of the pocket of private label MBS investors. Haven't PLMBS investors suffered enough? In all seriousness, are there any accusations of wrongdoing against PLMBS investors? Why are they bearing the cost? If the argument is to help the broader housing market by helping underwater borrowers, this is a drop in the bucket. Estimates of the total underwater balance of US borrowers are in the $700B - $750B range. $17B barely touches that.

- Payment to borrowers: According to the WSJ and FT, borrowers will receive payments totaling $4.2 - $5.0B. The WSJ reports that $1.5B of that will go to borrowers who were foreclosed between September 2008 and last December.

Hedgeye: This makes little sense to us. If a borrower wasn't wrongfully foreclosed on, why do they get any monetary settlement? And if a borrower was wrongfully removed from their home (as happened in certain cases), then a $1,500 payment hardly constitutes justice. What's more, the time frame is odd. Did the banks change their practices at the beginning of 2012?

Refinancing: Banks must provide $3B worth of benefit to borrowers in the form of refinancing.

Hedgeye: This is once again other people's money, except to the extent that banks are refinancing loans that they own.

Liability Waivers: Banks are freed from further liability from the AGs or regulators around foreclosures. However, they don't gain liability waivers around MERS (NY AG Scheiderman's suit will proceed) or around securitization (Schneiderman again, along with the FHFA).

Hedgeye: That's a pretty good deal on foreclosure wrongs - some states have serious penalties for wrongful foreclosures, and the servicers escape the threat of all of that. Waivers on other elements would be a real gift.

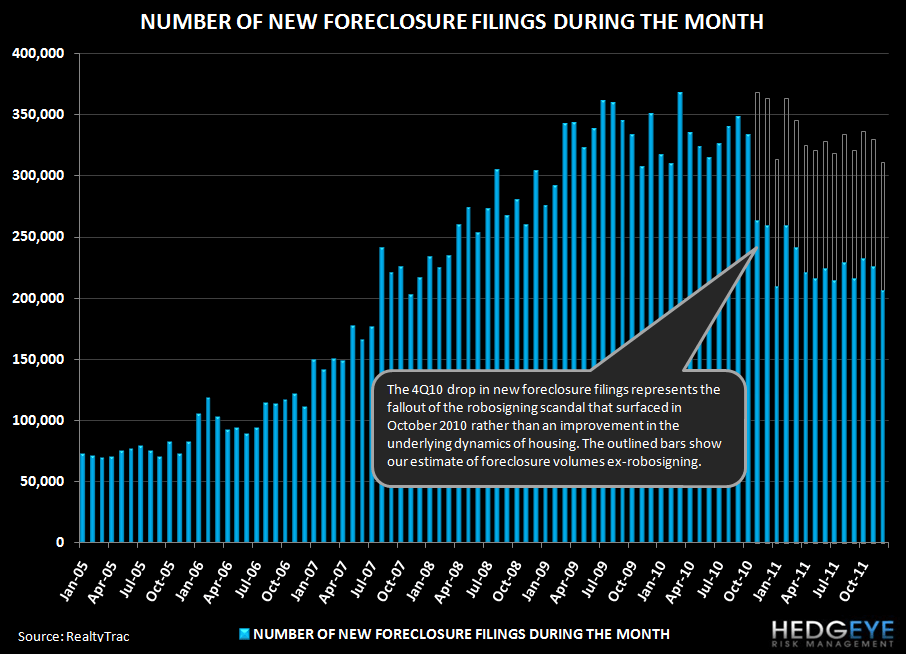

Implications of Rising Foreclosures - Bad News For Cards

We wrote extensively on the negative implications of a servicer settlement for the credit card operators back on 7/11/11. But to recap our thoughts we offer the following summary. Clearing the legal morass around foreclosures will cause them to re-accelerate. The chart below shows the swift drop-off in foreclosure filings when the robosigning scandal broke in October 2010. While reformed practices may slow the timeline somewhat compared to the pre-scandal time period, and increase in the pace of foreclosures from current levels is very likely. This has several implications:

1) More pressure on home prices: More low-level transactions in the distressed market pulls the home price indicators lower. Extremely low comps can also pressure non-distressed transactions.

2) More bankruptcies: As we showed in a prior research report, foreclosures are highly correlated with bankruptcies. Although the causality isn't always from foreclosures to bankruptcies, it often is: a bankruptcy filing can serve as a last-ditch effort to save a home. Increasing bankruptcy filings is a negative for the credit card issuers. We believe that part of the very low credit costs at the card names for the last five quarters is due to the artificial suppression of foreclosures. Because bankruptcies flow straight to charge-offs without spending time in delinquent status, the increase in credit costs could hit very quickly. This would be a negative for the pure-play card names (COF, DFS, AXP) and would slightly offset the benefit for the moneycenters.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky