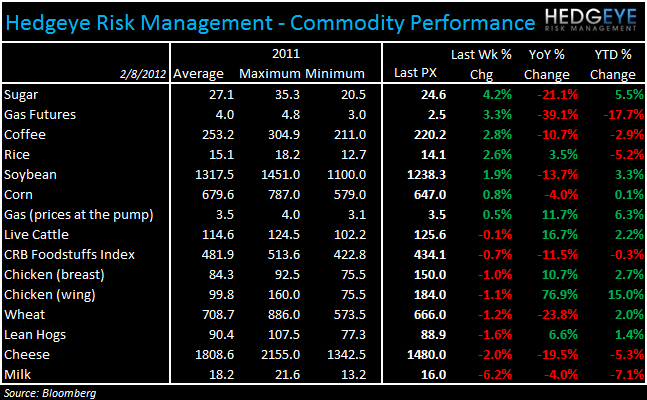

Strong employment trends and favorable weather versus last year has translated into strong top line trends in 4Q and 1Q to date for companies across the restaurant space. As the benefit of weather fades and compares become more difficult from a top-line perspective as we move through the year, we would expect commodity costs to play a greater role in stocks with exposure to certain commodities. On aggregate, 2011 was a year where the restaurant space was under pressure from a commodity inflation perspective but strong sales helped most companies leverage COGs. With overall commodity inflation abating in 2012, and sales trends remaining strong, many expect restaurant companies to continue to post impressive earnings growth. We agree with that view but think that there are companies that are facing significant exposure to protein costs that may pressure profit margins for FY12 more than expectations are anticipating.

SUPPLY & DEMAND

Beef – WEN, JACK, CMG, TXRH

Beef prices are a factor for most of the restaurant companies we follow but WEN (20% of food and paper spend), JACK (20% of commodity basket), TXRH, and CMG are especially exposed. The chart of live cattle prices, in the “charts” section of this post, below, shows just how far prices have run. Grain prices are holding up at current (elevated) levels and that does not bode well for those hoping for beef prices to snap back.

SUPPLY

The U.S. cattle inventory is down 1.9% from a year ago and 6% from the January 2007 peak. While a decline in cattle numbers from a year ago was expected, the drought of summer 2011 that affected the cattle industry added to the liquidation and inventory came in even lower than expectations. Jim Ross, of the Livestock Marketing Information Center, said in an interview with CattleNetwork that he expects no significant increase in U.S. beef production until at least 2015 as other countries are only beginning to cut production now.

DEMAND

Increasing export demand from emerging markets remains supportive for beef prices. We will be watching broad economic trends and the U.S. dollar to assess how demand is likely to impact beef prices. Supply, at least recently, has been the most important factor in driving such high prices over the last nine months.

