McDonald’s will release January sales tomorrow before market open.

McDonald’s has been one of our favorite stocks in the restaurant space and the company continues to take share from competitors domestically. This month is not expected to yield any huge surprise as management guided to 5.5-6.5% global same-store sales for January during the earnings call on 1/24.

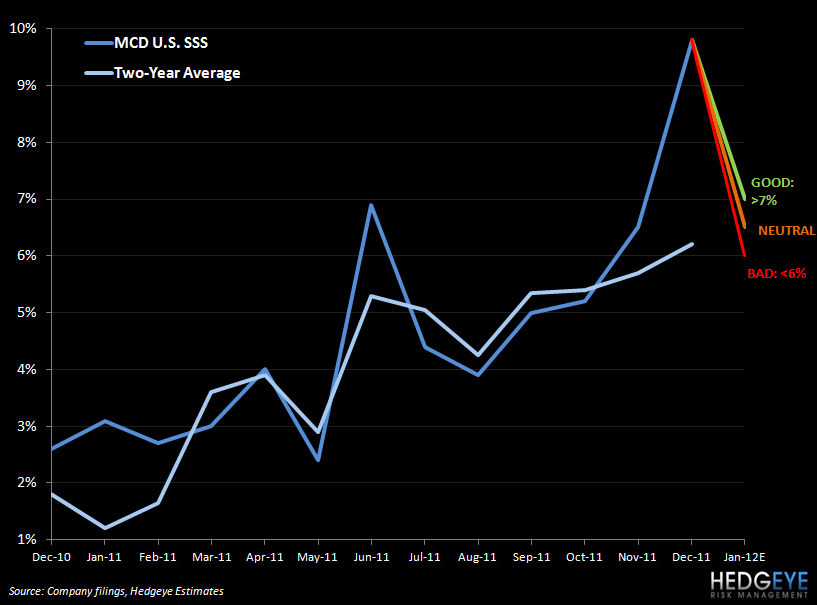

Below we go through our take on what numbers will be received by investors as good, bad, and neutral MCD comps numbers by region. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to January 2011, January 2010 had one less Saturday and one additional Tuesday. We expect a negative calendar shift as a result.

U.S. – facing a compare of +3.1%, including a calendar shift of between -1.3% and -0.4% varying by area of the world:

GOOD: A print of higher than 7% would be received as a good result as it would imply a sequential acceleration in two-year average trends on a calendar-adjusted basis. Additionally, 7% is above the guided range for global January comps and, since the U.S. business represents 45% of the operating income of the company, healthy trends in the domestic market are good for the stock. We expect the US comp to come in at 7%.

NEUTRAL: A print of between 6-7% would be received as neutral as it would imply two-year average trends that are roughly flat on a calendar-adjusted basis. Expectations for MCD are lofty as the sell off on strong 4Q11 results indicated, and any signal that things are slowing on the margin may lead to further declines in the stock.

BAD: A result of less than 6% would imply a slowdown in two-year average trends on a calendar-adjusted basis and, therefore, would likely be received as a poor result by investors.

Europe – facing a difficult compare of +7.0%, including a calendar shift of between -1.3% and -0.4% varying by area of the world:

GOOD: A result of 4.0% or higher would be received as a strong result as it would imply two-year average trends higher than those seen in December on a calendar-adjusted basis. We are holding Europe to a high standard in our estimates as economic weakness has seen consumers seek out the value McDonald’s offers.

NEUTRAL: A print between 3% and 4% would be received as neutral by investors, in our view, as it would signal a stabilization, rather than further expansion, of two-year average trends.

BAD: A Europe comp of below 3% would be received as a bad print by investors as it would imply a slowdown in two-year average trends. The consensus estimate for Europe comps is at 3.72%, per Consensus Metrix.

APMEA – facing a compare of 5.2%, including a calendar shift of between -1.3% and -0.4% varying by area of the world:

GOOD: A result of 7% or higher would be received as a good result by investors as it would imply two-year average trends that are roughly flat on a calendar-adjusted basis. The Chinese New Year fell on January 23rd in 2012 versus February 3rd in 2011 so we expect a positive impact from that on the company’s China business. YUM also mentioned on its earnings call this morning that its business performed well in January.

NEUTRAL: A result of between 6% and 7% same-store sales in January would be a neutral result for APMEA.

BAD: A print of less than 6% in January would imply a significant slowdown in two-year average trends in APMEA on a calendar-adjusted basis.

Howard Penney

Managing Director

Rory Green

Analyst