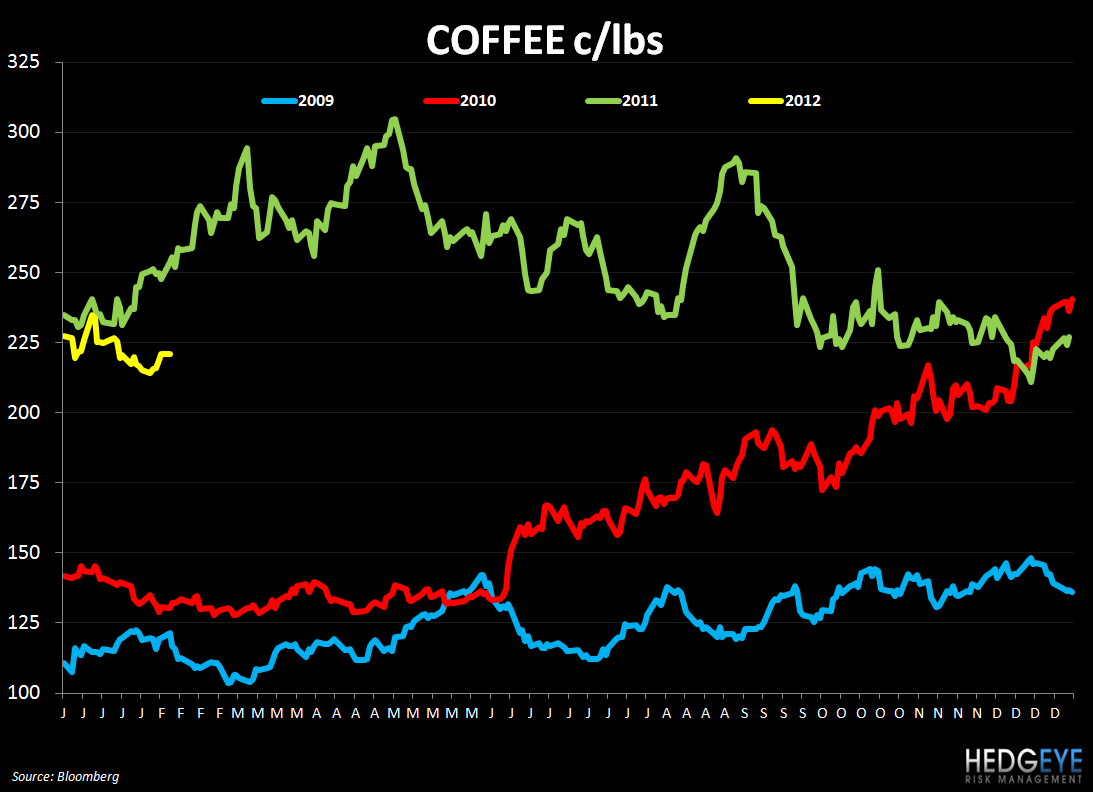

Coffee – SBUX, PEET, DNKN, CBOU, THI, MCD

Coffee prices gained 2.8% week-over-week but are almost 11% below last year’s levels. SBUX has its coffee costs locked through most of 2013. The company is past the peak of the inflation seen in coffee prices, according to management commentary on its most recent earnings call (1/26). Coffee costs have impacted PEET heavily and, as of the company’s most recent earnings call on 11/1/11, inflation had gotten ahead of pricing. While coffee prices have come down, it seems that supply and demand dynamics are likely to support prices or, at least, make a drastic decline from here unlikely.

SUPPLY

Global coffee production for 2011/12 will be 130.9 million bags, down from last month’s estimate of 132.4 million bags, according to the International Coffee Organization.

DEMAND

Coffee shipments from Brazil, the world’s largest producer and exporter, fell 26% in January from a year earlier.

Global coffee consumption for 2011/12 will be 136.5 million bags versus 135 million bags in 2010 due to increased demand from emerging markets, according to the International Coffee Organization.

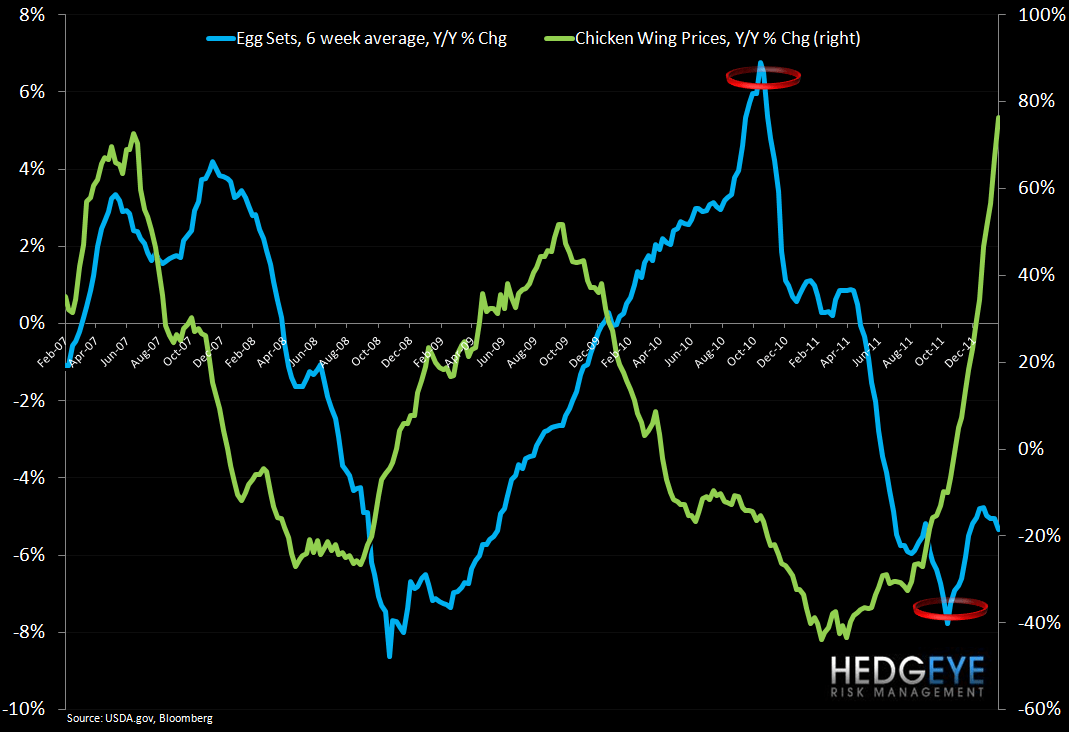

Chicken Wings – BWLD

Commodity cost inflation for BWLD will step up in 1Q with 2Q being the most unfavorable compare if prices remain elevated, as wing prices bottomed in 2Q10.

SUPPLY

The six-week moving average egg sets number declined sequentially from -5% for the week ended 1/28 to -5.3% for the week ended 2/4. This is a bullish data point for chicken wing prices.

DEMAND

As beef prices go higher, we expect the food service industry to shift focus to chicken to alleviate cost pressures.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

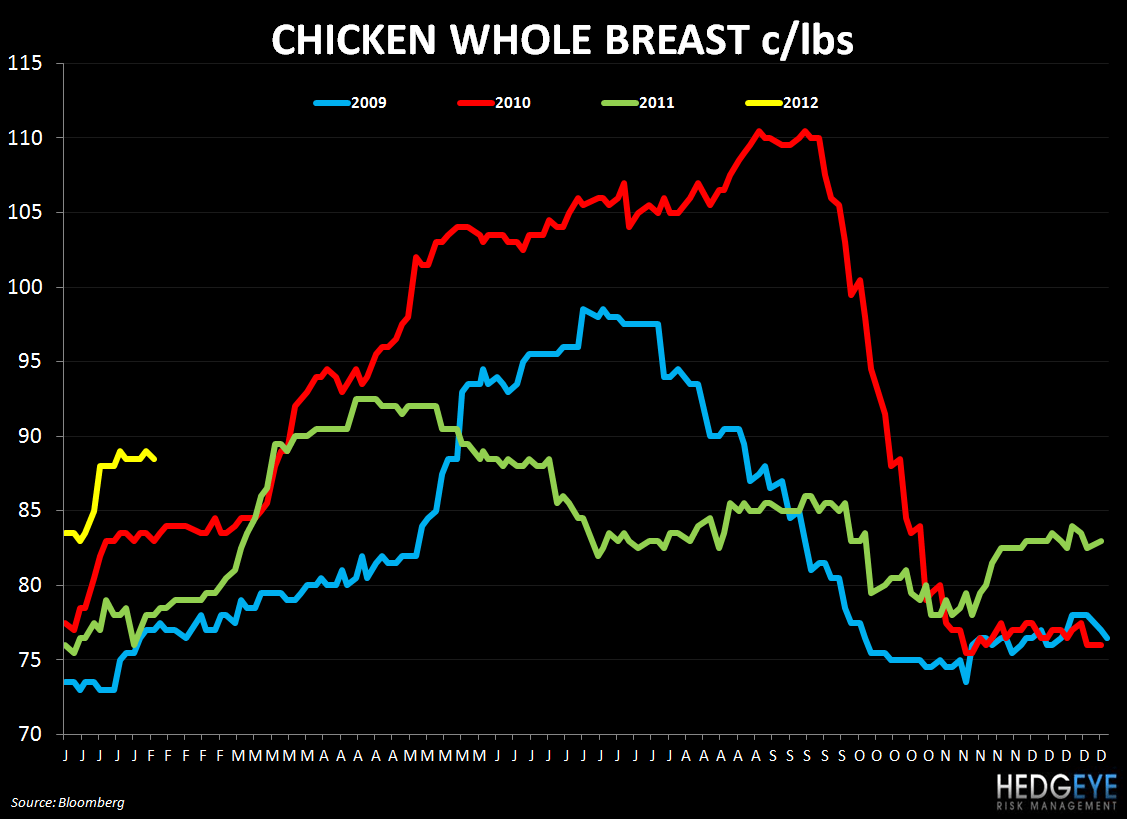

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst